Photos By Tang Ming Tung/DigitalVision through Getty Photos

Lyft (NASDAQ:LYFT) has curiously underperformed by a large margin this yr, regardless of displaying each sustained top-line development and continued margin enlargement. Whereas its shut competitor Uber (UBER) is perhaps receiving many of the investor love, it’s arduous to disregard the steep relative low cost in addition to the excessive internet money place making up over 15% of the market cap. Administration has outlined bold medium time period targets which can indicate that the inventory is kind of undervalued right here. I’m upgrading the inventory to purchase.

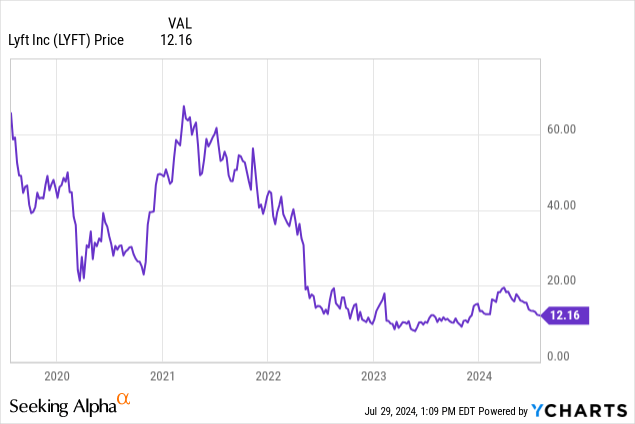

LYFT Inventory Worth

I final coated LYFT in December the place I defined why I used to be downgrading the inventory because of valuation. That proved to be fortuitous timing because the inventory has since underperformed the broader market by round 30%.

That type of underperformance can alleviate a substantial amount of valuation issues, particularly as the corporate continues to execute strongly.

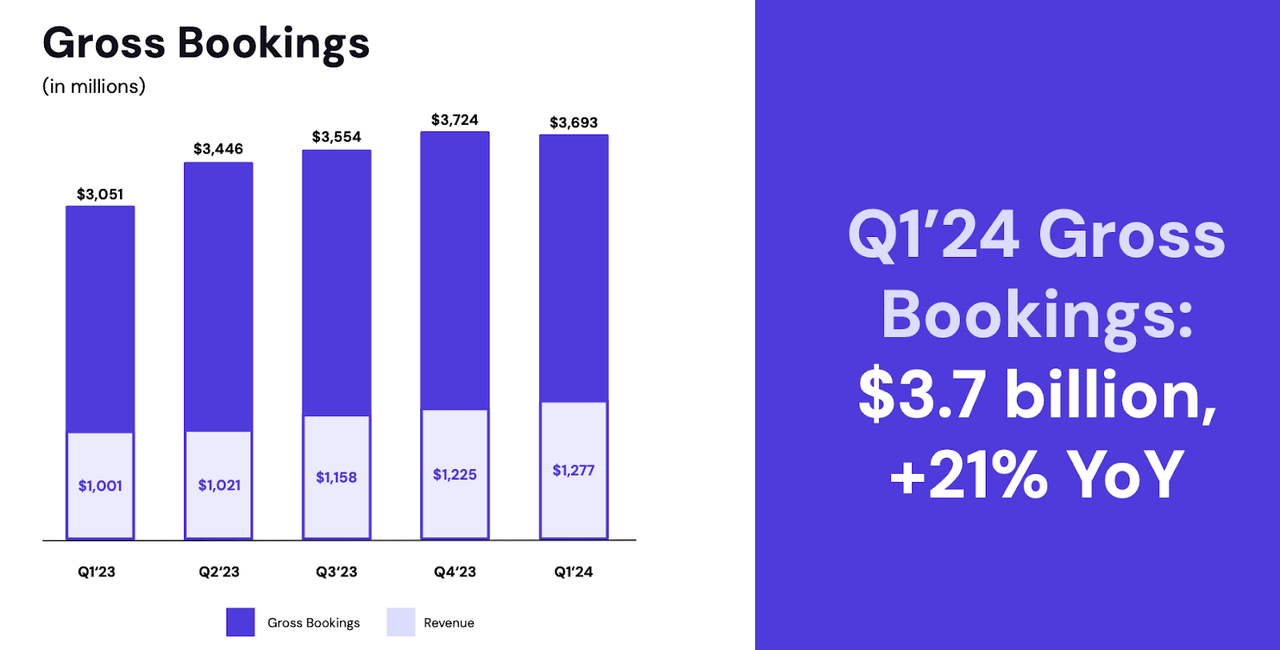

LYFT Inventory Key Metrics

In the latest quarter, LYFT generated 27.5% YoY income development to $1.277 billion and 21% YoY gross bookings development to $3.69 billion, surpassing steering for as much as $3.6 billion. I notice that the corporate is now lapping simpler comparables, as income development had beforehand lagged bookings development because of pricing modifications final yr. Over time, I anticipate income development to return to intently matching bookings development.

2024 Q1 Presentation

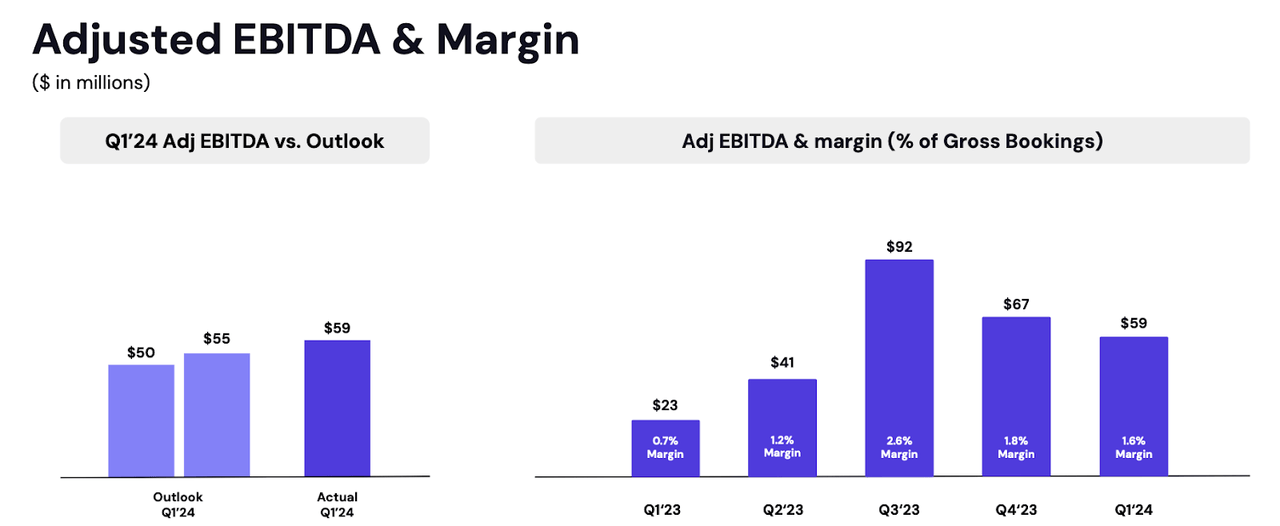

The corporate generated $59 million in adjusted EBITDA, surpassing steering of between $50 million and $55 million, and representing 90 bps of margin enlargement on a YoY foundation.

2024 Q1 Presentation

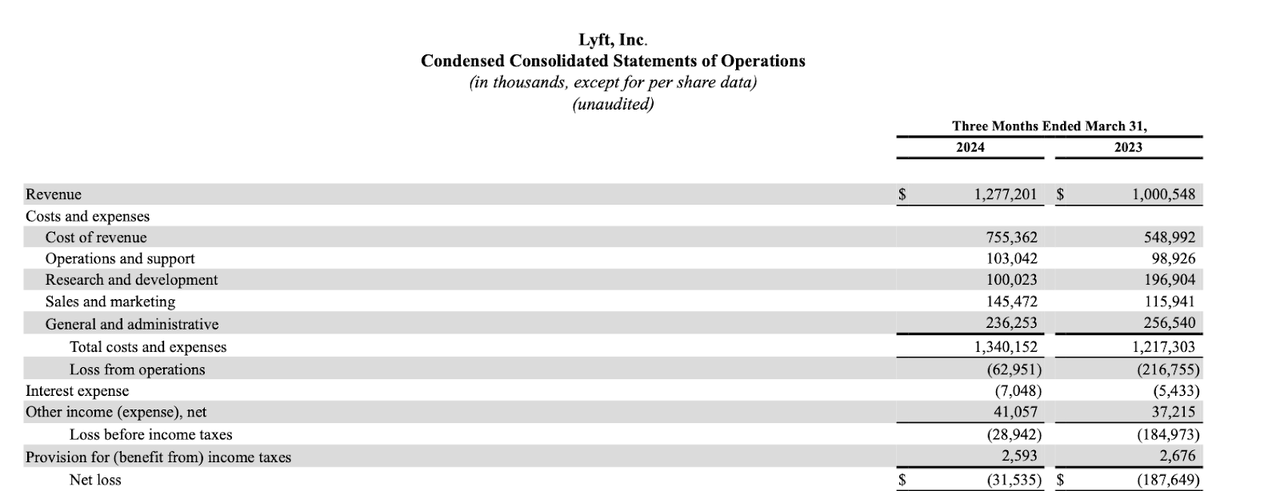

Many readers could also be cautious of utilizing non-GAAP numbers, and I don’t blame them. However I ought to notice that the corporate has made nice progress in decreasing its GAAP losses, with its GAAP internet loss narrowing from $187.6 million to $31.5 million.

2024 Q1 10-Q

LYFT ended the quarter with $1.7 billion of money versus $942 million of debt, representing a powerful internet money steadiness sheet. I notice that $389 million of the convertible debt matures in 2025 and carries a 1.5% rate of interest, that means that the corporate may see curiosity bills rise when the corporate refinances this debt.

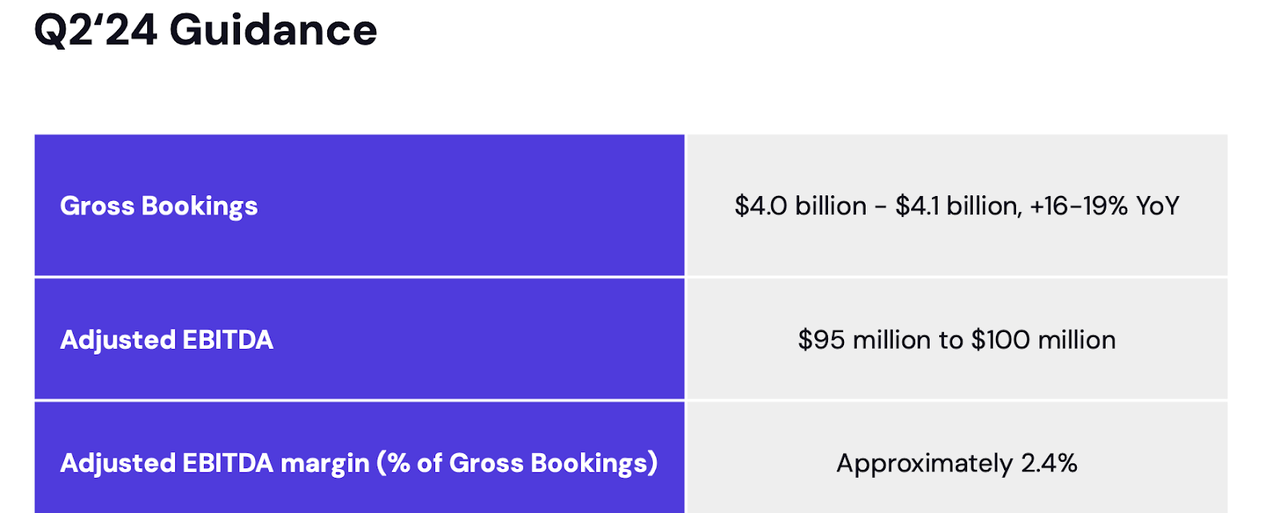

Wanting forward, administration has guided for as much as 19% YoY gross bookings development and $100 million in adjusted EBITDA within the second quarter.

2024 Q1 Presentation

For the full-year, administration expects gross bookings to develop round that very same tempo, with an emphasis on changing adjusted EBITDA into free money circulation.

2024 Q1 Presentation

On the convention name, administration famous that they’d lowered experience cancellations “by practically 50% versus a yr in the past,” serving to to enhance driver satisfaction. That metric could assist deal with investor issues that UBER is taking up the market – that detrimental sentiment doesn’t look like displaying within the fundamentals. Administration believes that they proceed to learn from some close to time period tailwinds, together with the continued return to the workplace in addition to the continued enthusiasm for dwell occasions like live shows. Concerning autonomous driving, administration has tried to border it extra as a chance than a threat. At this level, I feel it’s nonetheless too early to make such a dedication in both path, because it stays unclear if the upper competitors could also be offset by lowered driver bills.

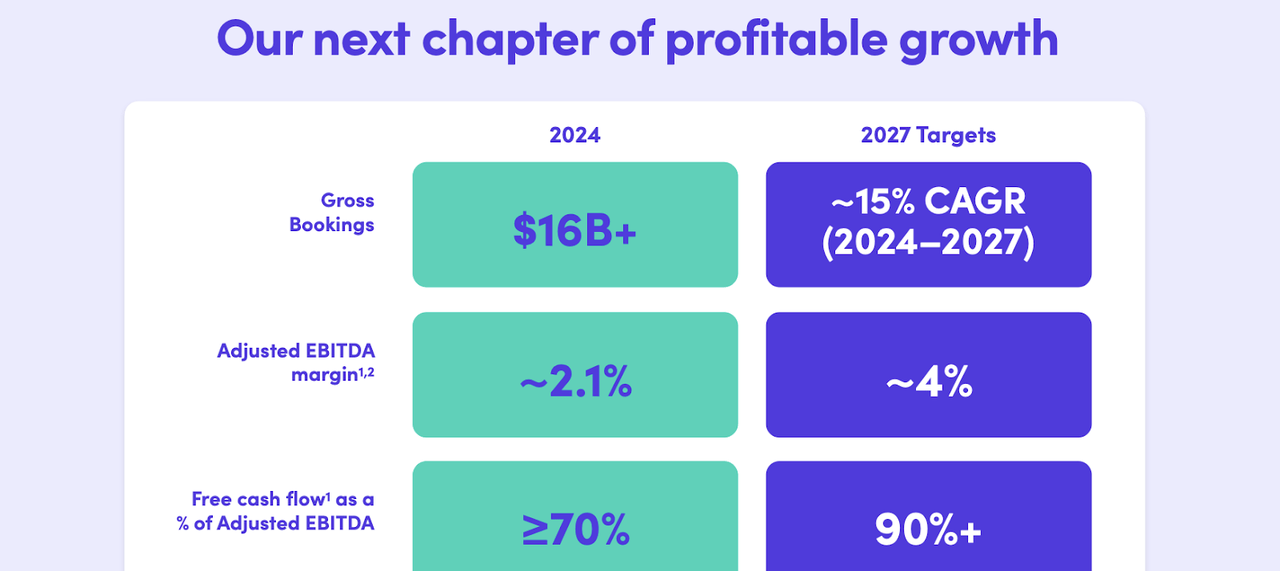

On the firm’s 2024 Investor Day, administration focused gross bookings to develop at a 15% CAGR by 2027 with adjusted EBITDA margins anticipated to rise 200 bps to 4%.

2024 Investor Day

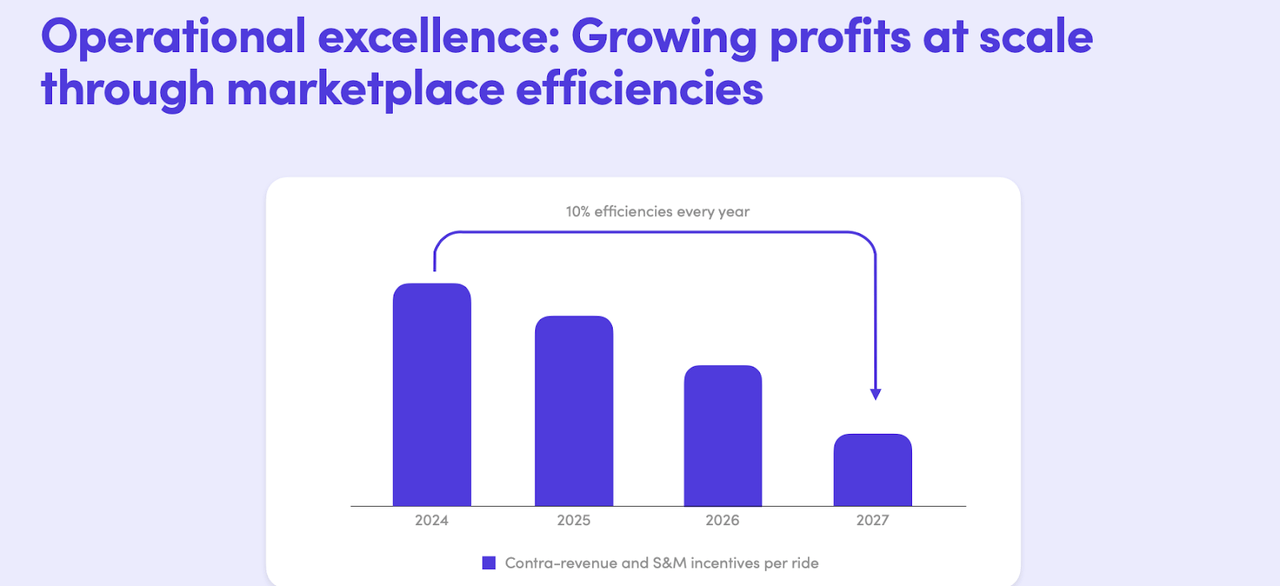

Administration expects to drive roughly 10% of OpEx efficiencies yearly by 2027. I discover these targets to be plausible on condition that they’re primarily focusing on promotional exercise, which in concept ought to proceed easing given the elevated driver provide post-pandemic.

2024 Investor Day

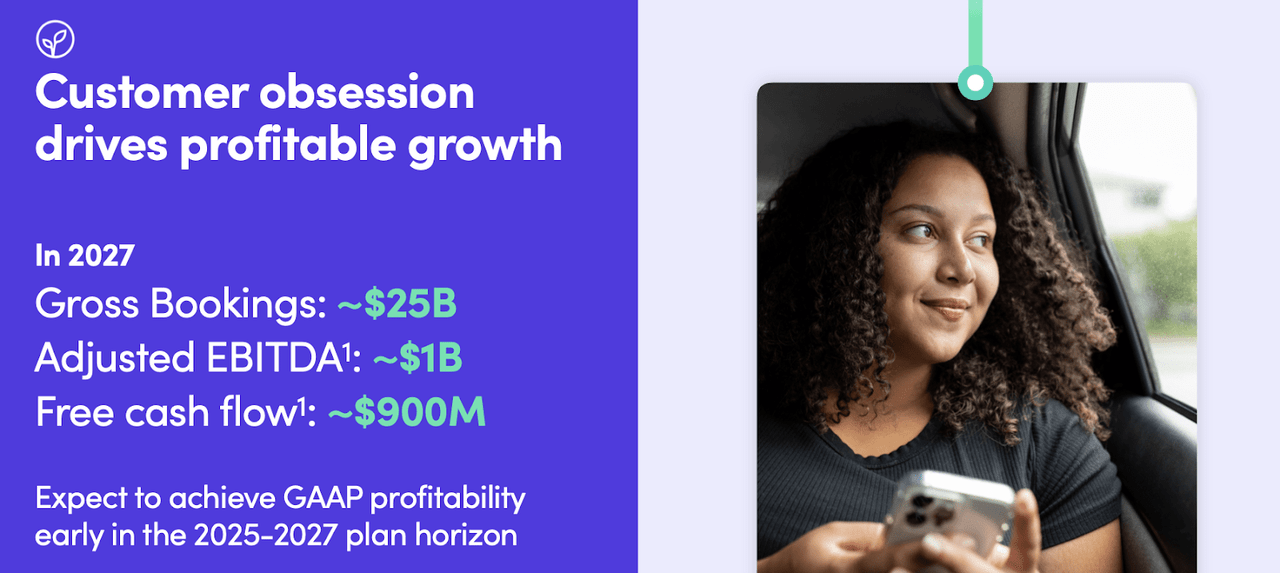

Administration expects these efforts to result in roughly $25 billion in gross bookings and $1 billion in adjusted EBITDA by 2027.

2024 Investor Day

Administration has additionally focused GAAP profitability “early” within the 2025 to 2027 horizon. Based mostly on what I see within the earnings assertion, I feel that working leverage alone could possibly enable the corporate to attain these objectives by that time-frame.

Is LYFT Inventory A Purchase, Promote, or Maintain?

It was fascinating that neither UBER nor LYFT noticed its inventory profit from the favorable gig financial system ruling in California, however maybe buyers have been already anticipating a constructive final result. After the latest underperformance, LYFT discovered its inventory buying and selling at simply 6x 2028e non-GAAP earnings.

Looking for Alpha

The undervaluation is made much more obvious within the inventory’s 0.9x a number of of this yr’s gross sales. Evaluate that to the three.1x a number of at UBER.

Looking for Alpha

Assuming that administration can execute in opposition to their aims to spice up margins, I anticipate that relative low cost to slim over time (for reference, UBER’s adjusted EBITDA margin stands at round 3%). It’s fascinating to see UBER see its inventory re-rate sharply larger over the past a number of years, because the market seems to be much less frightened about profitability and as an alternative viewing it as a recurring income enterprise. LYFT, in distinction, has seen its inventory commerce sharply decrease over that very same time-frame. It seems that the market believes that this can be a “winner takes all” market, however therein lies the chance. I can see LYFT ultimately re-rating to 1.5x gross sales, implying an 8x EBITDA a number of primarily based on administration’s 2027 goal.

LYFT Inventory Dangers

It’s attainable that LYFT is unable to compete in opposition to UBER. This may happen if the “community impact” have been to interrupt down within the different path, specifically, if LYFT have been to see deteriorating driver provide and rider demand to the purpose that it negatively impacts its potential to function effectively. My anecdotal expertise is that there could also be room for at the very least two rideshare operators, however buyers ought to intently monitor how the aggressive panorama shapes up over the following a number of years. LYFT has already undertaken drastic value discount, and I’m not so assured that there’s rather more “fats” that may be lower from right here. Because of this, any setbacks within the development story could impair the corporate’s potential to hit its profitability targets, and hasten the projected draw back.

LYFT Inventory Conclusion

LYFT seems to be like a forgotten inventory as buyers are extra passionate about UBER. However LYFT has proven strong monetary ends in its personal proper, and the inventory seems poised for strong upside if administration can execute in opposition to their medium time period targets. The inventory’s latest underperformance has significantly improved the worth proposition, main me to improve the inventory to purchase.

{kind=link}