Userba011d64_201/iStock through Getty Photographs

DocuSign (NASDAQ:DOCU) reported higher than anticipated first fiscal quarter outcomes, which have been launched on June 6, 2024. The e-Signature chief reported slowing top-line progress, which was anticipated, and in addition revealed persistent dangers to its greenback web retention price, a key efficiency metric for software program corporations. Though DocuSign is dealing with challenges by way of buyer monetization, I imagine the e-Signature firm could possibly be a gorgeous funding resulting from its robust free money flows and excessive margins. Within the first fiscal quarter, DocuSign achieved but once more a 30%+ free money movement margin and whereas shares will not be a very cut price, I imagine it’s price holding on to shares of the e-Signature firm.

Earlier ranking

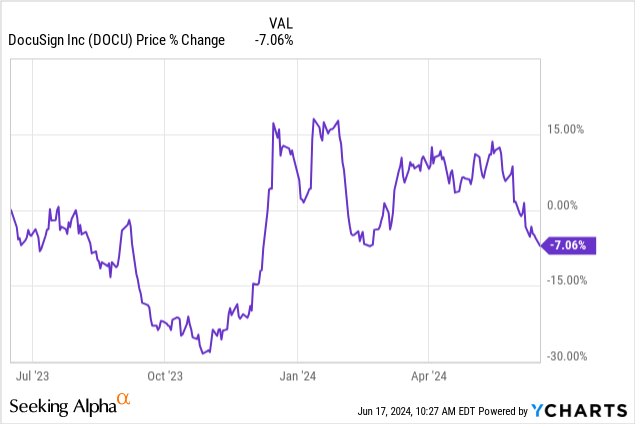

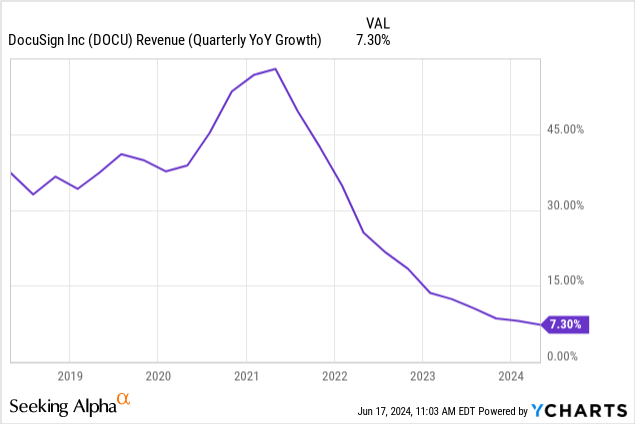

I rated shares of DocuSign to carry in November 2023 resulting from persistent greenback web retention dangers and weakening buyer monetization, which has principally performed out the best way that I predicted. Within the first fiscal quarter, DocuSign generated solely 7% top-line progress, extending its streak of successively slowing income progress, partly as a result of clients are extra discriminatory with their software program spending. Nonetheless, DocuSign is exceptionally free money movement worthwhile, which limits the draw back, for my part.

DocuSign beat the Road’s expectations for FQ1’25

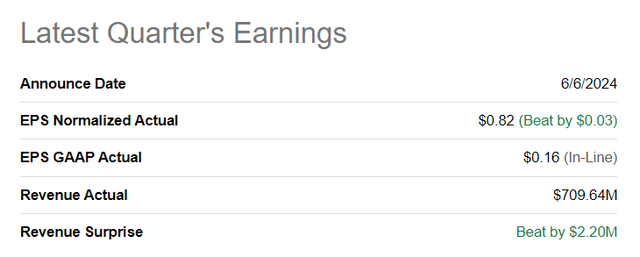

The e-Signature chief reported first fiscal quarter earnings at the start of June, which resulted in a prime and bottom-line beat: DocuSign had $0.82 per-share in adjusted earnings on revenues of $710M. Earnings beat by a small margin of $0.03 per-share, whereas revenues got here in additional than $2M above consensus expectations.

Searching for Alpha

DocuSign’s core worth proposition and greenback web retention dangers

DocuSign’s core product providing is its e-Signature answer that enables its clients to decentralize settlement processes and shortly and cost-effectively signal contracts and agreements between a number of contract events. DocuSign additionally presents complimentary providers that permit corporations to streamline enterprise processes, comparable to contract lifecycle administration, which helps corporations to maintain observe of contracts and customise agreements on the click on of a button.

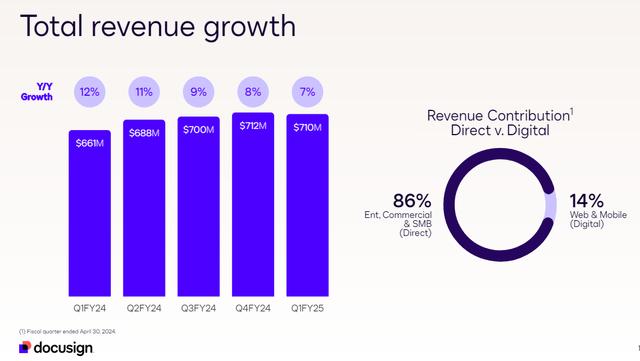

DocuSign generated $710M in revenues within the first-quarter, exhibiting a year-over-year progress price of seven% which marked the fourth straight quarter of income deceleration for the software program firm within the final yr. The excellent news is that DocuSign’s buyer base continues to be rising – the software program agency had 1.56M clients on its platform, exhibiting an 11% year-over-year progress price.

DocuSign

On the similar time, there are income dangers for DocuSign and these dangers have been mirrored in a moderating top-line progress, particularly because the pandemic.

DocuSign’s drawback is that current clients spend much less cash on the platform. This spending will be measures by a determine referred to as greenback web retention, which is measures how shortly a software program firm is rising its revenues organically. Prior to now, DocuSign’s dollar-based web retention price has fallen, and web retention dangers particularly have been a motive why I adopted a maintain ranking for shares of DocuSign in This autumn’23.

In the newest quarter, DocuSign’s dollar-based web retention price was 99%, exhibiting a 1 PP enhance over the earlier quarter. Nonetheless, a retention price beneath 100% nonetheless signifies that clients will not be rising their spending, which can stay a danger for DocuSign going ahead. Provided that DocuSign have been to develop its dollar-based web retention to a price of 100% or, ideally, increased than I might, I think about a ranking improve to purchase.

Sturdy free money movement offsetting retention dangers

DocuSign is a really free money flow-profitable software program firm and generated $232M in free money movement simply within the final quarter. From a margin perspective, DocuSign is doing nicely regardless of dealing with downward stress on its income progress and web retention price: the corporate saved 33 cents for each greenback it introduced in free money movement within the first fiscal quarter. Whereas the free money movement margin did not change a lot on a year-over-year foundation (+1 PP Y/Y), DocuSign nonetheless squeezed out 8% Y/Y free money movement progress.

$ in M

Q1’24

Q2’24

Q3’24

This autumn’24

Q1’25

Y/Y Progress

Complete Income

$661

$688

$700

$712

$710

7%

Free Money Move

$215

$184

$240

$249

$232

8%

Free Money Move Margin

32%

27%

34%

35%

33%

–

Click on to enlarge

(Supply: Creator)

DocuSign’s valuation

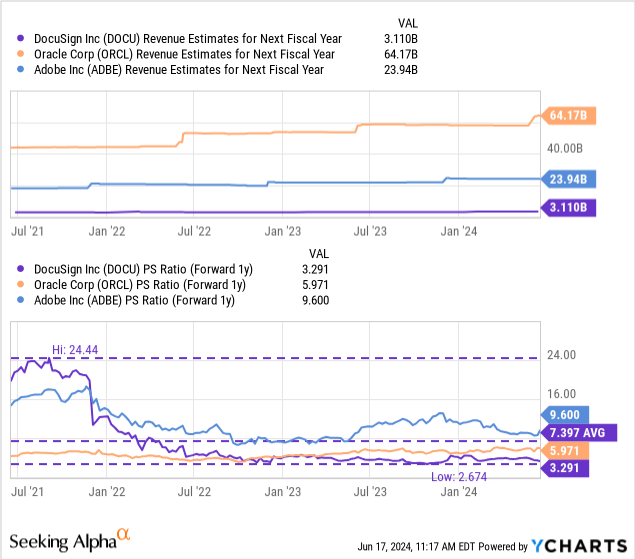

DocuSign’s shares are valued at a P/S ratio of three.3X, which is considerably beneath the corporate’s long run price-to-revenue valuation common of seven.4X. Shares have been valued extremely prior to now, particularly throughout the pandemic, however with slowing top-line progress, buyers have additionally reevaluated DocuSign’s valuation issue. Different software program corporations with comparable software program presents, like Adobe (ADBE) and Oracle (ORCL) have a lot increased valuation ratios, however these corporations have longer working histories, are additionally worthwhile on a web earnings foundation and are rising sooner.

Adobe is predicted to develop its prime line 13% in FY 2025 in comparison with 11% for Oracle and 6% for DocuSign. I imagine shares of DocuSign may commerce on the business common P/S ratio of 6.3X in the long run, however solely underneath the situation that the corporate improves its retention price and advances its product provide to such an extent that the corporate advantages from stronger income progress. If DocuSign traded on the business P/S ratio of 6.3X, shares may have a good worth of as much as $95.

Dangers with DocuSign

There are two main dangers that I see with DocuSign. The primary pertains to its slowing top-line progress price and the second associated to the corporate’s greenback web retention dangers, which signifies the potential for destructive income progress. If clients proceed to gradual their spending on the DocuSign platform, there’s a actual probability that the corporate’s top-line progress will fall into the low-single digits within the close to future. Provided that DocuSign managed to reverse its dollar-based web retention pattern in a sustainable method (at the very least three consecutive quarters of retention progress with a price above 100%), then a ranking improve could also be justified, for my part.

Closing ideas

DocuSign continues to see slowing income progress which is, partly, associated to weakening buyer monetization for the software program firm, as proven by a greenback web retention price of 99%. DocuSign, nevertheless, is sort of worthwhile on a free money movement foundation and delivered stable FCF margins within the final quarter. To a sure extent, DocuSign’s excessive FCF margins offset weak point in buyer monetization, for my part, and due to this fact the agency’s draw back potential may be restricted. I may solely conform to a ranking improve to purchase if DocuSign have been to make enhancements by way of buyer monetization and its greenback web retention price. If it achieves that, I imagine shares may revalue increased comparatively shortly. So long as that does not occur, nevertheless, I’ll affirm my maintain ranking for DocuSign’s shares.

{kind=link}