Whereas synthetic intelligence (AI) is attracting buyers’ consideration, there’s one other large development they need to concentrate on: cybersecurity. Unhealthy actors have by no means had extra instruments, and the quantity of digital data that may be accessed can be rising. This is not a development that is going away, both; firms should guarantee they’ve top-notch safety or threat being the goal of a cyberattack, which might price hundreds of thousands and destroy confidence in an organization.

Because of this new actuality, the cybersecurity business is seeing a large increase. However with so many cybersecurity firms accessible to select from, it is simple to get misplaced. One firm is my clear selection, and it has the potential to turn out to be a a lot bigger pressure on this business.

CrowdStrike has turn out to be a prime decide within the cybersecurity house

CrowdStrike (NASDAQ: CRWD) is my prime decide within the cybersecurity house for a lot of causes. First, it is a light-weight cloud-native program. This implies it may be simply deployed to all endpoints in a enterprise community rapidly and does not take a lot bandwidth. Moreover, CrowdStrike has built-in AI into its product lineup since its launch.

In contrast to some firms that use AI as a buzzword, CrowdStrike’s platform is constructed on it. Its main product within the Falcon platform is endpoint safety. This protects community entry factors like laptops or cellphones from outdoors threats, and CrowdStrike makes use of AI to investigate exercise to know if it is regular or a risk. It will probably terminate entry to an organization’s server with out human intervention if it detects a risk.

It additionally has its Charlotte AI, a generative AI product. This enables customers to automate workflows, speed up investigation time, and cut back the quantity of talent required to turn out to be a cybersecurity professional. Primarily based on a buyer survey, Charlotte helps save round two hours per day by means of elevated effectivity.

CrowdStrike has a large product line that has slowly grown over the previous few years. As a substitute of getting to piece collectively cybersecurity options from varied distributors, CrowdStrike is working towards turning into a one-stop store for all cybersecurity wants. With merchandise in endpoint safety, cloud safety, id safety, risk intel, and extra, CrowdStrike covers many areas.

This technique has labored for CrowdStrike, as 64% of consumers make the most of at the very least 5 modules, and 27% make the most of at the very least seven. This exhibits loads of room for product enlargement amongst its consumer base, so upselling current prospects and signing new ones offers CrowdStrike two development avenues.

Story continues

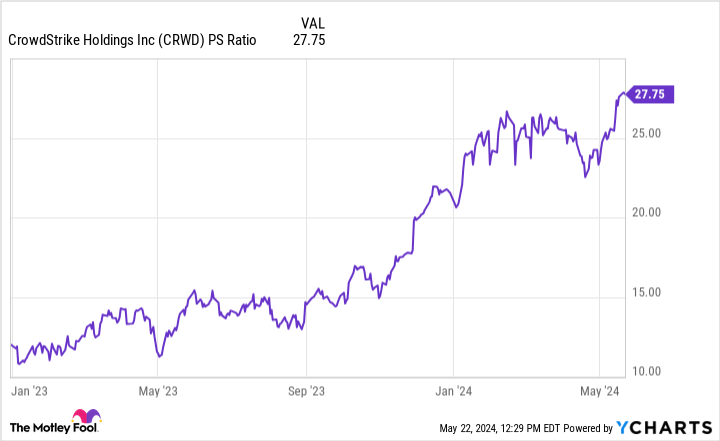

CrowdStrike’s inventory has gotten costly

Talking of development, CrowdStrike has been delivering glorious development for a while. Within the fourth quarter of fiscal-year 2024 (ending Jan. 31), its annual recurring income (ARR) rose 34% yr over yr to $3.44 billion. Trying ahead to FY 2025, CrowdStrike expects income development of 30% to just about $4 billion. Regardless of CrowdStrike getting bigger, its development is hardly slowing down, which is a testomony to the demand within the cybersecurity business and CrowdStrike’s prowess. Wall Avenue analysts even imagine it may possibly develop income at a 27% tempo in FY 2026 to over $5 billion.

CrowdStrike can be turning into more and more worthwhile every quarter.

So you’ve got bought an organization that’s an business chief in a quickly increasing discipline and has glorious financials. It looks as if a no brainer purchase, proper?

Buyers should additionally think about the value tag of the inventory. It is no secret that CrowdStrike is a wonderful firm, and its inventory is priced accordingly.

A worth of 28 occasions gross sales could be very costly, which is the first downside of CrowdStrike’s inventory. I am utilizing the price-to-sales (P/S) ratio as a result of CrowdStrike hasn’t reached most profitability but. To translate into the extra acquainted price-to-earnings (P/E) ratio, I will give CrowdStrike a man-made 30% revenue margin — an important purpose for software program firms like CrowdStrike.

With that revenue margin, CrowdStrike would have a P/E of 93 at as we speak’s costs. In case you make the most of analysts’ FY 2026 income projection of $5.03 billion, CrowdStrike would commerce at 56 occasions earnings.

That is too costly for a lot of buyers’ style, and I would not blame them for not shopping for at as we speak’s costs. Nonetheless, I would maintain CrowdStrike in your radar, because it’s too good of an organization to overlook about if the inventory worth drops to extra affordable ranges.

The place to take a position $1,000 proper now

When our analyst staff has a inventory tip, it may possibly pay to pay attention. In spite of everything, the publication they’ve run for twenty years, Motley Idiot Inventory Advisor, has greater than tripled the market.*

They only revealed what they imagine are the ten greatest shares for buyers to purchase proper now… and CrowdStrike made the listing — however there are 9 different shares you might be overlooking.

See the ten shares

*Inventory Advisor returns as of Might 13, 2024

Keithen Drury has positions in CrowdStrike. The Motley Idiot has positions in and recommends CrowdStrike. The Motley Idiot has a disclosure coverage.

This is My High Cybersecurity Inventory (and It is Not Even Shut) was initially revealed by The Motley Idiot