Tempura/E+ through Getty Photographs

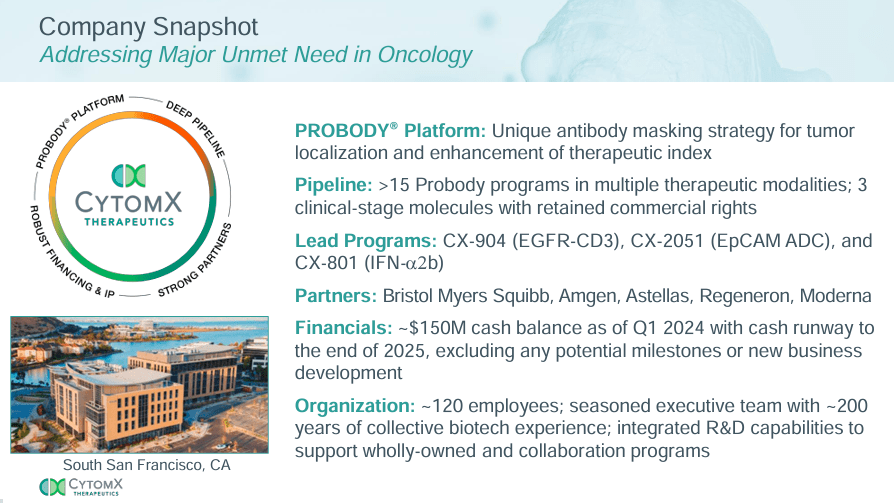

CytomX Therapeutics, Inc. (NASDAQ:CTMX) is a biotechnology firm that develops progressive oncology remedies utilizing its proprietary Probody platform. CTMX’s Probody creates inactive, conditionally activated biologics till they attain the tumor microenvironment, thereby rising drug effectivity and decreasing systemic toxicity and unintended effects. The Probody platform is CTMX’s crown jewel IP that generates drug candidates, enabling strategic partnerships with main corporations reminiscent of Amgen (AMGN), Astellas (OTCPK:ALPMY), Regeneron (REGN), Bristol Myers Squibb (BMY), Merck (MRK), and Moderna (MRNA). Whereas I settle for CTMX’s potential, its quick money runway and dilution dangers can’t be ignored. Thus, I take a impartial stance on the inventory, ranking it a “maintain” for now.

Probody: Enterprise Overview

CytomX was established in 2008 as a clinical-stage biotechnology firm headquartered in San Francisco, California. It develops activated biologics for oncology primarily based on its proprietary platform, Probody. This method permits a mechanism for inactive biologics till they attain the tumor’s microenvironments, rising drug efficacy and decreasing secondary results. I contemplate CTMX’s Probody platform its primary worth driver and the inspiration for its product pipeline and partnerships. At the moment, CTMX’s pipeline contains CX-904, CX-2051, and CX-801. It additionally presents a number of preclinical medication developed with corporations leveraging its progressive Probody platform, together with T-Cell Bispecifics [TCBs] with Astellas, mRNA packages with Moderna, interferon-alpha 2b immune modulator research with Merck, and T-cell engagers with Amgen.

Supply: Company Presentation. June 2024.

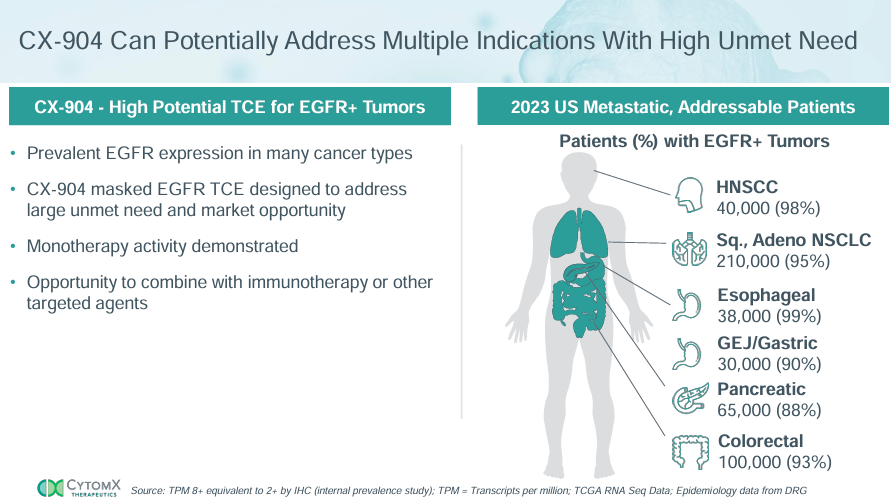

Furthermore, CX-904 is a bispecific antibody that targets epidermal development issue receptor [EGFR] on tumor cells and CD3 on T cells. This method directs the immune system to assault EGFR-positive most cancers cells. CX-904 is a section 1a drug, with anticipated dose escalation outcomes by yearend 2024. This drug is being developed in partnership with Amgen (AMGN).

In January 2023, CTMX earned a $5 million milestone for this drug when it was nominated for scientific improvement. Then again, CX-2051 is a section 1 drug and CTMX’s totally owned antibody-drug conjugate [ADC] that binds to the epithelial cell adhesion molecule [EpCAM]. EpCAMs are overexpressed proteins in colorectal, breast, and prostate cancers. CX-2051’s ADC combines with a cytotoxic payload, killing cancerous cells. Preliminary information is anticipated by early 2025.

Supply: Company Presentation. June 2024.

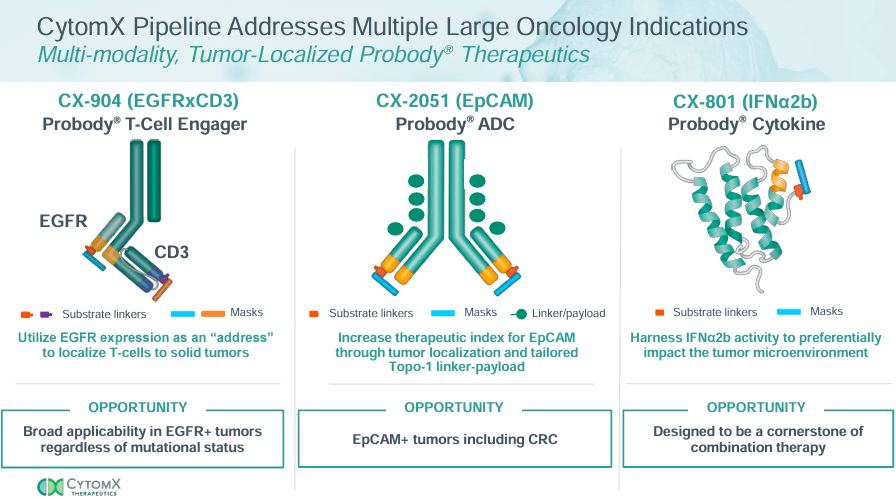

Lastly, CX-801 is a preclinical drug initially developed solely by CTMX. Nevertheless, on Could 7, 2024, CTMX introduced a collaboration with Merck to judge CX-801 together with Keytruda (pembrolizumab). CX-801 is a conditionally activated interferon-alpha 2b [IFNα2b], a cytokine that enhances immune cell exercise to eradicate tumor cells. This inhibits viral replication inside cells and modulates immune-related gene expression. Thus, CX-801 prompts particularly inside tumors, bettering efficacy and security. CTMX and BMY use Probody to create conditionally activated biologics with potential oncology use circumstances. Nevertheless, in March 2024, BMY withdrew from the partnership targeted on creating checkpoint inhibitors for most cancers immunotherapy. The product in query was BMS-986288, a section 1/2 drug.

CytomX’s Partnership and Blended Trial Outcomes

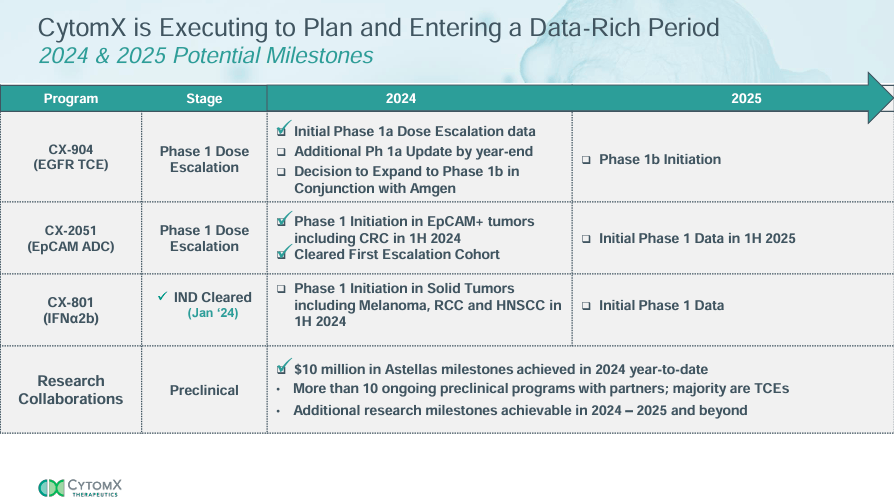

BMY’s inner portfolio revision finally discarded this program, considerably impacting CTMX, because it diminished potential milestone funds by $300 million. Nonetheless, BMY and CTMX proceed collaborating on T-cell engagers with a number of preclinical packages, with potential milestone funds now diminished from $2.1 billion to $1.8 billion after BMS-986288 was discontinued. Then, on Could 9, 2024, CTMX’s inventory value declined after Q1 2024 outcomes, together with CX-904’s preliminary section 1a outcomes co-developed with Amgen. The trial enrolled 35 sufferers with superior stable tumors, receiving a median of 4 prior remedy strains, and evaluated the variety of sufferers with dose-limiting toxicities as the first endpoint.

Supply: Company Presentation. June 2024.

Whereas CX-904’s security profile appeared favorable (most unintended effects had been grade 1), the secondary endpoint confirmed combined outcomes. CX-904’s response price, period of response, progression-free survival, disease-control price, and total survival confirmed a 33% partial response [PR] in six evaluable pancreatic most cancers sufferers. All six sufferers achieved illness management (i.e., goal response). One affected person at a 6 mg dose skilled an 83% tumor discount, and a second affected person at a 5 mg dose had a 51% tumor discount (nonetheless enrolled in therapy). A 3rd affected person introduced no proof of tumor development in the course of the 3.5 months of the examine. That’s, two out of six sufferers confirmed tumor reductions. Due to this fact, the outcomes are partially favorable, however oncology is notably tough. CTMX’s outcomes don’t appear as revolutionary as initially anticipated, which might partially clarify the inventory’s decline.

Low cost however Dangerous: Valuation Evaluation

From a valuation perspective, CTMX trades at a $110.7 million market cap, making it a biotech microcap. Its steadiness sheet holds $36.2 million in money and equivalents and $114.1 million in short-term investments. In complete, its accessible short-term funds quantity to $150.3 million. Whereas CTMX has no significant monetary debt, its complete liabilities quantity to $216.4 million, largely as a consequence of deferred revenues of $183.3 million. Due to this fact, I feel CTMX’s financials are fairly strong at this stage, particularly as a result of deferred revenues suggest money funds acquired with providers rendered pending. Curiously, it’s due to these deferred revenues that its steadiness sheet reveals a unfavourable e book worth of $31.7 million, however as a consequence of this accounting dynamic, I wouldn’t take it as a pink flag.

Supply: Company Presentation. June 2024.

Furthermore, I estimate CTMX’s newest quarterly money burn was $26.1 million by including its CFOs and Web CAPEX. This suggests a yearly money burn of $104.4 million, which suggests a money runway of about 1.4 years. This isn’t but alarming, nevertheless it signifies that CTMX will possible increase further capital within the subsequent couple of years, in all probability via fairness, as beforehand carried out. For context, CTMX raised $110.2 million and $139.6 million via inventory issuance in 2021 and 2018, respectively. The issue is {that a} comparable increase within the subsequent couple of years would suggest important dilution at its present valuation, a threat shareholders should contemplate. That is very true for CTMX, which has no section 2 drug candidate in its pipeline, and it’s largely early-stage analysis packages in section 1 and preclinical phases.

Supply: Searching for Alpha.

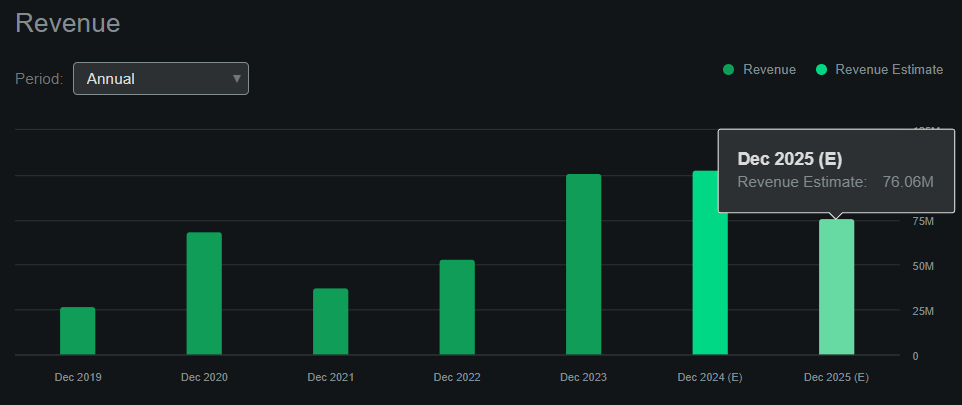

Searching for Alpha’s CTMX dashboard forecasts the corporate will generate about $76.1 million in revenues by 2025. This implies there are additionally negligible speedy income development prospects for the foreseeable future. To recap, CTMX trades at 0.7 occasions its money worth, with an implied ahead P/S ratio of 1.5. This valuation a number of appears self-evidently low cost. For context, its sector’s median ahead P/S a number of is 3.8, so CTMX seems comparatively undervalued via totally different metrics.

Nevertheless, inventory dilution dangers coupled with its low money runway and early-stage analysis packages tamper my optimism concerning the inventory. Therefore, I lean in direction of a impartial ranking on CTMX because the positives and negatives even out, so I price CTMX a “maintain” for now.

Extra Caveats: Threat Evaluation

It’s vital to notice that CTMX’s funding profile does have potential upside and draw back catalysts. As an example, any important breakthroughs in its analysis that present compelling effectiveness and security profiles might rapidly re-rate the inventory larger. Furthermore, if CTMX pronounces any new main partnerships with appreciable milestone funds, it might additionally trigger the inventory to extend, particularly since it’s a microcap, as a result of it doesn’t take a lot shopping for energy to maneuver it considerably.

Supply: TradingView.

Then again, CTMX can also be working towards a diminishing money runway. If time passes with none main optimistic bulletins, it might power it into an fairness providing whereas the inventory stays comparatively low cost. This might trigger important dilution and the share value decline, possible inflicting shareholder losses. Therefore, I see equal execs and cons, so I lean impartial on CTMX. Nevertheless, I imagine CTMX is value including to your watchlist, particularly as a consequence of its Probody platform potential.

Watchlist For Now: Conclusion

CTMX is a promising biotech, particularly as a consequence of its Probody platform. Nevertheless, a lot of the firm’s IP stays within the early phases, with solely Part 1 drug candidates now. Furthermore, its money runway implies it’ll possible must faucet the capital markets for extra funding within the subsequent few years, which might dilute shareholders considerably on the present valuation. Whereas I reckon CTMX has potential, I understand its dilution dangers can’t be ignored. Therefore, I take a impartial stance on the inventory, ranking it a “maintain” for now. Nevertheless, CTMX is value including to your watchlist if one thing materially adjustments its funding equation.

{kind=link}