sshepard

Co-authored by Treading Softly

There is a basic saying that “if you cannot beat them, be a part of them.”

On the subject of approaching the market to assemble earnings out of your holdings successfully, there might be areas out there the place you can’t produce higher earnings than the businesses that exist already there. The banking sector has existed for an exceptionally very long time and continues to be a significant a part of the economic system as a result of it supplies monetary companies that different corporations and sectors haven’t been in a position to successfully present on their very own. We have seen that when corporations wish to present related companies, they grow to be a financial institution; have a look at NewtekOne (NEWT) for instance. They had been a fantastically well-run BDC (Enterprise Growth Firm), however they determined that they wished to increase their choices to be extra of what a monetary establishment can be. So, they determined to grow to be a financial institution as a result of they might not sustain with banks with out changing into one themselves. They successfully mentioned we will not beat them, so we’ll be a part of them.

In case you’re following our distinctive Revenue Methodology to generate a livable yield out of your investments to pay your bills and stay your life to the fullest, typically it’s worthwhile to settle for that in the case of the monetary sector, there’s not significantly better you are able to do however to hitch the banks.

On this regard, I wish to look at two alternative ways that you could be a part of the banks. One entails investing in an enormous array of economic establishments, and the opposite entails investing in the identical forms of property that banks are investing in themselves.

Let’s dive in!

BTO — Yield 9.3%

John Hancock Monetary Alternatives Fund (BTO) is a CEF (Closed-Finish Fund) that invests in banks. Banks have fallen out of favor up to now couple of years, because the failure of Silicon Valley Financial institution sparked fears of one other bank-driven monetary disaster. Greater than a 12 months later, we will see that the fears did not materialize into actuality, because it turned out the boogeyman wasn’t really underneath the mattress.

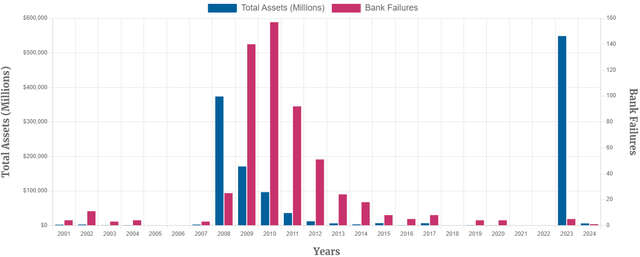

When it comes to property, the financial institution failures of 2023 had been big. The information media turned hyper-sensitive, and fears of financial institution panic spreading had been in all places. Some may discover it stunning that financial institution failures are pretty frequent. From 2015 via 2019, 25 banks failed with little fanfare. Supply

FDIC

What was startling final 12 months was not the variety of financial institution failures, however the sheer quantity of property, because the failure of Silicon Valley Financial institution was big. But, as we sit right here as we speak, we might be assured that it wasn’t a “Lehman second”, as some had been suggesting on the time. In the course of the crises, we famous that the problems with Silicon Valley Financial institution had been particular to them and never indicative of a systemic disaster.

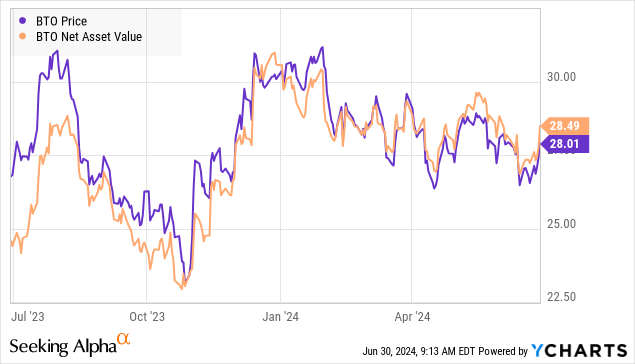

Quick-forward to as we speak — banks are now not at panic costs however are nonetheless buying and selling at very enticing valuations. The market stopped panicking, however remains to be a bit cautious about banks. For BTO, which means the value is at the moment buying and selling at a reduction to Web Asset Worth.

For a fund that routinely trades at a wholesome premium, it is a shopping for alternative.

We proceed to imagine that the structural dangers for banks are a lot decrease than some out there imagine. Banks had been careworn by declining Treasury costs on their steadiness sheets, however as rates of interest stabilize, the shock of the impression is dissipating. If rates of interest begin declining, that may velocity up the method, however it’s hardly required. The Treasury portfolios that the bears cherished to level to as having big unrealized losses are slowly curing themselves as Treasuries mature at par and are reinvested into new Treasuries at as we speak’s larger charges.

Whereas there’s actually some stress on business actual property that would trigger credit score losses at some banks, we do not see something that’s practically as important as the ever present mortgages and CDOs (Collateralized Debt Obligations) that collapsed throughout the GFC. Banking laws are much more strict, and the positioning of banks is much extra conservative. We aren’t in a interval the place credit score issuance was excessive and irresponsible. No matter overenthusiasm there was within the credit score markets, skilled a bucket of chilly water throughout COVID. In consequence, credit score high quality is comparatively robust amongst debtors in comparison with different pre-recession durations. This is the reason we count on that if there’s a recession, it’s unlikely to be a extreme one for lenders. This consists of financial institution and non-bank lenders.

JAAA and CLOA — Yield +6%

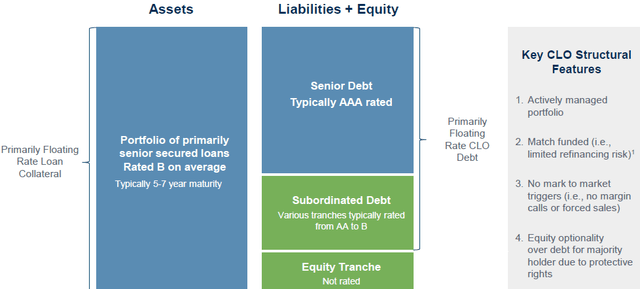

BlackRock AAA CLO ETF (CLOA) and Janus Henderson AAA CLO ETF (JAAA) are funds that supply enticing 6% yields. Once we often speak about CLO (Collateralized Mortgage Obligations) funds, we concentrate on funds on the underside aspect of the CLO construction. The fairness and subordinated tranches supply extraordinarily excessive yields on this atmosphere. Supply

ECC Earnings Name Presentation

This might be the upper threat however a lot larger reward aspect of issues. In case you’ve learn our articles on OXLC (Oxford Lane Capital) or ECC (Eagle Level credit score), which put money into the underside degree of a CLO, the fairness tranche, which presents the best threat however highest reward. We have now additionally recommended the thought of investing in Eagle Level Revenue Firm (EIC), which invests within the subordinated debt part of a CLO.

Many have requested us about safer choices. These two ETFs put money into the most important part of a CLO, which predominantly and traditionally has been owned by high-net-worth people, monetary establishments like main banks, and insurance coverage companies. That is as a result of Triple-A CLO debt is taken into account to be among the many lowest-risk debt investments doable alongside extremely rated company bonds, company mortgage-backed securities, and U.S. Treasury notes.

These senior tranches have little credit score threat as a result of the complete construction of a CLO is designed to make sure that the AAA tranches receives a commission first. Nonetheless, the underlying debtors are nonetheless rated B/B+. In consequence, these investments present a barely larger degree of earnings than a Treasury notice. Nonetheless, not like fixed-income options, Triple-A CLO debt is a floating funding.

In case you count on rates of interest to stay larger for longer and need a spot to place money that gives the next yield than Treasury notes, these ETFs are an affordable choice. It’s value noting that the distributions will probably be variable and can decline if rates of interest decline.

When it comes to worth volatility, JAAA/CLOA might be anticipated to have comparatively low worth swings. The value will probably be delicate to adjustments in rate of interest outlooks and may very well be impacted by default fears, however possible far lower than many different investments. To be clear, the chance is low relative to different funding choices, and it might be cheap to place funding cash right here to earn the next yield whilst you anticipate alternatives to deploy it. It’s a place for cash the place you need decrease threat. Nonetheless, it’s not a protected place for cash the place you can not tolerate any threat like your emergency fund. Value swings over a month or two are more likely to be within the low single digits, however they’ll occur and, in a panic-type occasion, may very well be bigger.

I do know a whole lot of traders are on the lookout for a lower-risk place to place their money that may earn the next yield than possibly their cash market account from their brokerage is providing. These two funds are an amazing alternative with the understanding that the yield will decline in live performance with adjustments in short-term rates of interest.

Conclusion

With BTO, JAAA, and CLOA, we’ve got a number of routes to have the ability to make investments alongside or in monetary establishments that enable us to take pleasure in robust earnings from them. BTO offers you publicity to an enormous array of economic establishments to gather an amazing yield from the effectiveness of skilled fund managers. CLOA and JAAA present us a path to put money into Triple-A CLO debt to gather the next yield earnings at very low dangers, proper alongside monetary establishments that put money into such a debt, MBS, and Treasury notes. On the finish of the day, our aim is to maximise the earnings we will obtain and decrease the dangers that we tackle. These alternatives as we speak enable us to hit that candy spot between threat and reward to have the ability to acquire nice earnings with out having to tackle outsized threat.

On the subject of retirement, the best threat you face is changing into financially destitute. Sadly, it is a truth of life that as we become older, our well being will wane, and we might want to make investments extra of our time and power into sustaining our well being. The very last thing you wish to do is fear about your funds whilst you’re taking good care of your well being and having fun with retirement along with your family members. This is the reason I created my Revenue Methodology within the first place, to assist remedy a few of retirement’s greatest burning questions and meet these wants head-on. That is the great thing about my Revenue Methodology. That is the great thing about earnings investing. At the moment, it is time to determine that if you cannot beat the sustainable earnings technology of our Revenue Methodology, it could be time to hitch it.

{kind=link}