kontrast-fotodesign

Pricey readers/followers,

Fresenius Medical Care (OTCPK:FMCQF) (NYSE:FMS) is an organization that I have been overlaying for years, and investing in for years. For sure elements of my place, I am truly at a really spectacular total RoR. That isn’t the case for the whole lot of my present place in Fresenius – and as earlier than, my funding into the corporate is finished utilizing the bigger Fresenius firm, not the Fresenius Medical Care Arm.

Nonetheless, Fresenius owns a big a part of the Medical Care firm, so that is nonetheless a related strategy and one which I consider will finally lead to outperformance. I’d be mendacity if I mentioned that I wasn’t disillusioned on the period of time that it is taken for the corporate to see even some extent of normalization right here.

On this article, I am going to replace my thesis for the following 12 months and see what we might anticipate for 2024-2026 from the Medical Care firm.

Additionally, I’ve had some short-term success with the advice to my final article – although within the bigger context, the corporate nonetheless must get better much more.

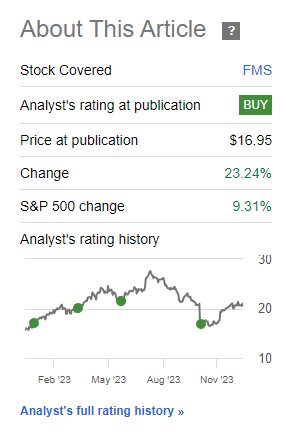

Looking for Alpha Fresenius Medical Care (Looking for Alpha)

Fresenius Medical Care – Lots to love, assuming the corporate finally reverses

The market has already spoken as to what’s too low-cost, and what is not. Again in October of 2023, the corporate dove for a month or two, earlier than recovering firmly again to a $20/share stage for the FMS ticker. The yield right here just isn’t engaging – we’re speaking lower than 3% in an setting with 4%+ risk-free – so the upside for the corporate must be considerably engaging for this to make any type of sense.

Fortunately, that is truly the case right here.

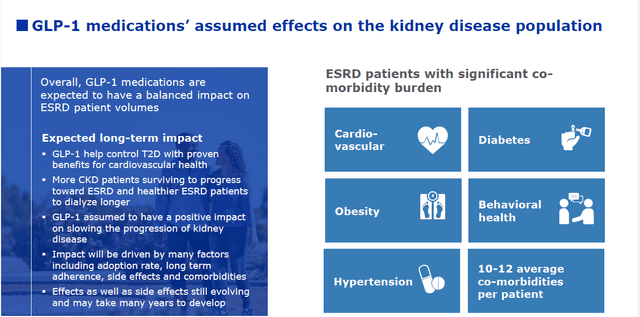

My final article on this firm coincided with the crash, which in itself was an overreaction to the Danish firm Novo Nordisk (NVO) and its weight-loss drug Ozempic. I spent the article displaying why this was an overreaction, and why even when Ozempic brought about every little thing that its proponents hoped, this nonetheless would not imply any type of elementary decline for Fresenius.

Ozempic is Novo’s GLP-1 drug, and Novo has been pinning a good bit of hope on the drug for the long run. On account of this, dialysis firms that labored on the opposite facet of this space dropped double digits again in mid-October when the efficacy of this drug grew to become clearly indicated. I do not simply imply FMS, as a result of I additionally spend money on different firms. Companies like Baxter (BAX), and Outset Medical (OM), dropped double-digits, with onset dropping probably the most at 21% in a single day, being probably the most uncovered on this context.

The explanation why the affect of Ozempic is not as unhealthy as many appeared to worry are clear – or on this case, truly unclear. From the dearth of readability in healthcare financial savings prices, the truth that it is on no account a treatment for Kidney failure, however merely a delay within the development of kidney illness, appears to indicate to me that the market did not perceive that this was doubtlessly solely a income hit – not a elementary enterprise risk.

We have now 3Q23 outcomes to take a look at, which got here out in November about 2 months in the past.

The corporate’s present heavy focus is on unlocking its worth as a number one kidney care firm. It is lower down segments to 2, simplified the corporate’s monetary reporting, and total optimized its capital allocation and the way it works with its phase with its FME25 targets, in each Care Supply and Care Enablement, it is now two segments.

The corporate itself addressed at first, the expectation of the affect of GLP medicines.

FMS IR (FMS IR)

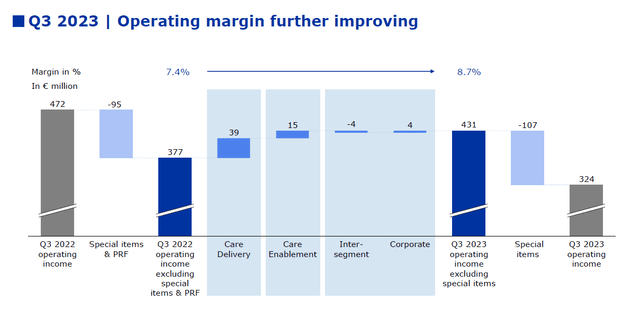

3Q23 noticed the corporate verify its upward trajectory. We’re speaking about continued natural development by each segments, continued remedy development, and profitable execution of the corporate’s turnaround plan.

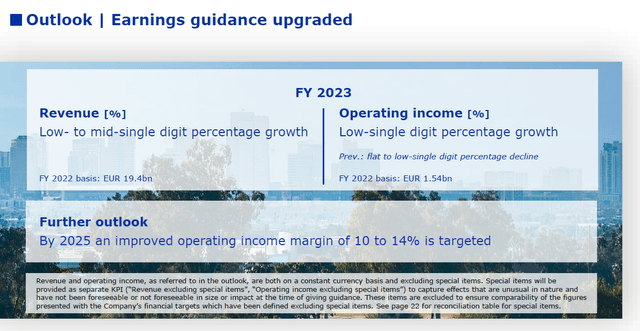

This has resulted within the 2025E financial savings and optimization targets being absolutely on observe right here. The corporate additionally raised its earnings outlook. These traits additionally absolutely mirror the traits occurring in my funding, Fresenius, which ultimately might even see some above-market returns that I’ve been anticipating for a very long time.

Natural development for the corporate was enabled by development in each of the segments, pushed by each quantity and value – and the corporate’s working revenue improved primarily based on higher efficiency, and expense administration whereas managing the damaging continued impacts from inflation and a non-recurring fee merchandise. Here’s a bridge for the working margin enchancment.

FMS IR (FMS IR)

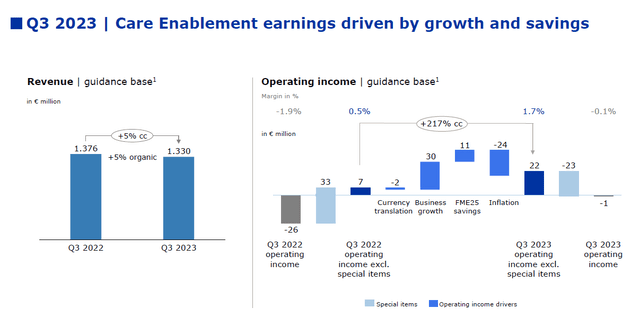

The underlying traits are what curiosity me right here. We’re speaking strong natural income development within the care supply phase, with constructive U.S. identical market remedy development when adjusted for exits from much less worthwhile contracts. The corporate has managed to mix enterprise financial savings and at last optimize its combine. Care enablement, the opposite sector, noticed higher gross sales of in-center disposables, machines, and residential merchandise as effectively, with constructive continued impacts from good pricing measures. The bridge right here is much more spectacular in its enchancment.

FMS IR (FMS IR)

The corporate nonetheless is not above common in something. When wanting on the sector of Healthcare firms, the issue we discover right here is that FMS nonetheless is pretty common, in each gross, working, internet margins, and many of the elementary KPIs when taking a look at profitability. The identical is true for fundamentals. Debt to EBITDA remains to be at round 4x, with an curiosity protection of sub-3x. Not the best pattern.

On the identical time, now we have good indicators for the corporate. The corporate’s top-line indicators are rising sequentially, which means that the corporate wants to enhance its working margins to actually result in some change right here – and that is precisely what FMS is now reporting.

Additionally, and necessary to recollect, that irrespective of the way you slice it, this firm remains to be fairly low-cost.

Worth is the only most necessary issue as soon as we decide that an organization is value investing in primarily based on the foundations of its enterprise mannequin – which I consider Fresenius Medical Care is.

FMS Enterprise mannequin (GuruFocus)

Once more, not probably the most environment friendly or engaging enterprise mannequin – at the very least not but – however undoubtedly the place I consider it to be “ok”.

FMS had a very good 2023 3Q – ok to the place the corporate raised its earnings steerage for the 12 months, which ought to present some help for the share value and valuation going ahead.

FMS IR (FMS IR)

Let’s take a look at what quantities to the corporate’s dangers and total upside right here.

Dangers & opsides for Fresenius Medical Care

I take into account this firm to have a no-nonsense upside right here for the long run, and have been undervalued – albeit for a very good motive – for a really very long time. Dangers to the corporate do exist, and a few of them are operational, not associated to macro. The corporate’s revenue combine is one thing to pay attention to as a result of nearly all the firm’s earnings come from business insurance coverage insurance policies. If the panorama for these insurance policies or how these are dealt with on a political scale adjustments, the potential affect on Fresenius’s income just isn’t insignificant. I do not see this as dire as some analysts do – I consider insurers can have an effect on these components, however a elementary downturn over a very long time is unlikely – however the danger exists. We have now some proof that pricing stress is coming – simply take a look at the comparatively latest Supreme Courtroom ruling towards DaVita.

On the upside, the corporate is closely diversified each in geography and enterprise combine, its home-treatment charges that are growing are going to result in higher margins (conceivably at the very least), and the corporate has a working enterprise capital arm and is investing in methods to deal with ESRD except for conventional instruments. Extra importantly, although, the corporate is surely and with out argument, at a really low-cost stage provided that its earnings have troughed.

Let’s take a look at the up to date valuation upside for the corporate.

Valuation for Fresenius Medical Care

This firm has been troughing for years. We have seen earnings decline since 2021, however the earnings development had slowed all the way down to near-zero in 2019. Shareholders of this firm have primarily been shedding cash since 2018 when the corporate was overvalued at nearly 18-20x P/E.

It is at present buying and selling at 16x normalized, however nearer to 10-12x if we account for a future earnings development.

Is Fresenius Medical Care the most effective firm you could spend money on right here?

I don’t consider that to be the case, no – however it’s a strong enterprise with a very good upside, and deserves highlighting for this reality.

You possibly can closely impair the corporate’s earnings to solely take a look at the final 5 years, normalize beneath P/E 15x at 14x, and nonetheless see a market-beating RoR and upside.

If the corporate’s forecasts materialize, which they do over 50% of the time for the previous decade, you are taking a look at nearly 20% annualized RoR with a 42%+ RoR in 3 years for this enterprise. For those who’re prepared to normalize the a number of at nearer to its 20-year common, which is eighteen.5x, that RoR goes as much as 33.5% per 12 months or nearly 80% in whole.

I nonetheless consider that Fresenius, with native ticker FRE, affords you a extra compelling combine and upside as a result of the estimates for the corporate are higher development, a greater combine, and never as concentrated revenues. Moreover, the decline in Fresenius SE & Co KGaA wasn’t as deep because it was within the medical care phase, FRE has higher fundamentals with a full BBB, and a yield of three.3%, quite than sub-3%.

So, total, Fresenius remains to be the higher choose right here, based on me – however FMS with medical care nonetheless constitutes a “BUY” right here.

I am not altering my goal for the corporate, and my up to date thesis for 2024E is as follows.

Thesis

I view FMS as an organization to purchase. It is a chief within the kidney care sector and owns massive elements of the dialysis operations within the US market in addition to on a world foundation. It is BBB-rated, has a suitable yield, and has a near-72% upside going ahead to the following few years. Nevertheless, as a result of company construction, governance, and the enchantment of its “father or mother”, I take into account Fresenius to be the superior funding if evaluating the 2. FMS is a “BUY”, and it has upside – however FSNUY/FRE has a greater thesis. I nonetheless view this as being the case. Nevertheless, the corporate is a really strong “BUY” right here – and the latest decline as a result of Ozempic trial outcomes doesn’t faze me within the least. I present you two explanation why this firm is definitely unlikely to see any type of affect as of this, at worst we’ll see some delays in remedies. The latest firm quarterly earnings report implies that I’m sticking to my value goal for the corporate, in addition to my stance – and I nonetheless take into account it “low-cost” regardless of not being as low-cost because it was again in October. I give FMS a PT of $34/share for the long run and fee it a “BUY”.

Keep in mind, I am all about :

1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly large – firms at a reduction, permitting them to normalize over time and harvesting capital features and dividends within the meantime.

2. If the corporate goes effectively past normalization and goes into overvaluation, I harvest features and rotate my place into different undervalued shares, repeating #1.

3. If the corporate does not go into overvaluation, however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed here are my standards and the way the corporate fulfills them (italicized).

This firm is total qualitative. This firm is essentially secure/conservative & well-run. This firm pays a well-covered dividend. This firm is at present low-cost. This firm has a sensible upside primarily based on earnings development or a number of enlargement/reversion.

As a result of the corporate fulfills each single one among my standards, it’s a “BUY” to me right here. I am speaking about each FMS and FRE right here, however this text is on FMS.

This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.

{kind=link}