Up to date on October thirteenth, 2023 by Bob Ciura

PepsiCo (PEP) lately elevated its dividend by 10%. This marks the corporate’s 51st consecutive yr of elevated dividends paid to shareholders.

In consequence, it’s on the checklist of Dividend Kings.

The Dividend Kings are a bunch of simply 50 shares which have elevated their dividends for a minimum of 50 years in a row. We consider the Dividend Kings are among the many highest-quality dividend progress shares to purchase and maintain for the long run.

With this in thoughts, we created a full checklist of all 50 Dividend Kings. You may obtain the complete checklist, together with vital monetary metrics akin to dividend yields and price-to-earnings ratios, by clicking on the hyperlink beneath:

PepsiCo is a recession-proof Dividend King with a management place within the meals and beverage business. It’s a dependable dividend progress inventory that may enhance its dividend, even throughout recessions.

On the identical time, the inventory has a market-beating 3.2% dividend yield. On account of its above-average yield and lengthy historical past of constant annual dividend will increase, PepsiCo stays a high-quality holding for revenue buyers.

Enterprise Overview

PepsiCo is a significant client staples inventory. It has a big portfolio of high quality manufacturers, together with greater than 20 particular person manufacturers that generate annual gross sales of $1 billion or extra. Just some of its core manufacturers embody Pepsi, Frito-Lay, Quaker, Gatorade, and lots of extra.

Supply: Investor Presentation

Its enterprise is almost equally cut up between its meals and beverage segments. Additionally it is balanced geographically between the U.S. and the remainder of the world.

On October tenth, 2023, PepsiCo introduced third quarter outcomes. Income elevated 6.7% to $23.45 billion whereas adjusted earnings-per-share of $2.25 elevated 14% year-over-year. Natural gross sales elevated 8.8% for the third quarter. For the quarter, beverage quantity was flat whereas handy meals have been down 2%.

PepsiCo Drinks North America’s income grew 9% organically as increased costs greater than offset a 4.5% decline in quantity. Frito-Lay North America elevated 12%, once more resulting from worth will increase, whereas quantity was flat. Quaker Meals North America grew natural gross sales 6% regardless of a 3% decline in quantity.

PepsiCo supplied an up to date outlook for 2023 as effectively, with the corporate anticipating adjusted earnings-per-share of $7.54 for the yr, up from $7.47, $7.27, and $6.93 beforehand. Natural gross sales are nonetheless projected to be increased by 10% for the yr.

Progress Prospects

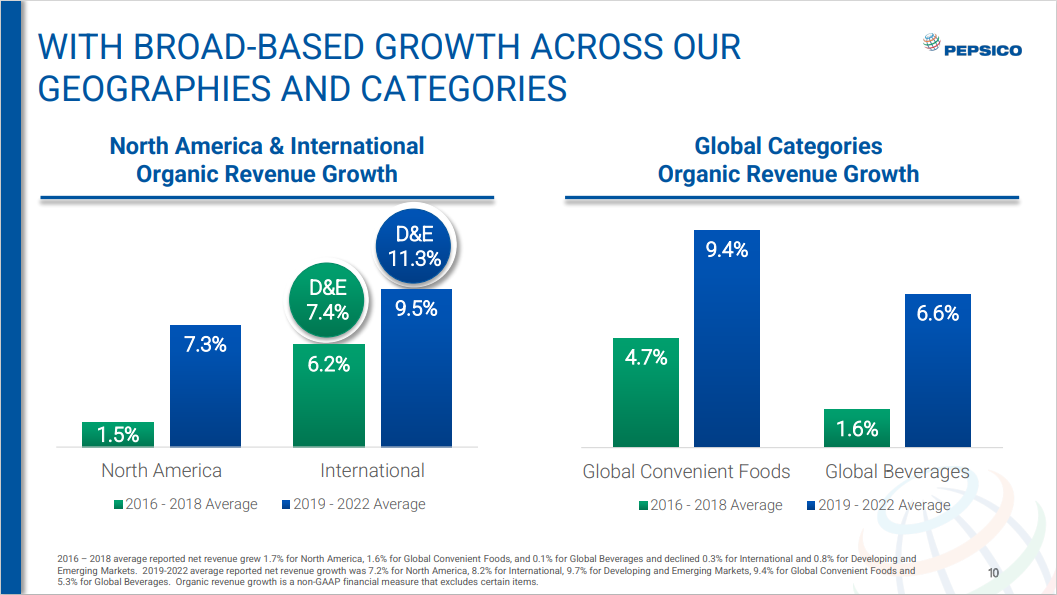

PepsiCo has an extended historical past of regular progress. Even in a difficult setting for soda, PepsiCo has continued its constant progress. An illustration of the corporate’s efficiency over the previous a number of years might be seen within the beneath picture.

Supply: Investor Presentation

We consider PepsiCo will generate round 5%-6% adjusted earnings-per-share progress per yr over the following 5 years. Going ahead, two of PepsiCo’s most promising catalysts are progress in more healthy meals and drinks, and in rising markets.

Gross sales of soda are slowing down in developed markets just like the U.S., the place soda consumption has steadily declined for over a decade.

In consequence, massive soda corporations like PepsiCo have needed to adapt to a extra health-conscious client. To do that, PepsiCo has shifted its portfolio towards more healthy meals which are resonating extra strongly with altering client preferences.

As well as, PepsiCo has an enormous progress alternative in rising markets like China, Africa, India, and Latin America. These are under-developed areas of the world with massive client populations and excessive financial progress charges.

Rising markets have been a progress driver as soon as once more final quarter. Latin America income elevated 12%, Asia Pacific/Australia/New Zealand/China area improved 7%, and Africa/Center East/South Asia was up 20%. Every area noticed an uptick in quantity.

Aggressive Benefits & Recession Efficiency

PepsiCo has quite a few aggressive benefits. Amongst them are sturdy manufacturers and a worldwide scale. In all, PepsiCo has over 20 particular person manufacturers that every gather a minimum of $1 billion in annual income. Robust manufacturers give PepsiCo optimum shelf house at retailers and provides the corporate pricing energy.

PepsiCo’s monetary energy additionally permits the corporate to spend money on analysis and growth, in addition to promoting, to retain its aggressive benefits.

For instance, PepsiCo invests billions every year in analysis and growth to innovate new merchandise and packaging designs. As well as, PepsiCo recurrently spends greater than $2 billion every year on promoting to take care of market share and construct model fairness with shoppers.

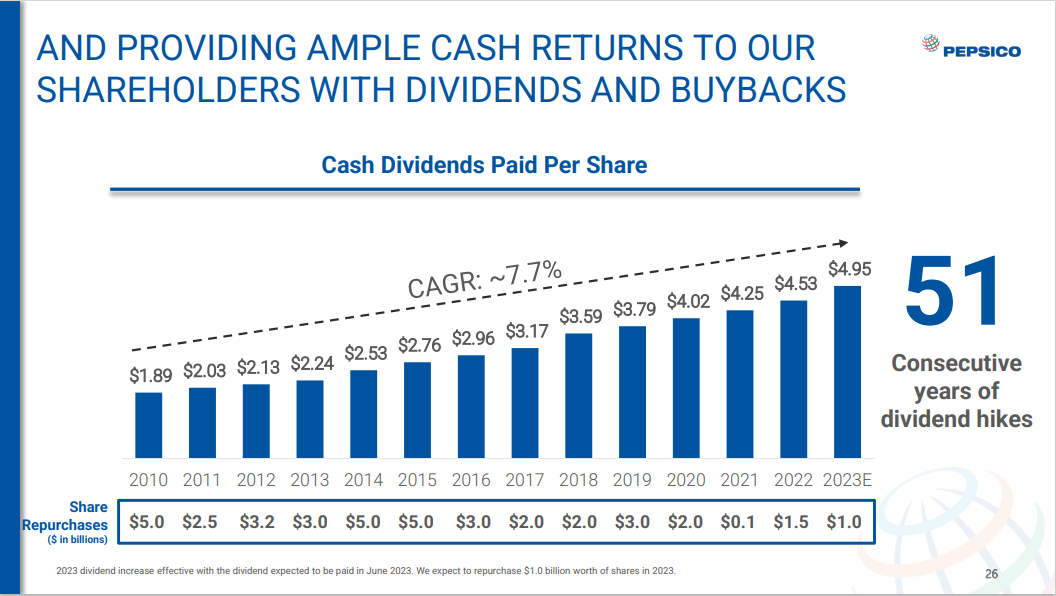

PepsiCo’s aggressive benefits and robust manufacturers make the corporate extremely worthwhile, even throughout recessions. Meals and drinks at all times retain a sure stage of demand, which is why the corporate held up so effectively in the course of the Nice Recession.

Supply: Investor Presentation

PepsiCo’s aggressive benefits and profitability have enabled the corporate to extend its dividend for 50 years straight. Since 2010, PepsiCo has elevated its dividend by 8% per yr on common.

PepsiCo’s earnings-per-share all through the Nice Recession of 2007-2009 are listed beneath:

2007 earnings-per-share of $3.34

2008 earnings-per-share of $3.21 (3.9% decline)

2009 earnings-per-share of $3.77 (17% enhance)

2010 earnings-per-share of $3.91 (3.7% enhance)

As you possibly can see, PepsiCo’s earnings-per-share declined solely modestly in 2008. The corporate proceeded to develop earnings by practically 20% in 2009, which may be very spectacular. Earnings continued to develop as soon as the recession ended.

The corporate reported sturdy progress in 2020 and 2021 when the coronavirus pandemic despatched the U.S. financial system right into a recession. Due to this fact, PepsiCo is a recession-resistant enterprise.

Valuation & Anticipated Returns

PepsiCo is anticipated to generate earnings-per-share of $7.54 for 2023. Primarily based on this, the inventory trades for a price-to-earnings ratio of 21.2. Our truthful worth estimate is a price-to-earnings ratio of 21.0. In consequence, the inventory is simply barely overvalued. A declining price-to-earnings ratio might cut back annual returns by 0.2% every year over the following 5 years.

In consequence, future returns will seemingly be comprised of earnings-per-share progress and dividends. We anticipate PepsiCo to develop earnings-per-share every year by 5.5%, consisting of natural income progress, acquisitions, and share repurchases.

As well as, PepsiCo additionally has a 3.2% present dividend yield. The mix of valuation adjustments, earnings progress, and dividends leads to whole anticipated returns of 8.5% per yr over the following 5 years.

We presently fee PepsiCo inventory a maintain.

PepsiCo has a safe dividend, with a projected dividend payout ratio of 67% for 2023. This offers PepsiCo sufficient room to proceed growing the dividend at a fee in-line with the expansion fee of its adjusted EPS.

Ultimate Ideas

PepsiCo is a high-quality firm with a various portfolio of sturdy manufacturers. Its long-term progress will probably be fueled by its snacks enterprise and by advancing in creating markets.

The corporate has elevated its dividend for 50 years in a row, and the inventory presently yields 3.2%. Due to this fact, it meets our definition of a blue-chip inventory, and it ought to proceed to ship regular dividend will increase every year.

If you’re fascinated about discovering extra high-quality dividend progress shares appropriate for long-term funding, the next Certain Dividend databases will probably be helpful:

The foremost home inventory market indices are one other strong useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.

{kind=link}