syahrir maulana

After lagging the massive cap indices for many of the 12 months, small caps outperformed within the third quarter, pushed principally by a number of enlargement, as earnings proceed to be comparatively depressed relative to massive caps.

Efficiency And Positioning

The Madison Small Cap Fund (Class Y) returned 6.3% within the third quarter of 2024. Efficiency lagged the Russell 2000’s return of 9.3% and Russell 2500’s return of 8.8%. Underperformance was pushed by each allocation and choice. Our laggard sectors within the third quarter included: Industrials, pushed by inventory choice; Healthcare, additionally pushed by inventory choice; and Info Expertise, primarily pushed by allocation impact. Power outperformed, pushed by allocation, and Client Discretionary additionally outperformed, pushed by inventory choice.

We made only a few modifications to the fund’s positioning within the third quarter. Our solely new funding to the fund was Workiva (WK), a cloud-based software program supplier of compliance and regulatory reporting options, whose platform is utilized by hundreds of corporations to publish SEC and different regulatory paperwork.

Greater than 75% of the Fortune 500 use at the very least one of many options. The Workiva platform affords clients collaboration, information integration, and course of administration controls, which lead to better visibility and insights into their monetary and regulatory administration programs and allow environment friendly regulatory submitting and reporting. Workiva is taken into account a system of report for compliance and regulatory reporting, a comparatively non-discretionary class.

The corporate has a brand new CEO centered on worthwhile development by constructing a associate channel with the influential Massive 5 consulting companies. The aggressive moats are huge and deep, as Workiva continues to press the place it sees its best aggressive benefit: being the one supplier promoting a single platform for monetary and non-financial reporting with assurance.

Moreover, the corporate has a major put in base of present clients (~6,000) ripe for harvesting. Our base case is that the put in software program may be very “sticky” with low turnover charges and durables development runways. The present inventory value represents a fabric low cost relative to our conservative intrinsic worth evaluation of $100 per share. We have opportunistically used the mixture of latest administration resetting expectations, broadly weak sentiment for software program corporations, and up to date market volatility to determine this new place.

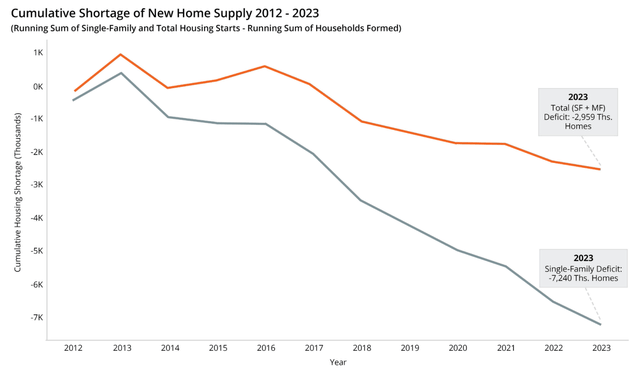

From a sector perspective, our overweights are in Client, Industrials, and Info Expertise, which has been constant for a number of years. Lengthy-time traders will know that we don’t make sector bets, these occur to be the areas the place we’ve discovered the best high quality enterprise at reductions to intrinsic worth. Though our Industrial shares characterize the largest drag to our efficiency within the third quarter, we’re very optimistic as we glance forward. Lots of our Industrial shares are tied to the housing sector, which has been depressed for a number of years. The housing market has been in a structural undersupply for a number of years (see the chart from Realtor.com). Residential building has been pressured by excessive prices and a decent mortgage market. Nevertheless, as we doubtlessly start a central financial institution fee easing cycle, the mixture of undersupply vs sturdy secular demand and decrease charges might lead to a major residential building cycle lasting a number of years.

Though we proceed to be underweight Healthcare, inventory choice year-to-date has been usually sturdy. Our largest chubby stays Info Expertise, the place we now have outperformed the Russell 2000 Index by about 1,000 foundation factors 12 months up to now, virtually all pushed by inventory choice. Many of those investments occurred throughout 2022, when the sector was extraordinarily out of favor, and we recognized attractively rising, worthwhile expertise corporations buying and selling at massive reductions to their intrinsic worth.

Whereas there’s some macro uncertainty out there, particularly across the energy and sturdiness of the labor market, client spending stays resilient, buoyed by increased wages and a halo of wealth impact from the sturdy market and better housing costs. Lots of our investments tied to the development business await indicators that the business has bottomed, and undertaking begins may speed up in early 2025, pushed by nascent rate of interest easing cycle and a doubtlessly smooth financial touchdown. We’re intently watching the Architectural Billing Index for indicators of an inflection. So far, it stays in barely contraction territory.

One Last Notice

As we mirror on our 5 years with Madison Investments, we’re reminded of the sturdy alignment between our funding philosophy and that of our teammates on the broader Madison U.S. Fairness Division. Once we joined the agency within the third quarter of 2019, the shared dedication to bottom-up, research-driven, high-conviction investing and a give attention to threat administration was instantly clear. Embracing the Take part and Defend method that Madison Investments is understood for got here naturally. Our core funding rules stay unchanged. We proceed to boost our collaboration with our U.S. Fairness colleagues in an effort to ship the perfect risk-adjusted funding returns attainable.

As all the time, we respect the chance to serve our purchasers.

Sincerely,

Faraz Farzam | Aaron Garcia

Disclosures

“Madison” and/or “Madison Investments” is the unifying tradename of Madison Funding Holdings, Inc., Madison Asset Administration, LLC (“MAM”), and Madison Funding Advisors, LLC (“MIA”). MAM and MIA are registered as funding advisers with the U.S. Securities and Change Fee. Madison Funds are distributed by MFD Distributor, LLC. MFD Distributor, LLC is registered with the U.S. Securities and Change Fee as a broker-dealer, and is a member agency of the Monetary Trade Regulatory Authority. The house workplace for every agency listed above is 550 Science Drive, Madison, WI 53711. Madison’s toll-free quantity is 800-767-0300.

Any efficiency information proven represents previous efficiency. Previous efficiency is not any assure of future outcomes.

Indices are unmanaged. An investor can not make investments instantly in an index. They’re proven for illustrative functions solely, and don’t characterize the efficiency of any particular funding. Index returns don’t embody any bills, charges or gross sales expenses, which might decrease efficiency.

Russell 2000®Index measures the efficiency of the two,000 smallest corporations within the Russell 3000® Index, which represents roughly 11% of the overall market capitalization of the Russell 3000® Index. The Russell 3000 Index measures the efficiency of the biggest 3,000 U.S. corporations representing roughly 98% of the investable U.S. fairness market. The Russell 3000 Index is constructed to supply a complete, unbiased and secure barometer of the broad market and is totally reconstituted yearly to make sure new and rising equities are mirrored. Russell Funding Group is the supply and proprietor of the logos, service marks and copyrights associated to the Russell Indexes. Russell® is a trademark of Russell Funding Group.

The Russell 2500 Index combines a portion of midcap shares with small cap shares – forming a “SMID” (small/mid) cap section of shares from the Russell 3000®.

The Structure Billings Index tracks the month-to-month billings of structure companies, providing an advance have a look at nonresidential building spending developments for the approaching 9 to 12 months. The index is derived from a month-to-month survey of structure companies throughout the U.S., and measures the modifications within the variety of design providers supplied to purchasers, reflecting the demand for architectural providers.

Madison’s expectation is that traders within the technique will take part close to totally in market appreciation throughout bull markets and expertise one thing lower than full participation throughout bear markets in contrast with traders in portfolios holding extra speculative and unstable securities. Subsequently, the funding philosophy is meant to characterize a conservative funding technique. There is no such thing as a assurance that Madison’s expectations relating to this funding technique shall be realized.

A foundation level is one hundredth of a %.

Non-deposit funding merchandise usually are not federally insured, contain funding threat, might lose worth and usually are not obligations of, or assured by, any monetary establishment. Funding returns and principal worth will fluctuate.

This report is for informational functions solely and isn’t meant as a proposal or solicitation with respect to the acquisition or sale of any safety.

Take into account the funding aims, dangers, and expenses and bills of Madison Funds rigorously earlier than investing. Every fund’s prospectus accommodates this and different details about the fund. Name 800.877.6089 or go to Madison Funds to acquire a prospectus and browse it rigorously earlier than investing.

Though the knowledge on this report has been obtained from sources that the agency believes to be dependable, we don’t assure its accuracy, and any such info could also be incomplete or condensed. All opinions included within the report represent the authors’ judgment as of the date of this report and are topic to vary with out discover.

Madison Asset Administration, LLC doesn’t present funding recommendation on to shareholders of the Madison Funds. Opinions acknowledged are informational solely and shouldn’t be taken as funding advice or recommendation of any type in any respect (whether or not neutral or in any other case).

Madison Funds are distributed by MFD Distributor, LLC, member FINRA.

Madison-619183-2024-10-09

Click on to enlarge

{kind=link}