rocketegg/E+ through Getty Photos

Introduction

Most that observe my work right here on Searching for Alpha most likely know I make investments with the intention to carry for an extended time frame. Sadly, it does not all the time work out that manner for no matter purpose.

I am positive different traders can relate. I consistently preach a top quality over amount strategy, however understand each investor has a unique aim on their funding journey. Some components play an enormous half on this, like age, and funding technique, and many others.

Just lately, I got here throughout a BDC that though I would not essentially put them up there within the high-quality class, it has the potential makings of a fantastic play for traders looking for revenue now. On this article, I listing 3 the explanation why Nice Elm Capital Company (NASDAQ:GECC) could possibly be a fantastic portfolio addition for traders looking for revenue within the brief to medium time period.

Why Earnings Now?

Just lately, I obtained a message in my inbox from a reader and follower of mine asking for my recommendation on two shares. One was a favourite REIT and present holding of mine, CareTrust REIT (CTRE); one which I believe is a good long-term funding on account of their development potential.

The opposite was Common Well being Realty Earnings (UHT); one which I believe is a good revenue play for these looking for revenue now. And that is one thing I instructed them once they inquired. I knew they had been older, so my query to them was, “Are you looking for revenue now or later?” I figured I knew their reply, and after cautious consideration, they made their alternative. Searching for revenue now.

I do know there are many older traders right here on Searching for Alpha who’ve a shorter time span compared to somebody like me who simply turned 40 just a few months in the past. An individual’s age performs an enormous function of their funding journey for apparent causes. Relying on various factors reminiscent of race, gender, and geography, an individual’s life span differs.

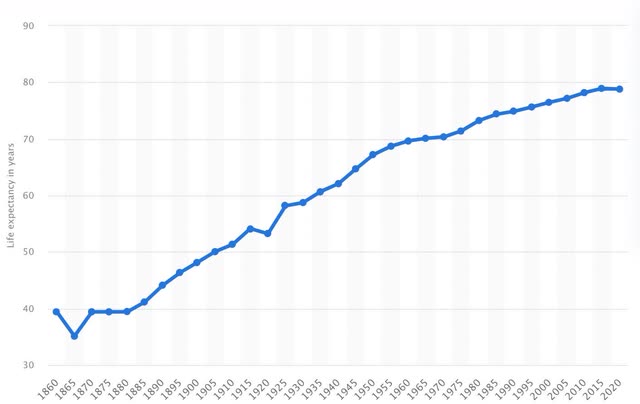

As demonstrated by the chart under, the common life span for individuals within the U.S. is roughly 80 years, and this has steadily elevated over time. However like most issues, this fluctuates periodically. So, in the event you’re older, in your 60s or 70s, it is possible you are searching for revenue now. In case you’re youthful, say 40 or (youthful), you possible have an extended funding horizon. And when searching for potential investments, that is possible a forethought when making your resolution.

Statista

Who Is Nice Elm Capital Corp?

GECC is an externally-managed BDC on the smaller facet with a market cap lower than $100 million. The corporate additionally has a shorter observe file having IPO’d in 2016. They concentrate on producing revenue with investments in company credit score & specialty finance.

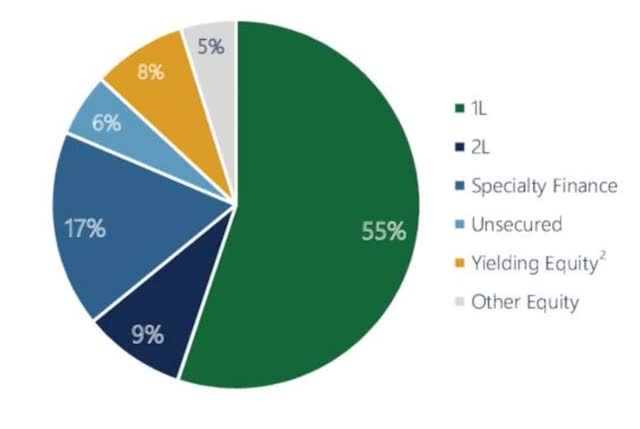

On the finish of their most up-to-date quarter, their portfolio’s honest worth stood at roughly $263 million. This consisted of 58 investments (45 debt, 13 fairness) in 45 corporations throughout 25 industries. Most of those had been in two segments, Chemical compounds and Transportation Gear at 11.3% and 10.6% respectively.

Motive #1 Portfolio Enhancements

Nice Elm Capital reported their first quarter earnings on Could third lacking analysts’ estimates on each it is prime & backside traces. Web funding revenue of $3.2 mil or $0.37 got here in roughly 9.8% under the $0.41 consensus. Whole funding revenue of $8.9 million additionally missed estimates, though a smaller miss at 2.5%.

This was as a result of write-down of illiquid investments in two corporations. To be honest, these had been originated previous to new administration taking up. Furthermore, this might affect future the BDC’s backside line or stability sheet if further write-downs happen within the foreseeable future.

NII additionally suffered a drag from the timing of money flows and the elevated share rely, in addition to newly made investments, mentioned later. This additionally adversely impacted their NAV, which declined by 3.2% from the prior quarter. So, not so nice begin for the BDC. Nevertheless, trying over an extended time frame, the BDC did make some enhancements.

Though web funding revenue was flat year-over-year at $0.37, it did barely enhance to $3.2 million from $2.8 million in Q1’23. Whole funding revenue additionally grew over the identical interval from $8.4 million to $8.9 million. NAV elevated from $11.88 to $12.57. So, on an annualized foundation, GECC noticed some enhancements, indicating a strong efficiency contemplating the difficult macro surroundings.

Through the quarter, in addition they managed to deploy extra capital than the earlier 12 months. Throughout Q1, administration invested $64.2 million throughout 29 investments, a major enhance from the $46 million deployed within the first quarter the 12 months prior. GECC additionally managed to develop their portfolio’s complete worth from $225 million on the finish of 2022.

In addition they continued to enhance their portfolio by rising their first-lien publicity. Of the 29 new investments, greater than half had been first-lien, senior-secured debt.

This introduced first-lien publicity to 64.2%. That is compared to one other small cap BDC, Monroe Capital (MRCC) whose first-lien publicity stood at 82%. Nevertheless, GECC’s administration has been making good investments rising their first-lien publicity, placing them in a greater place to navigate future downturns ought to they come up.

GECC investor presentation

Moreover, their exterior supervisor, Nice Elm Group (GEG) has a major possession stake within the firm, giving them a aggressive benefit over a few of their smaller friends. This not solely signifies confidence within the enterprise construction, however that administration has a vested curiosity in rising the corporate and maximizing worth for shareholders for the foreseeable future.

Motive #2 Strengthening Steadiness Sheet

Other than rising their first-lien publicity and making portfolio enhancements previously 12 months, GECC additionally strengthened their stability sheet by lowering their debt. Their complete debt decreased from roughly $151 million within the first quarter of 2023 to $148.1 million. At quarter’s finish, their leverage stood at 1.25x, down from 1.67x a 12 months in the past.

And though that is above the sector common 1.16x, administration has been making a concerted effort to additional strengthen the stability sheet to capitalize on future investments. Moreover, they raised capital by issuing shares at NAV earlier this 12 months. This was for a further 1.85 million shares for $24 million in proceeds.

In addition they issued $34.5 million value of senior notes, rising their liquidity & scale for future funding alternatives. These had an rate of interest of 8.5% due in June 2029. In addition they had money & cash market securities totaling $9 million and $20 million out there on the revolver.

They do have roughly $46 million value of debt due within the subsequent 6 months. This had an rate of interest of 6.75%, which they are going to possible get to refinance at a decrease fee. After that, the BDC has no extra debt maturing till a 12 months and a half later with $57.5 million maturing in June. This had an rate of interest of 5.875%. So, from a stability sheet standpoint, GECC’s will not be nice however not horrible both.

Motive #3 Dividend Protection/12 months-Finish Particular

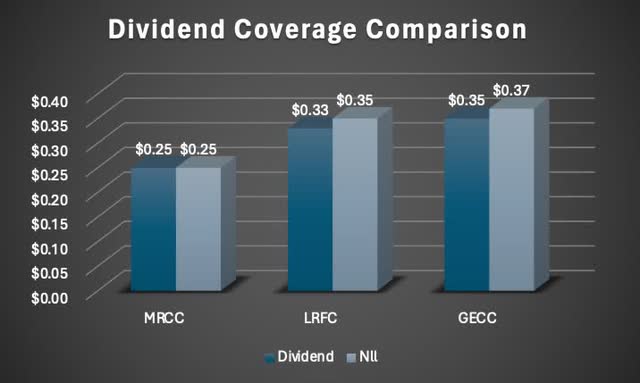

The ultimate and doubtless an important metric for revenue traders is the corporate’s dividend protection. With web funding revenue of $0.37, this marked the fifth consecutive quarter GECC lined its base dividend.

This gave them protection of 106%. And though I wish to see my holdings with greater protection, GECC’s protection was greater than its peer Monroe Capital, who had protection of 100% throughout its newest quarter.

Logan Ridge Capital (LRFC), one other smaller cap BDC, had the identical protection of 106%. Some traders could also be apprehensive about GECC’s tighter dividend protection compared to among the extra widespread and bigger BDCs like Ares Capital (ARCC) and Capital Southwest (CSWC), however administration expects this to enhance within the coming months.

Writer creation

Regardless of NII anticipated within the upcoming quarter to be just like Q1, administration expects this to choose up within the later a part of the 12 months as a result of anticipated ramp-up in distributions of their JV portfolio.

That is from their CEO throughout Q1 earnings:

With the anticipated ramp-up in distributions from our JV within the again half of the 12 months, coupled with revenue from the prudent deployments from the capital raises in 1Q & 2Q, we anticipate NII within the second half to meaningfully outpace the primary half. Consequently, we consider we stay well-positioned to proceed overlaying our dividend and we consider our Board will likely be in place to guage a particular distribution once more round year-end.

As beforehand talked about, GECC’s administration has been making concerted efforts to enhance their total portfolio high quality. I additionally anticipate administration to ship on rising their financials within the again half of the 12 months as M&A exercise possible picks up on account of decrease rates of interest.

In addition they anticipate receiving distributions from their current CLO JV funding beginning subsequent quarter, as per their CEO throughout earnings. So, for these searching for revenue within the brief to medium time period, GECC could possibly be a fantastic play to construct different positions in your portfolio.

Dangers & Valuation

Other than non-accruals, which ticked up throughout Q1, bringing the whole to $4.7 million of their portfolio’s honest worth, one other danger is the corporate’s smaller dimension. On the time of writing, Nice Elm Capital’s market cap was roughly $95 million. For these wanting dependable revenue, GECC could also be thought-about too dangerous. Moreover, they’ve very low buying and selling quantity with a median quantity of 17.4k. So, that is one thing traders ought to pay attention to earlier than investing in GECC.

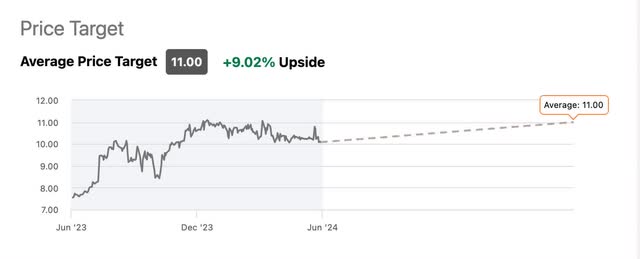

Over the previous 12 months, GECC is up greater than 33% from $7.55 a 12 months in the past, which could possibly be a results of their portfolio & stability sheet enhancements in addition to greater rates of interest. Regardless of this, the BDC nonetheless trades at an almost a 20% low cost to their NAV. That is greater than their 3-year common of 16.2% indicating they could possibly be undervalued. Wall Road additionally has them providing some upside to their worth goal of $11 a share. Nevertheless, I anticipate them to commerce close to this vary for the brief to medium-term.

Searching for Alpha

Moreover, I agree with Wall Road’s present maintain score and would contemplate upgrading them to a purchase if web funding revenue improves within the again half of the 12 months together with their leverage and total portfolio credit score high quality.

Backside Line

Nice Elm Capital has been enhancing their portfolio in addition to their stability sheet, placing themselves in a greater place to navigate future headwinds and proceed capitalizing on engaging funding alternatives.

For traders searching for revenue within the brief to medium-term, GECC might current a gorgeous alternative presently as they commerce at a reduction to NAV, possible a results of their smaller dimension.

Furthermore, their enhancing fundamentals and strong dividend protection may make GECC a possible funding for the long run. However on account of their smaller dimension and unproven observe file making them a riskier funding, I presently fee the BDC a maintain.

Editor’s Observe: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.

{kind=link}