littleclie

Abstract

Following my protection on MSCI (NYSE:MSCI) in Apr’24, which I beneficial a purchase ranking as I believed the valuation was low cost (inventory was oversold) and that the expansion outlook was not structurally impaired, this publish is to supply an replace on my ideas on the enterprise and inventory. MSCI continues to obtain a purchase ranking from me as numerous indicators counsel development will proceed to be robust. Any slowdown in development is just about because of the unsure macro atmosphere, which ought to get higher as we get extra readability on the Fed’s resolution to chop charges and the US election involves an finish. Valuation can also be nonetheless low cost when in comparison with the market.

Funding thesis

On 23-07-2024, MSCI launched its 2Q24 earnings, which noticed income development of 14% (natural development was 9.7%), driving whole income to $707.9 million, beating the road’s estimate for ~12% y/y development. Each section contributed to this development on an natural foundation, the place index income grew 9.8% y/y; analytics income grew 11.2%; ESG & Local weather income grew 10%; and personal property income grew 1.3%. By income sort, recurring subscription income grew 14.4%, trending increased than the consolidated stage as non-recurring income modestly dragged down development efficiency (down 15% in 2Q24). EBITDA margins had been flat vs. 2Q23 at 60.7%, leading to an EPS of $3.64, beating consensus estimates of $3.55.

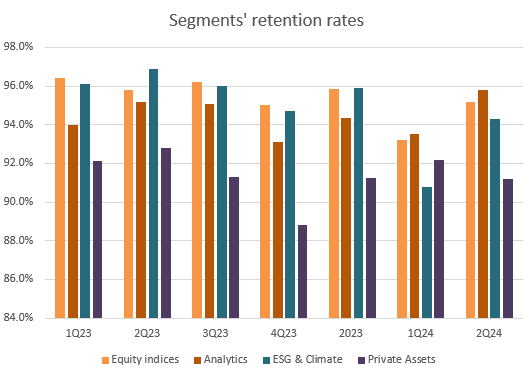

The principle destructive narrative, I consider, that’s stopping the MSCI share worth from going increased might be the macro impression on energetic asset managers (MSCI’s shoppers). There is no such thing as a doubt that MSCI is getting impacted because it results in shoppers tightening their budgets, longer gross sales cycles, and weak index recurring subscription income development of 8% y/y (that is beneath the historic development of low-teens development) as a consequence of elevated cancellations. Nonetheless, I reiterate my view that development is being delayed and never structurally impaired. If it was certainly a structural impairment to demand, the MSCI retention fee ought to see a success as shoppers churn. Nonetheless, that isn’t the case. In reality, retention charges rose throughout all segments besides ESG & Local weather (which I additionally suppose is non permanent because of the US election, as mentioned beneath).

Personal calculation

2Q24 outcomes proceed to show that MSCI can proceed to develop healthily. A number of main indicators help my view. Primary, AUM in ETFs linked to MSCI indexes grew very strongly at 19% to a complete of $1.63 billion, and this translated instantly into index asset-based price development of 18% within the quarter, accelerating from 13% in 1Q24. On condition that the market (utilizing S&P as a benchmark) is up so strongly on a year-to-date foundation (about 16%), this could proceed to drive robust fund inflows into ETFs and non-listed merchandise linked to MSCI indices.

Quantity two, the sturdy efficiency seen in MSCI’s Analytics section (11% development in 2Q24) exhibits that MSCI can also be benefiting from the unsure macro atmosphere. Particularly, MSCI addresses funding managers want for analytical instruments to higher facilitate credit score and liquidity threat within the present financial atmosphere. My expectations are that the macro state of affairs will keep unsure at the very least till the top of this yr, because the Fed has not particularly known as out when they’re reducing charges and the US election is in November. As such, Analytics section development ought to stay elevated.

Quantity three, to enhance its personal firm ESG protection, MSCI has entered right into a partnership with Moody’s [MCO] personal firm database, Orbis. In return, MSCI will present MCO with information on its ESG scores. This partnership does not appear to be short-term as in 2025, each events agreed to increase the partnership into personal credit score. This can be a huge win for MSCI as a result of it considerably enhances the worth proposition of its ESG & Local weather providing immediately to shoppers – which additionally makes MSCI stickier. Traders could be involved that this section’s development has slowed by 100bps to 10% vs 1Q24, however I don’t suppose that is an space of concern. The rationale for the slowdown is probably going as a consequence of US shoppers pulling again their investments in the intervening time as they’re unsure in regards to the upcoming US election – which is able to impression insurance policies associated to ESG. There is no such thing as a structural impairment to development in any respect, as different areas like EMEA grew 17% and APAC grew 20%. My view is that this section development will recuperate publish the election, and general section development will inflect upward once more.

Valuation

Personal calculation

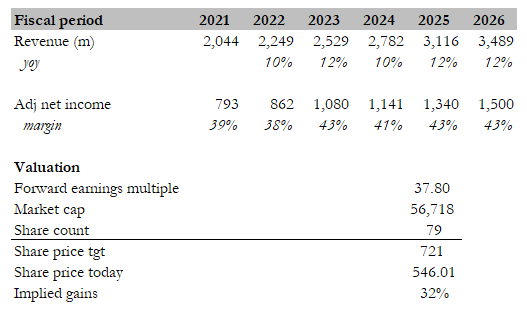

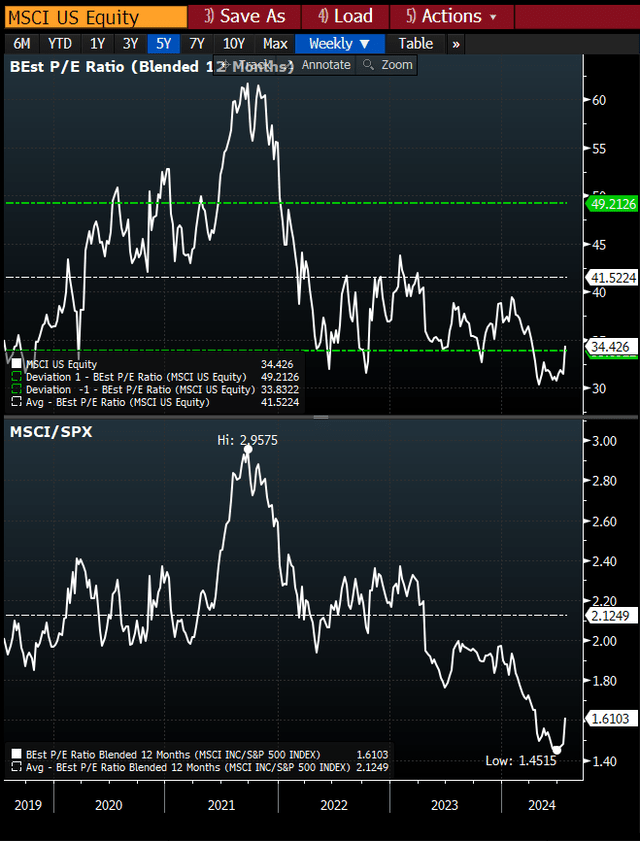

Even after the sharp enhance within the share worth, I nonetheless consider there’s a sexy upside to the share worth. My revisited worth goal is now $721 primarily based on FY26e estimates (my earlier worth goal was $552 primarily based on FY25e estimates). On this revised mannequin, I’ve introduced down my FY24 estimates as I acknowledge the present unsure macro state of affairs will seemingly persist till the top of the yr. Nonetheless, publish FY24, I’m anticipating MSCI to revert again to its normalized development and margin profile (12% development and 43% web margin). The variable here’s what a number of MSCI ought to commerce at, and I feel one of the best ways continues to be to anchor expectations in opposition to the S&P500 a number of. My earlier view was that MSCI would commerce again to ~1.8x of S&P’s common PE a number of, and this ratio has moved in my anticipated path after the market acknowledged MSCI’s robust 2Q24 outcomes. In a normalized atmosphere, I consider this ratio will proceed to development again to the typical stage of two.1x. Doing the identical math and attaching 2.1x to the S&P common a number of of 18x, I consider MSCI will commerce as much as 38x ahead PE. That is roughly the typical the MSCI has been buying and selling at over the previous 5 years if we take away the COVID interval the place multiples went above 41x.

Bloomberg

Danger

The US industrial actual property business is prone to falling even additional, and thus far, the impression has been distinguished in MSCI’s outcomes, the place personal property natural income development got here in weak at 1% y/y in 2Q as a consequence of a industrial actual property slowdown, which impacted demand for MSCI’s transaction information merchandise. If the business blows up, it might drag down general topline efficiency for MSCI. This might put a ceiling on how excessive valuations might doubtlessly rerate within the close to time period.

Conclusion

In conclusion, I reiterate my purchase ranking for MSCI. Whereas the macro atmosphere is impacting energetic asset managers, my view is that MSCI’s development is delayed, not impaired, as evidenced by rising AUM in ETFs and shopper retention. The unsure atmosphere till the US election additionally advantages MSCI’s Analytics section. As for the slight weak point in ESG & Local weather, it’s seemingly non permanent as a consequence of buyers’ considerations about how insurance policies associated to ESG might change after the election. Lastly, valuation stays enticing with upside potential.

{kind=link}