Matteo Colombo

Funding Abstract

Avid readers of this channel will know that we now have been scouring the fundamental supplies sector for 1) well-priced compounders, with 2) mouth-watering economics, and three) throwing off piles of free money circulation. Up to now, there have been a number of names that match this mould.

It’s not all rainbows and butterflies, nonetheless. Discovering firms that match this strict financial standards is tremendously troublesome and compounded by the truth that, oftentimes, all of a enterprise’s “excellent news” is absolutely embedded into present market expectations.

Within the seek for selective alternatives within the materials sector, we flip to the specialty chemical compounds trade. Right here, Worldwide Flavors & Fragrances Inc. (NYSE:IFF) has turn out to be a possible candidate for the fairness bucket.

Determine 1.

Tradingview by way of Searching for Alpha

The query is whether or not IFF is an investment-grade firm on the time of writing, and, if the value/worth equation is skewed to the upside. Based mostly on the info sample introduced right here, I don’t imagine the corporate is a compelling purchase on a danger/reward foundation, in comparison with related alternatives with an analogous degree of danger. In that regard, I price the corporate a maintain for causes said right here at the moment.

Background fundamentals

IFF is within the enterprise of producing and distributing substances for client well being and beauty merchandise. Its gross sales footprint is international. It accomplished a merger with the Diet & Biosciences (“N&B”) phase of chemical big DuPont in 2018. This was seconded by the acquisition of Frutarom Industries in the identical yr.

The corporate serves the meals and beverage markets alongside the well being, private care, and wellness markets. It additionally has area of interest publicity to enzymes, cultures, style texture, components, and probiotics, making it a extremely specialised operator for my part.

It operates throughout 4 segments, specifically:

Nourish – that is the corporate’s pure ingredient line, which sells to the meals & beverage, dairy, and bakery markets. You may consider issues like flavours and substances as the important thing end result for its prospects right here.

Well being and biosciences – this phase produces a portfolio of enzymes, meals cultures and probiotics for the meals and beverage trade. These find yourself in merchandise like fermented meals, yoghurts, cheeses, and so forth.

Scent-The scent enterprise produces fragrances and perfume compounds, that are then used as substances in “the world’s most interesting perfumes and best-known family and private care merchandise,” per the 2023 10-Ok. Part of this enterprise was the beauty ingredient operation, which administration divested from as of April 2024.

Pharmaceutical options – lastly, the pharmaceutical options enterprise is within the operation of seaweed-based pharmaceutical excipients. These are used to unlock the supply of pharmaceutical compounds – for instance, in using extended-release formulations.

Based in 1909, the corporate has not created substantial worth for its shareholders over the past 10 years or so, past its spectacular dividend development. I’m not stunned to see the corporate of this age buying and selling sideways. Furthermore, firms on this maturity cycle can nonetheless have mouthwatering economics.

In 2014, the corporate produced round $3.1 billion in gross sales on $601 million in working earnings. It had stretched this to $$3.9 billion in income by 2018, on roughly $607 million in working earnings. After finishing the N&B merger, the highest line has expanded considerably. Working earnings have not. As an example, in 2021, gross sales had been $11.7 billion – nearly 3x that in 2018 – however this was towards working earnings of $660 million, in-line. Final yr, it printed $11.5 billion on the high line, on working earnings of $612 million. Based mostly on this document, I query if the restructuring has added financial worth for the corporate’s buyers.

Q1 2024 financials

1. Key insights

The corporate put up $3 billion in quarterly revenues in Q1 2024, down 400 foundation factors yr over yr. It pulled this to adj. EBITDA of $503 million, down 15%. This compressed working margins by 300 foundation factors. Regardless of the pullback, administration retained full-year steerage and is projecting $10.8 billion to $11.1 billion in revenues this yr. It additionally means that product volumes will elevate 300 foundation factors on the higher finish of the vary, coupled with a circle 1% elevate in pricing. This consequence additionally bakes in a 3% to 4% foreign exchange headwind. Administration is eyeing $2.1 billion in adjusted pre-tax earnings on this.

As to the divisional breakdown, the nourish phase clipped 3% gross sales development to $1.5 billion on adj. working earnings of $216 million (up 13%). Well being and biosciences revenues grew 6% to $531 million, lifting pre-tax earnings by 21% to round $160 million. This was underscored by each quantity and productiveness positive aspects.

In the meantime, the scent and pharmaceutical options had been up 16% and down 11%, respectively. Administration famous that stock stocking within the pharmaceutical options enterprise continues to be a headwind that compressed adjusted working earnings by 22% yr over yr to $46 million. Lastly, it left the interval with complete debt of $10.3 billion towards money readily available of $764 million.

2. Appraisal

My view of the primary quarter outcomes from IFF was blended. Administration’s language on the decision was pretty muted, for my part, regardless of noting the “improved monetary and working efficiency” of the corporate. Within the slides, the ahead outlook says that “it’s nonetheless early, and uncertainty stays” regarding 2024.

This could possibly be administration being appropriately cautious, however I might nonetheless prefer to see some conviction concerning the place it intends to allocate capital shifting ahead. Fortunately, it has been clear on current makes use of of money. It talked about that it has lowered debt by ~$1 billion over the previous 12 months, bringing the leverage ratio to 4.4x by the tip of Q1. In the meantime, capital expenditures ran at 4% of gross sales within the quarter at $118 million, and it returned $207 million of capital to shareholders by its dividend.

Based mostly on this appraisal, it might seem 1) the funding runway for IFF is comparatively small, 2) alternatives exist solely to mine the acquisition pipeline, or 3) to reinvest into present operations for issues like efficiencies and manufacturing benefits.

Enterprise economics underlying maintain thesis

One benefit IFF enjoys being within the perfume and biopharmaceutical house is that these are extremely differentiated domains. This implies the corporate ought to usually be capable of promote its choices greater than trade averages and luxuriate in some type of client benefit (particularly within the perfume house).

We see this when evaluating IFF to the specialty chemical compounds trade. The corporate has round 350 foundation factors greater gross margins (indicating the upper promoting costs) however has greater than common working margins too (Determine 2).

This is able to counsel it has decrease working prices as a share of revenues and, for my part, squares off with the economics of the enterprise: (i) It’s a diversified operation conducting enterprise throughout distinct segments, (ii) acquisitions are one main means to development, which means (iii) it could actually amalgamate working prices of its numerous belongings by “synergies”.

Given the extremely intangible nature of the enterprise’s invested capital, I’m not stunned to see a aggressive benefit in free money circulation margin both – 17.4% in comparison with the trade median of 6.8% – incremental capital necessities must be comparatively low, with investments reserved for issues like acquisitions and upkeep expenditures.

In that respect, it’s fairly stunning that this firm produces such small post-tax earnings relative to the capital employed within the enterprise. That is an trade the place substantial capability exists, and plenty of operators incur the commodity-like economics I prefer to keep away from. Presumably, IFF would profit from this, given its completely different differentiated merchandise in fragrances and so forth. A minimum of, that is what I had assumed initially.

Determine 2.

Firm filings, Creator

This can be a basic case of why one merely can not assume in capital markets and fairness evaluation. I wished to grasp why FF runs such an intensive, unprofitable enterprise (profitability is measured right here, not by way of internet margins, earnings per share, or development – it’s measured within the context of internet working revenue towards invested capital, in any other case, return on invested capital).

Determine 4 illustrates the web working revenue after tax IFF has produced on capital invested within the enterprise and free money circulation left over after contemplating all reinvestment wanted to keep up its aggressive place. It does this on a rolling 12-month foundation.

As noticed, the corporate has wound again complete capital in danger within the enterprise from $142 per share in September 2021 to $102 per within the final 12 months. Towards this, the corporate has grown put up tax earnings from $4.90 per share as much as $5.12 per share within the trailing 12 months, a 5% ROIC. All dividends paid up; this tallies $9.80 per share, a trailing yield of 10.2% as I write.

The consequence has been lower than 5% to six% rolling returns on capital every interval. Evaluation of the drivers of this slack return is revealing. It enjoys moderately excessive post-tax margins of 10%. This squares off with the economics I outlined earlier, within the client benefits it has with branding and specialty merchandise with comparatively quick product cycles.

Nonetheless, on the $26.1 billion of capital employed into this enterprise, the ratio of gross sales to capital is simply 0.43x, indicating that for each $1 invested into the enterprise, solely $0.43 in revenues return.

Mentioned one other approach, the funding required to provide one greenback of revenues is tremendously excessive, indicating this can be a capital intensive train.

Determine 3.

Firm filings, Creator

Objectively, the present trailing free money circulation is engaging. It’s also one which the corporate is more likely to keep, for my part. Determine 5 exhibits the trailing free money for yield IFF has carried out enterprise on over the past three years, on a rolling 12-month foundation. Traders have been in a position to buy the corporate at a number of factors alongside this horizon at a >6% trailing free money for yield.

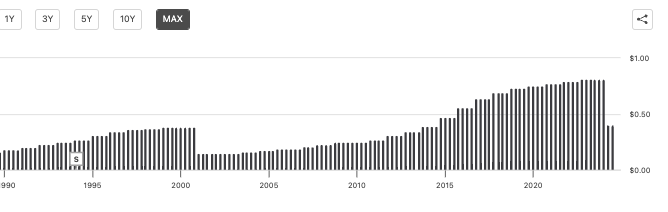

Right here is the place the worth is on this identify for my part. This money circulation helps a gentle stream of dividends which have elevated consecutively for 21 years, and been paid consecutively for 34 years (Determine 6).

That is actually one for consideration for income-oriented buyers. For my part, with the mixture of 1) incremental capital necessities and a couple of) IFF’s sheer dimension, buyers can anticipate hearty dividends in years to come back. This can be a balancing issue within the funding debate.

Determine 4.

Firm filings, creator

Determine 5.

Searching for Alpha

As for the financial worth – that’s, the propensity for capital appreciation – my views flat for IFF. That is constructed on the premise administration will not be creating financial worth for shareholders within the first place.

I measured this because the return on invested capital relative to a hurdle price, on this occasion, 12%, measuring the long-term market averages. Something above this 12% price is an financial revenue, and vice versa. Making use of this benchmark to the corporate’s earnings exhibits it has not elicited financial revenue throughout the testing interval (Determine 7).

As an example, within the 12 months to March 2024, we would have liked internet working revenue after tax of $3.1 billion on invested capital of $26.1 billion. The corporate produced $1.3 billion as an alternative, inflicting an financial lack of $1.8 billion, or $7.15 per share. Over the interval proven, administration has produced an financial lack of $23.8 billion. On the similar time, IFF’s market worth has decreased by $14.5 billion – unsurprising when benchmarked towards financial worth added.

Determine 6.

Firm filings, creator calculations

Projections of worth at regular state of operations

To grasp the intrinsic worth of IFF and the enterprise belongings’ price, I’m going to analyse how administration has been working and rising the enterprise over the previous three years. Determine 8 illustrates administration’s capital allocation choices from 2021 to 2024 on a rolling 12-month foundation. It then compares this towards the monetary efficiency over this time. I’ve additionally included all acquisition exercise beneath the funding drivers.

As noticed, to create a brand new greenback of revenues, the corporate has invested most of its out there funds in the direction of working capital, however lowered capital density in acquisitions, fastened belongings and intangibles. This has adopted key divestment over the current years. For my part, it might be unreasonable to imagine this pattern may proceed over a 5 or ten-year interval. The corporate does shed capital by dividends, however it does want working belongings to provide free money circulation within the first place. I’ve subsequently revised my assumptions to these proven in Determine 9.

Determine 7.

Firm filings, creator calculations

Right here, I presume {that a} new greenback in revenues would require a $0.05 funding to fastened capital and acquisitions. I imagine this can be a honest set of assumptions because it aligns with newer tendencies of incremental funding noticed within the final 12 months, and elements in expenditures at a price of 4% of gross sales (consistent with Q1 2024).

Determine 8.

Creator’s calculations

The projections constructed from this mannequin are proven in Determine 10, beneath. I’ve carried the common tax price of 16.3% ahead by the sequence as nicely.

My numbers have the corporate to provide round $11.8 billion in gross sales this yr, forward of consensus estimates of $11.16 billion. These estimates have the corporate to throw off anyplace from $1.12 billion to $1.17 billion in free money circulation over this time, with capital turnover of 0.4x and tax margins above 10%. Below these assumptions, I estimate the corporate may examine its intrinsic valuation at round 140 foundation factors every quarter. As mentioned in additional views on valuation beneath, this isn’t a compelling image.

Determine 9.

Creator’s estimates

Valuation

The inventory sells fairly expensively to the sector at 26x trailing non-GAAP earnings and 55x EBIT. It additionally sells at 1.7 instances the web belongings employed within the firm, and this tight a number of is right for my part, given the negligible returns on tangible capital. Instantly, I’m suspicious of this valuation, as I have never recognized administration as creating substantial financial worth – solely by the persistent stream of dividends. This isn’t mirrored in multiples of earnings or belongings.

Furthermore, you’ll have simply seen the corporate sells at a better value relative to the earnings of the enterprise, however a low value relative to the belongings of the enterprise, telling me there’s a dislocation available in the market’s views on productiveness of the agency’s capital.

To get a way of whether or not these multiples are honest or not, I’ve projected my estimates of free money circulation out over the following 10 years and discounted them again on the 12% price to reach at a gift worth at the moment. I’ve blended this with a view on intrinsic valuation that appears on the estimated return on capital and reinvestment charges. I’ve carried out this throughout two eventualities, one with the regular state of operations, and one with the revised assumptions listed earlier. Right here, I get a valuation vary of $78-$82 per share, starting from 18-20x earnings. This helps a impartial view, for my part.

Determine 10.

Creator’s assumptions

Determine 11.

Creator’s assumptions

I additionally wished to evaluate the sensitivity of the valuation to adjustments within the P/E a number of and earnings development.

If administration does hit the projected development numbers of 20% in EPS this yr, and the P/E a number of doesn’t change, then the corporate is price $108 to us at the moment, a marginal upside on the place it sells as I write.

The difficulty is, nonetheless, if the a number of contracts all the way down to, say, the sector median of 16x, even when it hits the stipulated development charges, implied valuation drops to $64 per share. Equally, if it misses, however buyers proceed to pay this a number of, it’s price round what we pay for it at the moment, illustrating how a lot the valuation is tight as much as the P/E a number of versus the corporate’s fundamentals. This helps a impartial score, for my part.

Determine 12.

Creator

Briefly

IFF has an intensive historical past of accelerating dividends and increasing its footprint within the specialty chemical compounds trade. It enjoys a number of aggressive benefits relative to friends in pricing and on the patron aspect. Nonetheless, these are balanced by the enterprise economics at present, producing lower than 5% returns on capital. The free money flows it could actually throw off are, due to this fact, not of a fantastic sufficient magnitude to warrant the present valuation, for my part. Fee maintain.

{kind=link}