Oil Tanker HeliRy

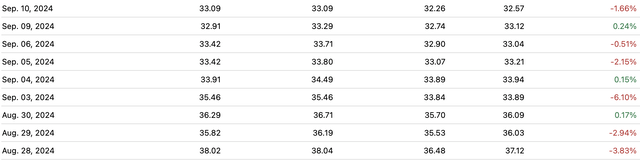

Within the two weeks ended September 10, TORM plc (NASDAQ:TRMD) crashed roughly 14% to $32.26, a degree not seen in years.

TORM plc historic costs (Searching for Alpha Quant)

The wrongdoer behind the crash seems to have been falling oil costs. On Tuesday, the WTI crude value dipped under $70 and took most associated equities together with it. By the shut of the buying and selling day, Brent Crude was under $70 per barrel, whereas WTI was close to $65. These value ranges had been even decrease than these seen in late 2023, which noticed costs down practically 50% from the mid-2022 highs.

Though TORM is just not instantly concerned in shopping for and promoting crude oil, its shopper base is; subsequently its value tends to be correlated with these of oil and gasoline firms. We noticed this impact final week when TRMD inventory fell together with its exploration and manufacturing (E&P) cousins.

TORM plc is an oil tanker firm, which means it transports oil and different petroleum merchandise by sea. Oil costs affect long-term profitability in TORM’s trade, though not as strongly as they affect oil firms’ profitability. It is extra the demand for oil and measurement of the tanker fleet that affect tanker profitability, fairly than value. Principally, a whole lot of demand for oil will often preserve tankers full, even when extra provide is weighing on costs. That is doubly the case when oil must be shipped by sea for no matter cause. Sanctions on Russia within the wake of the Ukraine invasion led to extra maritime delivery, as many European patrons couldn’t settle for oil from Russian pipelines. Lots of the suppliers that changed Russia-such because the U.S.-were separated from Europe by massive oceans. This reality was a boon to TORM plc and different tankers in 2022 and 2023, as they received extra enterprise because of the sanctions.

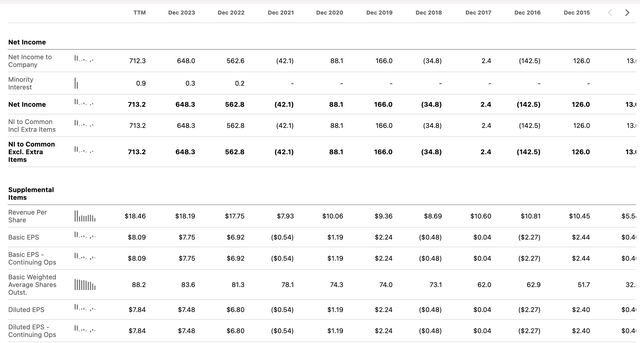

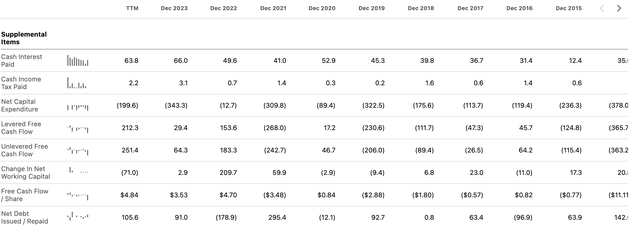

An attention-grabbing reality about TRMD is that, in contrast to E&Ps, its earnings continued rising in 2023 and into the trailing-12-month (TTM) interval. Because the financials in Searching for Alpha Quant present, the corporate hit document ranges of gross revenue, web revenue and free money circulation within the TTM interval. That is fairly completely different from the destiny of oil firms, whose earnings peaked in 2022, underscoring the truth that oil costs aren’t the most important think about TRMD’s profitability.

TORM at all-time excessive web revenue (Searching for Alpha Quant) TORM at all-time excessive FCF per share (Searching for Alpha Quant)

What’s the main driver in TRMD’s profitability?

It is exhausting to level to 1 single issue, however favorable geopolitics would appear to be a part of it. The corporate benefitted from patrons searching for alternate options to Russian crude in 2022, and now seems to be benefitting from the disruptions within the Pink Sea. In line with TORM’s most up-to-date earnings launch, the rerouting ensuing from the Pink Sea assaults led to strong demand for the corporate’s companies. The newly rerouted routes cowl an extended distance than the outdated ones did, leading to larger income tanker miles and larger general income.

One other think about TRMD’s profitability is the place we’re within the tanker cycle. The “tanker cycle” is a cyclical sample that performs out within the tanker trade. It isn’t all the time completely correlated with the broader economic system. The cycle consists of a development part attributable to elevated demand; a plateau the place tanker charges are excessive and corporations are shopping for extra ships; and eventually a contraction part by which extra tankers within the ocean results in value competitors and decrease charges. The size of a tanker cycle is regarded as between three and 10 years.

If we knew precisely the place we had been within the tanker cycle, then we would have a very invaluable edge in evaluating an organization like TORM. Sadly, it isn’t precisely straightforward to foretell these items, and even the very best forecasts of future demand are solely “roughly” appropriate. TORM appears to suppose that the nice instances will final, because it bought 9 vessels during the last 12 months whereas promoting just one. That will point out bullishness from administration for now; however alternatively, this precise kind of stockpiling of vessels results in downward stress on charges within the later phases of the cycle. Most forecasts for the tanker trade are at the moment bullish, and we positively aren’t close to the top of a cycle; nevertheless, we aren’t initially of an enlargement part both. Most probably, we’re someplace close to the late phases of an enlargement and the early phases of a peak. This may have a tendency to point that TRMD has some good years of profitability remaining, and even perhaps a continued interval of lively earnings growth-albeit development at a slower tempo than was seen in 2022 and 2023.

After I final lined TORM plc, I gave the inventory a ‘purchase’ score as a result of it was extraordinarily low-cost whereas tanker trade fundamentals remained sound. Immediately, I maintain largely comparable views in regards to the firm and its prospects, however the now-lower inventory value will increase my enthusiasm. On this article, I clarify why I am upgrading my score to sturdy purchase.

Massively Bettering Fundamentals

TORM plc’s fundamentals have improved on primarily each significant metric in recent times. The one threat to the lengthy thesis primarily is a significant change within the economics of the tanker trade that causes a decline in earnings. That will be a significant threat to TORM as a result of the inventory at the moment has a really excessive payout ratio and even a moderate-sized decline in earnings might probably pressure a dividend discount. I will discover the probability of that taking place in a later part. For now, I’ll take a look at the previous few years’ enchancment in fundamentals, and why the inventory is a purchase if it may be decided that this success will final for not less than just a few extra years.

We are able to begin with the revenue assertion.

Over the past 5 years, TRMD has compounded a few of its key revenue assertion metrics on the following charges:

Income: 19.72%.

EBITDA: 40.5%.

Internet revenue: 230%.

Earnings per share (EPS): 233%.

These are compounded annual development charges, not cumulative charges. The cumulative development has been actually exceptional, with web revenue up 5,384% during the last ten years.

After we take a look at the money circulation assertion, we see comparable traits:

Working money circulation: $866 million, up 400% over 5 years.

Free money circulation per share: $4.84, up from detrimental figures each 5 and ten years in the past.

Lastly, we are able to see appreciable enhancements to the steadiness sheet. Within the TTM interval, the corporate had a 3.43 present ratio (larger is healthier) and a 0.615 debt to fairness ratio (decrease is healthier). These ratios have not exploded the best way web revenue and free money circulation have, however each had been mainly worse 5 years in the past than within the TTM interval.

Lastly, we should always take a look at the TTM profitability metrics. Right here is the place the corporate actually shines. Within the final 12 months, TORM had:

A 58% gross margin.

A 42% EBIT margin.

A 43% web margin.

A 39% ROE.

A 21% return on whole capital.

These figures are all above common, indicating that TORM was very worthwhile within the trailing 12-month interval.

Earnings Sustainability

It is nice to know that TORM was thriving in previous years, however it does not essentially imply that the corporate will thrive sooner or later. It operates in a cyclical trade that’s at the moment in an uptrend-the query is how lengthy will the corporate’s present power will persist. In case you take a look at TORM’s historic monetary statements, you will notice loads of dropping years. The query is how lengthy till the subsequent leg down within the firm’s fortunes trigger comparable issues to occur once more.

Evidently, final week’s crash in oil costs received individuals nervous that TRMD’s subsequent “leg down” can be occurring sooner fairly than later. I think that that is not the case. Oil costs play a job in tanker profitability, however they do not single-handedly decide it, as is the case with E&Ps. The provision of tankers on the ocean is in the end an even bigger think about tanker profitability; so long as producers see oil costs as excessive sufficient to justify delivery oil and there aren’t sufficient tankers, then TORM ought to make good cash.

We all know that TORM itself sees its prospects as being good. It’s investing in new ships (or fairly buying second-hand ships), and the general tone of its most up-to-date earnings launch was optimistic.

Is administration proper to be optimistic?

This is one encouraging signal: regardless of oil costs having risen 89% or 15.6% CAGR during the last 4 years, the tanker fleet has solely been rising at 1% to 2% per 12 months. So the fleet measurement is lagging oil costs, and possibly demand for oil as properly. Additionally, many tankers on the seas right now are outdated and in want of being changed. That would cut back the dimensions of the tanker fleet, which might enhance profitability at firms like TORM.

In fact, if oil costs collapse to unprecedented lows, then the tanker market might go down with them. That will be dangerous information, however as I wrote in my current article on Occidental Petroleum (OXY), the worldwide image for oil is certainly one of slowly rising demand, lowered OPEC provide, and plenty of provide disruptions. I might think about oil costs will maintain an inexpensive degree over the subsequent 5 years.

Valuation

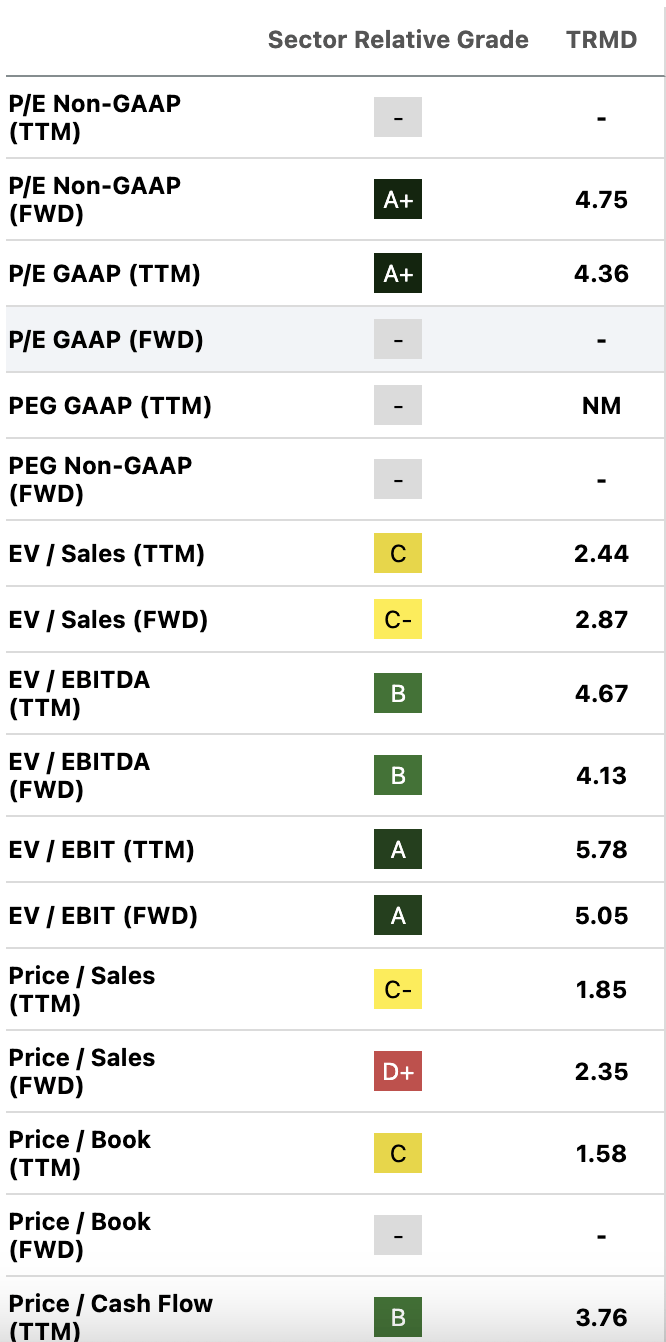

If my above forecast sounds surprisingly muted for a ‘sturdy purchase’ score, then it’d assist to take a look at the multiples under. TORM trades at all-time low earnings and money circulation multiples. It does not really have to proceed its current development streak to be well worth the funding. It simply wants to not shrink.

TRMD multiples (Searching for Alpha Quant)

In case you take TORM’s $4.84 in TTM FCF per share, and low cost it at 10% assuming no extra development, you find yourself with a $48.8 honest worth estimate. The inventory has 43.3% upside should you assume it by no means grows once more and worth it with a reduction price that means a very huge quantity of threat! It is this cheapness that has me very optimistic about TRMD at these newly decrease costs. I do not suppose the corporate will carry on rising prefer it has in current years-overall, I count on simply reasonable development for the subsequent 12 months or two. However if you take a look at how low-cost the inventory is, it’d simply be value it anyway.

Dangers

Earlier than concluding, I ought to contact on some company-specific dangers that TORM plc faces. The ‘macro’ dangers had been reviewed earlier, some particular to this firm embrace:

Environmental rules. TORM not too long ago acquired 22 new eco-friendly vessels at a big value. The investments had been obligatory however got here at nice value, because the eco-friendly options elevated the price of the ships. That additional value was as a consequence of regulatory pressures from the EU, which now calls for extra environment friendly modes of transportation than earlier than. A excessive payout ratio. In line with Searching for Alpha Quant, TRMD’s payout ratio is 84%. Which means the corporate’s dividend dangers being minimize if earnings decline, or eradicated if earnings go detrimental. For now, TORM’s trade seems wholesome sufficient to help continued dividends. However this isn’t a inventory one ought to simply sleep on. Searching additional than two years, cuts are attainable.

The Backside Line

TRMD is a inventory that has just about every thing you’d want-high development, cheapness and excessive margins, multi functional package deal. The principle “catch” right here is that this can be a cyclical inventory, and there can be a downturn within the firm’s fortunes sooner or later. Nevertheless, most indicators point out that “some level” is a good approach’s off.

{kind=link}