William_Potter

Funding Thesis

Each firms agreed to half methods since China didn’t present regulatory approval on the acquisition, which implies that Tower Semiconductor (NASDAQ:TSEM) will proceed its operations independently. This non permanent setback is offering what I imagine is a very good alternative to spend money on a strong semiconductor firm that already has good financials in place, subsequently, I’m updating my ranking from “Maintain” to “Purchase” as I imagine the corporate might be simply advantageous in the long term by itself.

Approval Denied

So, I woke as much as the information which wasn’t too shocking to me however huge information for TSEM, not a lot so for Intel (INTC) as INTC inventory just isn’t budging pre-market. The information that Intel and Tower agreed to terminate the beforehand introduced merger resulting from what I believe is the continual geopolitical tensions between China and the US, which culminated in China blocking the deal altogether. That isn’t the end result present shareholders of TSEM have hoped for that’s for positive, nonetheless, it appeared that the writing was on the wall for a few months now and that was mirrored within the firm’s share worth dwindling YTD and is down round 33% if we embody the pre-market numbers.

With the termination of the deal, as per the settlement, Intel might be paying TSEM $353m in termination charges. There isn’t a date as to when that is going to be paid, nonetheless, this one-time money occasion will end in round $3.2 in EPS. It isn’t higher than a buyout at over $50 a share, nonetheless, it’s nonetheless higher than nothing. What this primarily means is the corporate will proceed to function because it has prior to now however simply obtained just a little bump in earnings one yr.

Outlook and Newest Quarter Outcomes

The final time I coated the corporate was in April after I seemed on the firm’s financials intimately, so be happy to have a learn right here. In the identical article, I seemed on the semiconductor sector in just a little extra element than I’ll right here. In that article, I additionally talked about that the corporate is barely too costly if the deal falls via and count on a ten%-15% drop on the information that the deal is useless, quick ahead to August sixteenth, within the pre-market, the corporate is at the moment down round 12% and round 38% because the first time I coated the corporate. I believe it’s time to re-evaluate.

The corporate just lately reported Q2 ’23 earnings, which beat consensus estimates however weren’t one of the best in my view, nonetheless, I wasn’t shocked concerning the outcomes both as a result of as I coated in April, I anticipated revenues to proceed to fall a short time longer due to the softness in demand and total detrimental sentiment within the semis sector. Revenues have been down round 16% y-o-y, gross revenue was down round 22% from the identical quarter a yr in the past whereas working revenue was down round 28% in comparison with the identical quarter a yr in the past. Internet revenue got here in at $51m or $0.46 a share in comparison with $58m Q2 ’22 and $0.53 a share (a drop of 12% y-o-y).

So, not the best outcomes, nonetheless, I used to be anticipating this to occur, so I’m not shocked. Sadly, the corporate has not been offering any steering for some time now due to the acquisition by Intel, nonetheless, now that the deal is useless, I might be listening intently to the corporate’s steering for subsequent quarter’s launch, which is scheduled someday in early November.

As for the broad semiconductor sector outlook, evidently a number of reviews level to a trough within the first half of ’23 with some indicators of progress within the second half of the yr obvious. This report suggests the continuation of headwinds for the remainder of the yr; nonetheless, we are going to see sturdy progress in most if not all segments of the semiconductor sector in ’24 and past, which bodes effectively for the way forward for TSEM.

Financials

I’ve coated the financials within the earlier article in additional depth by trying again at historic figures, so I received’t be repeating myself right here, nonetheless, I’ll take a look on the firm’s present state to see how effectively it’s nonetheless doing.

As of Q2 ’23, the corporate has round $912m in liquidity in opposition to $178m in long-term debt. Secure to say the corporate continues to be as robust as earlier than and is at no threat of insolvency. The corporate’s present ratio continues to be very excessive, and whereas it isn’t a foul factor, it’s above my acceptable efficient ratio of round 1.5- 2.0 as a result of this tells me that the corporate isn’t using its money pile very effectively. It might be utilizing that money to start out increasing its operations and be extra aggressive in it or reward shareholders with some share repurchases or another approach. I imagine now that the deal is off, the corporate will begin to develop its operations additional.

TSEM in my view continues to be a really robust firm financially, with loads of liquidity readily available and with little or no long-term debt, which suggests the corporate will proceed surviving the headwinds that we’re but to see within the subsequent half of the yr.

Valuation

I made some modifications to my 10-year DCF evaluation, and I’ll current two separate valuations right here. One might be with out the $353m one-time money cost to TSEM and one with.

I additionally assumed a -18% progress in revenues for each valuations in ’23, then a subsequent 15% progress in ’24, which is able to linearly develop down to five% by ’32, giving me round 7% CAGR for the following decade.

For the optimistic case, I went with 9% CAGR, whereas for the conservative case, I went with 5% CAGR for the following decade on each valuations.

Additionally, for each valuations, I left margins as I had them in April. Identical with the 25% margin of security. With that mentioned, if we embody the $353m in additional revenue on the finish of ’23, the corporate could be buying and selling for six.7x earnings of FY23 and total intrinsic worth could be $43.81 a share, that means there may be round 47% upside from the present (pre-market) valuation.

Intrinsic Worth with One time money cost (Writer)

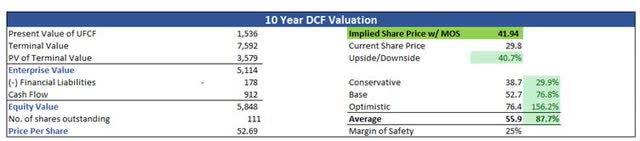

Now, if we do not embody the $353m, the intrinsic worth would nonetheless be $41.94 a share, implying a 40% low cost to truthful worth in response to my calculations.

Intrinsic worth with out one time money cost (Writer)

Closing Feedback

I don’t assume that is the top of the street for TSEM now that the deal is useless. The corporate will proceed to function as regular going ahead as an unbiased firm. I’d charge the corporate a powerful purchase proper now, nonetheless, I really feel like due to this short-term noise, the inventory worth could proceed its additional decline due to the information. I’m going to improve it from Maintain to Purchase as I imagine the danger/reward right here may be very attractive and additional declines in share worth solely assist the long-term investor to build up shares in a incredible firm like TSEM.

I might be opening a small place, to start with very shortly, and can welcome additional worth depreciation within the aftermath of the useless deal.

{kind=link}