Alistair Berg

Willdan Group Inc. (NASDAQ:WLDN), is an organization positioned to learn from some strong tailwinds that embrace AI, electrical load development, and decarbonization. It continues going through stable demand for its companies from its shoppers within the authorities, business, and utilities areas, which is translating into report efficiency. With such sturdy alternative, and a good valuation, I like to recommend a robust purchase score for the inventory.

Willdan Group: Driving Sustainable Positive factors

Willdan Group is knowledgeable, technical, and consulting service supplier targeted on driving sustainable vitality transitions for its shoppers. These shoppers vary from state and native governments, utility firms, to business gamers. By way of its expert-led options, the corporate has efficiently helped its shoppers keep away from emissions of seven.8 million metric tons of greenhouse gases, through the years. For context, that is equal to eradicating the influence of 1.7 million passenger automobiles for one full 12 months.

With 53 workplaces throughout North America, almost 1700 workers, and a market cap of over $500 million {dollars}, Willdan Group is a well-established participant on this house, together with a extremely respected model. The corporate attracts in an annual income of over $550 million.

Demand for Willdan’s companies stays strong in all its segments, given the numerous price and vitality financial savings it delivers to its shoppers, all whereas boasting an environmentally sustainable worth chain. This sustainable positioning, together with its numerous income streams, makes the corporate very compelling over the long run.

Along with this broader issue of enchantment, every of Willdan Group’s three shopper varieties additional add to its strengths. As an illustration, the corporate’s government-facing shopper phase, representing 43% of complete income, continues to be a spectacular development driver, with a YoY gross sales improve of 27%.

Equally, Willdan’s utilities shopper kind, which primarily represents multi-year income contracts, positions it largely within the energy-intensive knowledge middle house. On this entrance, the corporate is well-positioned to get pleasure from broad tailwinds, particularly as AI purposes proceed to enter the mainstream and push electrical load development increased.

Lastly, on the business finish, Willdan continues to display its technical {and professional} functionality whereas strengthening its model and market place. For instance, in response to its current earnings name, the corporate lately received a contract with Meta Platforms for a research relating to a voluntary clear vitality procurement program they’re engaged in. Willdan shouldn’t be new to working carefully with main tech gamers, because it has been concerned with AT&T, an early entrant within the knowledge middle business, from very early on. General, pursuing research and different contracts from tech giants provides to Willdan’s credibility, which in the end would improve demand for its choices.

Broadly talking, Willdan’s returns are noticeably aligned with the prices of electrical energy by means of its vitality phase. Consequently, the corporate continues to get pleasure from stellar development that’s largely pushed by double-digit electrical energy fee hikes within the firm’s two largest markets: California and New York. What I significantly like about this side of the corporate is that the dynamic provides an inflation hedge to the inventory, particularly in relation to rising electrical energy prices.

General, Willdan Group appeals to me as a result of it’s uniquely positioned to seize alternative, whereas being a power for sustainability and transition. To me, it’s clear that the corporate will proceed to sail on forward, pushed forward by AI, electrical energy load development traits, and the overall shift in direction of optimized vitality consumption by authorities companies and tech firms.

Monetary Overview

FY24Q2 proved to be a report quarter for Willdan Group, in some ways, beating its personal expectations, in addition to of analyst consensus. On the topline, the corporate noticed a climb of 18.41%, delivering complete income of $141 million for the quarter. This sturdy climb in income comes primarily from rising municipal engineering contracts, in addition to undertaking administration income recognition coming in from a considerable backlog. Owing to a lot better volumes and a decrease development fee in price of gross sales vs contract income, the corporate additionally noticed a slight 49 foundation level enchancment on its gross margin.

Turning in direction of working revenue, we see an much more spectacular image, with a 161% YoY soar to $6.4 million. The margins right here additionally showcase sturdy enchancment, with a virtually 250 foundation level improve from 2.08% to 4.57%.

Transferring to the underside line, we see the identical development with EPS surging from $0.03 to a full $0.33, in simply 12 months. This was largely pushed by improved tax charges within the present fiscal 12 months, in addition to a decrease efficient rate of interest attributable to the next money steadiness and a lowered leverage. When it comes to adjusted EBITDA, we see a 56% soar from $8.2 million to $12.8 million. When checked out when it comes to gross sales, this can be a margin enchancment from 13.3% of web income to 17.7%. That is 440 foundation factors in enchancment.

What I discover particularly compelling in regards to the firm from a monetary standpoint is its efforts in translating these beneficial properties in direction of strengthening its steadiness sheet. In simply six months from the year-end in 2023 to June 2024, the corporate’s web debt determine plunged from $75 million to beneath $50 million.

General, the Willdan’s financials paint a wonderful image of its strategic execution, and its capacity to capitalize on broader tailwinds and alternatives it has positioned itself with.

Valuation

WLDN inventory has climbed by 75% YTD. Upon nearer examination of its value chart, it’s clear that the market provides it a notable enhance as its earnings are launched, and the beneficial properties constantly held regular within the intervals that comply with.

TradingView

Usually, shares see a big value surge after constructive earnings, and there’s a correction that ultimately follows as soon as the hype cools down. This isn’t the case with WLDN as, I consider, there may be substantial upside to the inventory that has room for much more development past its submit earnings pleasure.

In line with the Quant grade elements, it could appear that WLDN is nearly priced for development. It holds a valuation rating of a C-, regardless of Development, Momentum, and Revisions all being within the A classes. Regardless of this pricing, nevertheless, I really feel that there’s nonetheless a worth alternative right here for people who act fast.

Creator

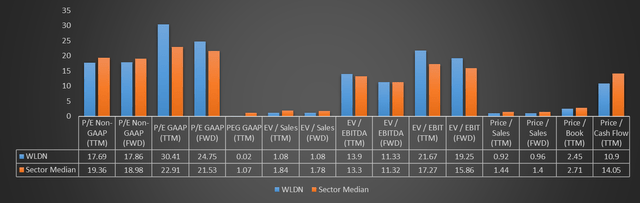

As you’ll be able to see within the knowledge visualized above, WLDN’s valuation multiples exceed the sector’s median solely in 5 out of the fifteen metrics displayed. From these 5, solely three present a big discrepancy of over 10%. Furthermore, 4 of those 5 are PE ratios, that are understandably excessive, as the corporate has solely been worthwhile for the final two years. Equally, whereas its EV/EBITDA (TTM) determine of 13.90 factors to a possible overvaluation, it’s considerably beneath the inventory’s personal five-year median determine of 76.69.

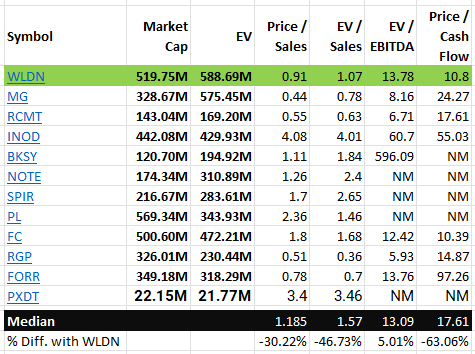

To get a extra targeted look, as an alternative of evaluating WLDN value multiples with the commercial sector, I’ve chosen 11 further firms from the analysis and consultancy business, with an enterprise worth near that of Willdan Group. The findings are proven beneath:

Creator Creator

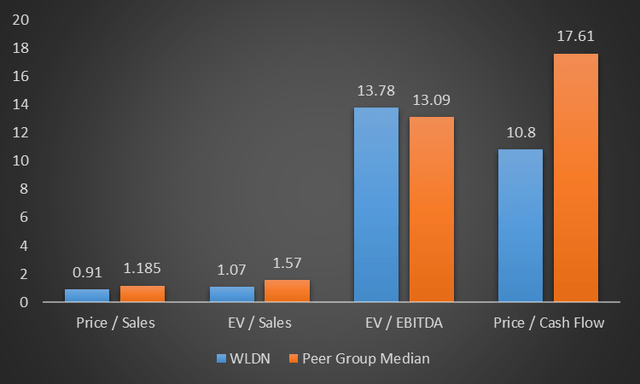

On this extra targeted look towards friends from the analysis and consultancy business, we see a possible undervaluation on the Value/Gross sales, EV/Gross sales, and Value/Money Stream ratios. Specifically, the corporate’s enterprise worth of $598 million is considerably decrease than the remainder of its friends, given its gross sales quantity. That could be a sturdy indication of an undervaluation to me. The one exception to the development appears to be the EV/EBITDA.

Primarily based on these indicators, I really feel that the inventory could also be undervalued, based mostly on its sturdy development traits. Contemplating its sturdy positioning, tailwinds in electrical load development, AI and the info middle scene, the purchase case is fairly clear.

Danger

As talked about above, Willdan Group has been steadily working to strengthen its steadiness sheet, as is clear by its enhancing web debt determine. Regardless of this, nevertheless, it should be identified that the corporate’s steadiness sheet is extremely leveraged, with a complete debt of $90 million. This places its complete debt to fairness ratio at 0.44. The results of such a heavy debt burden is a considerable curiosity fee. Trailing twelve months, Willdan’s curiosity expense quantities to about $8.8 million, which is kind of sizeable, contemplating this displays a 3rd of the corporate’s working revenue. That is very pricey for my part, particularly when it comes to its influence on the corporate’s backside line. I additionally consider that, if this isn’t managed, it may hamper the corporate’s capacity to translate its spectacular topline development into returns for its shareholders.

Takeaway

The Quant Score system places WLDN within the ‘sturdy purchase zone’ and so do Wall Avenue analysts (given its rankings within the final 90 days). I consider this can be a truthful place and I too would advocate a robust purchase for the inventory. It is experiencing phenomenal development on the efficiency aspect, and is well-positioned to learn from some very strong tailwinds. With AI including load to present knowledge middle infrastructure, an elevated electrical load, and a basic development in direction of lowering emissions, I consider WLDN is more likely to soar to vital new highs.

{kind=link}