Kevin Dietsch/Getty Photos Information

With Apple (AAPL) showing to announce an exit from the Purchase Now, Pay Later area, Affirm (NASDAQ:AFRM) is trying like an more and more enticing guess. The corporate has posted torrid top-line progress together with quickly enhancing working margins. The corporate has a web money steadiness sheet and the Affirm Card is clearly gaining traction with shoppers. The corporate’s strong execution during the last a number of years within the excessive rate of interest atmosphere might counsel that bearish fears are overblown. I reiterate my purchase ranking for the inventory.

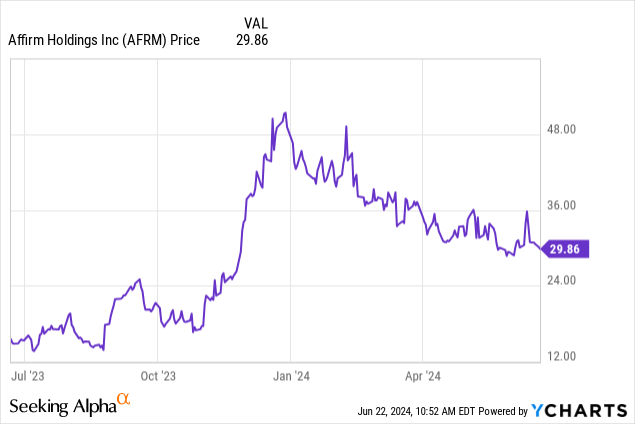

AFRM Inventory Worth

I final lined AFRM in April the place I rated the inventory a purchase on account of the gorgeous acceleration in high line progress. The inventory has underperformed the broader market since then.

Whereas the inventory has carried out strongly over the previous 12 months, this nonetheless appears to be like like early innings for this progress firm.

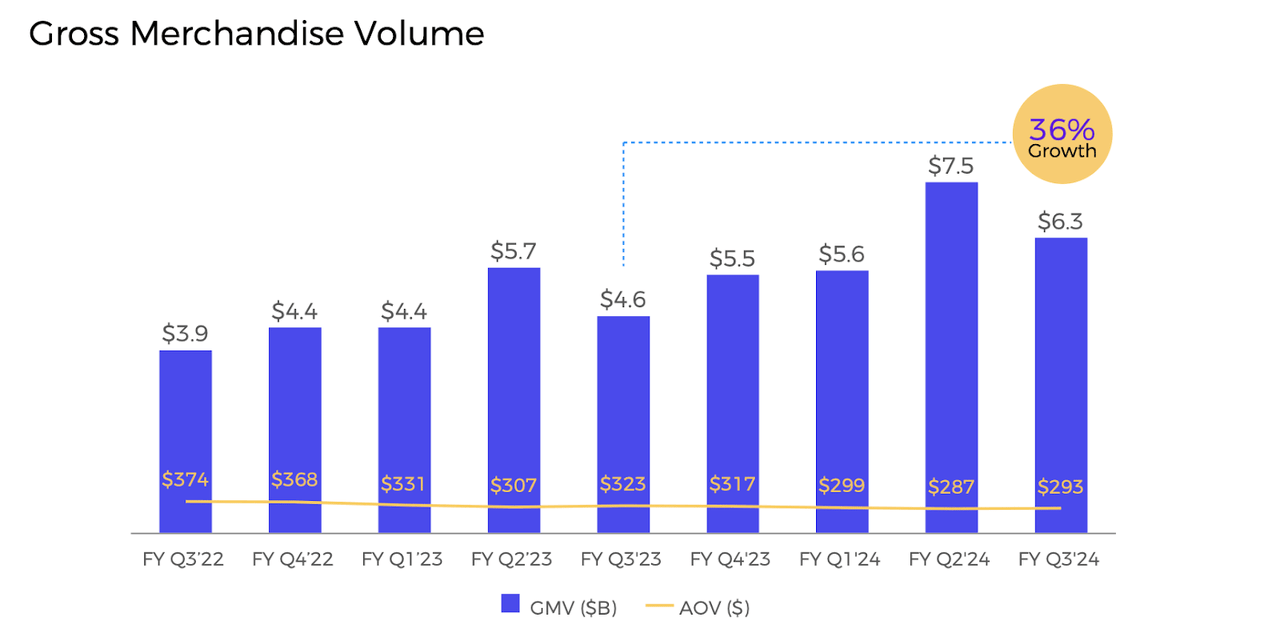

AFRM Inventory Key Metrics

AFRM is a number one purchase now pay later firm with a give attention to america. In essentially the most quarter, the corporate posted its 4th consecutive quarter of accelerating gross merchandise worth (‘GMV’) progress, with GMV rising 36% YoY.

FY24 Q3 Presentation

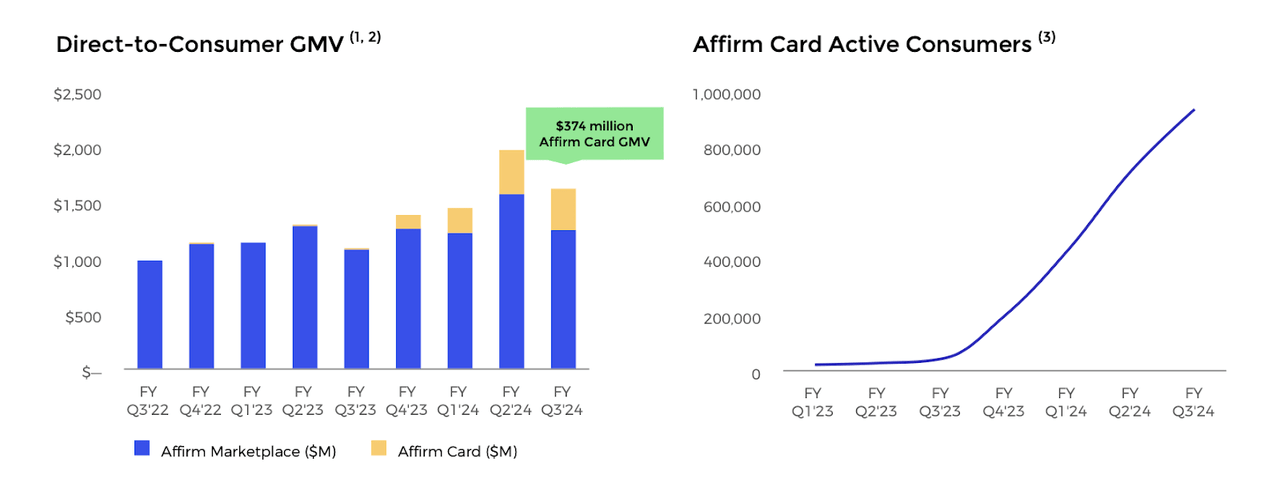

A considerable portion of that progress is being pushed by the Affirm Card, which has been a runaway success for the corporate.

FY24 Q3 Presentation

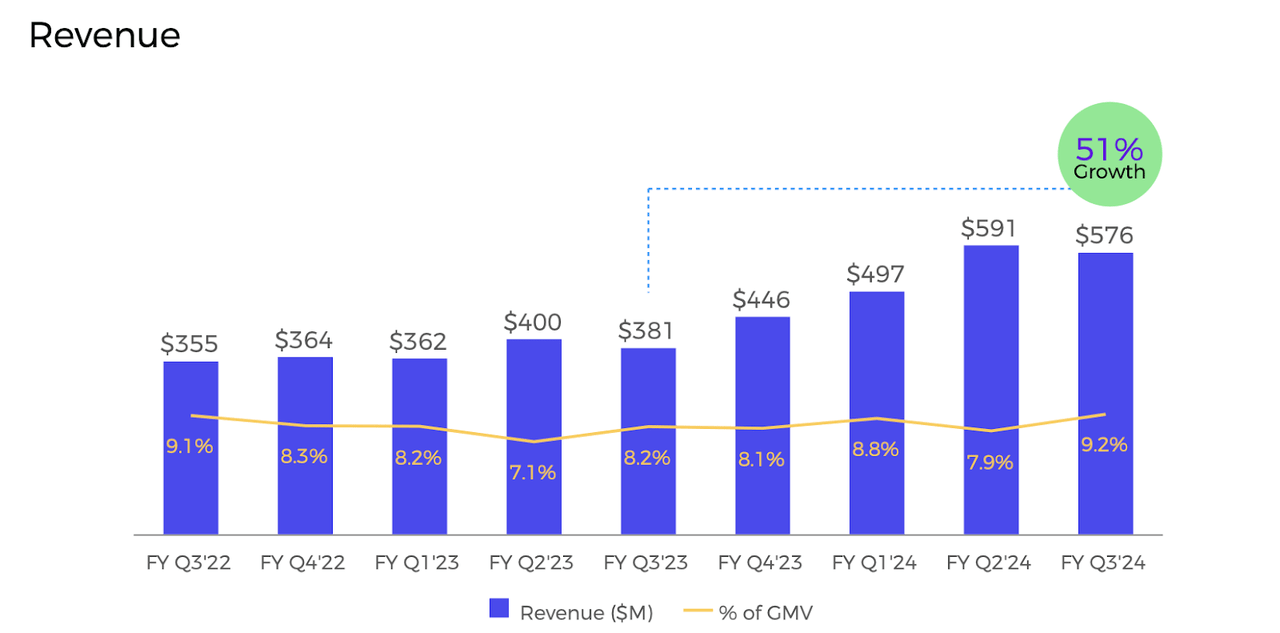

AFRM noticed income develop 51% YoY because it continues to profit from pricing initiatives. Recall that for a number of quarters following the rise in rates of interest, AFRM was unable to lift its personal APRs, resulting in decrease monetization charges relative to GMV.

FY24 Q3 Presentation

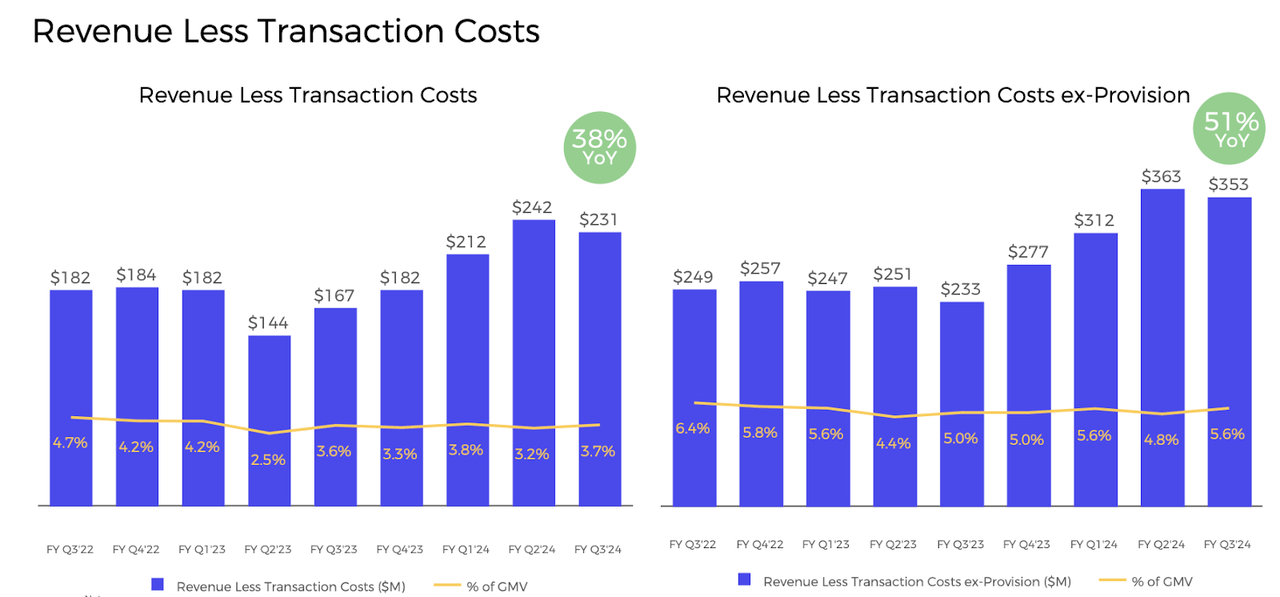

AFRM noticed income much less transaction prices develop at a 38% YoY clip, with 10 bps of margin growth YoY.

FY24 Q3 Presentation

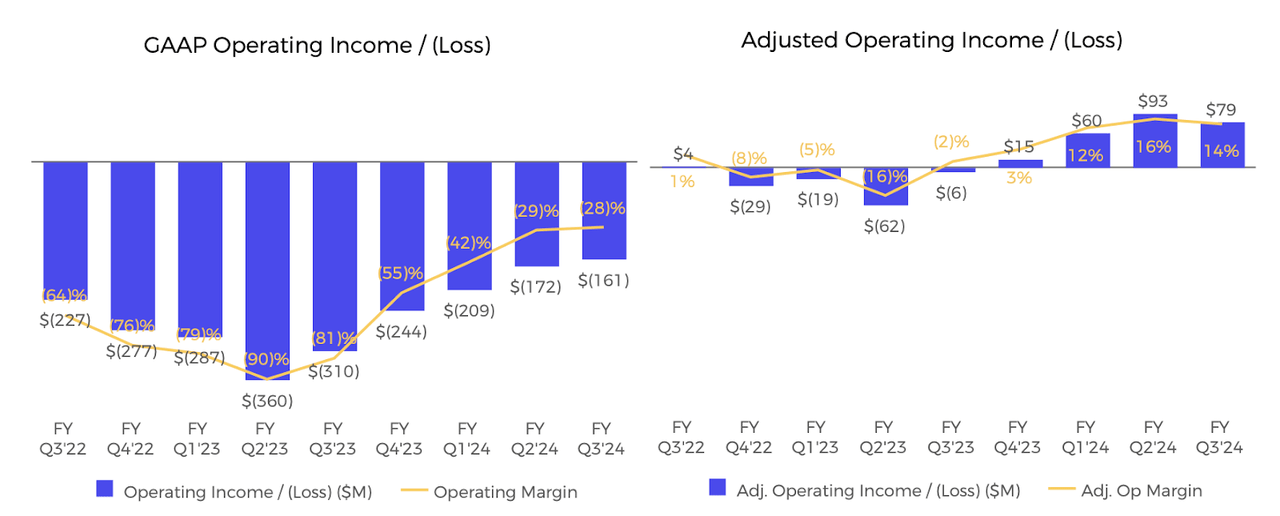

AFRM noticed its adjusted working margin swing from destructive 2% to constructive 14% YoY and made some progress on decreasing its GAAP working loss.

FY24 Q3 Presentation

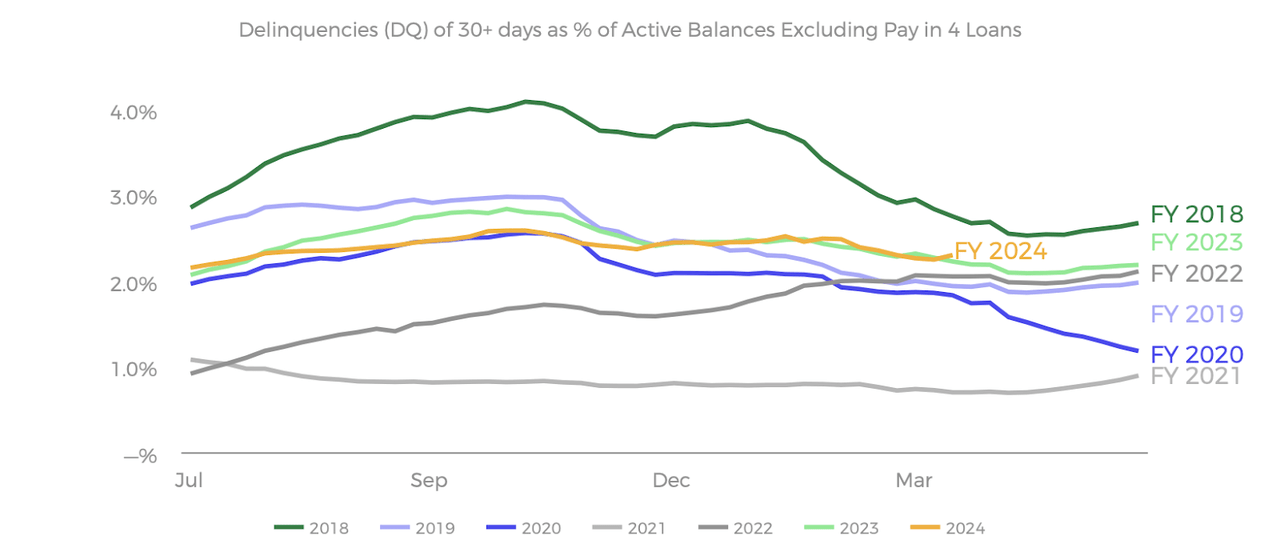

The corporate has seen its 30+ days delinquency development line very equally to final 12 months and never considerably worse than prior years. Bears had nervous that the BNPL market may face nice credit score danger amidst the upper rate of interest atmosphere, however AFRM has handed the take a look at with flying colours.

FY24 Q3 Presentation

The corporate ended the quarter with $1.6 billion of money versus $1.4 billion in convertible debt.

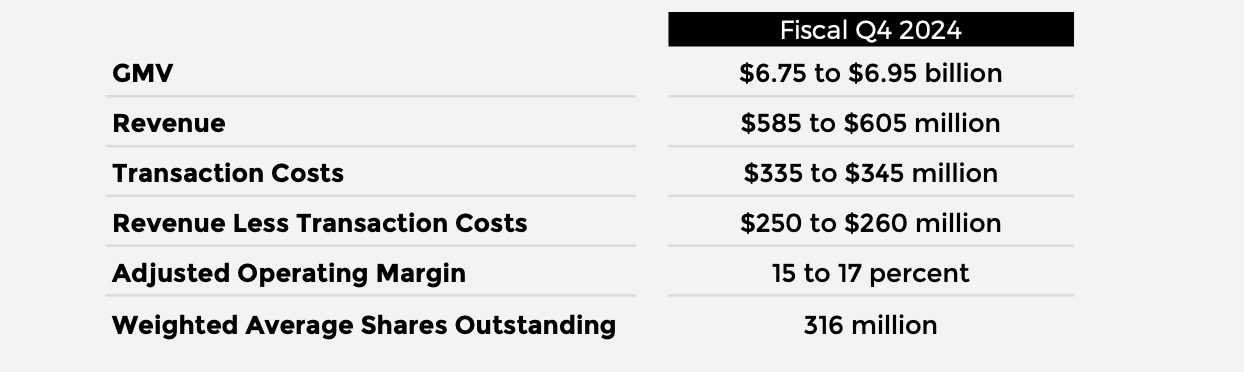

Wanting forward, administration has guided for as much as 26% GMV progress, 35.7% income progress, and adjusted working margins of as much as 17% (versus 3% within the prior 12 months)

FY24 Q3 Presentation

On the convention name, administration notably refused to instantly reply how a lot the pricing initiatives boosted progress. I feel it’s cheap to imagine that present progress charges are being considerably boosted by macro elements and will decelerate within the upcoming 12 months. Administration warned about upcoming robust comparables within the fourth quarter, stemming from that being the quarter through which they launched 36% APR caps. Administration additionally appeared to indicate that they view 20% top-line progress as being sustainable not less than within the medium time period.

Is AFRM Inventory A Purchase, Promote, Or Maintain?

Subsequent to the tip of the quarter, there was two necessary items of stories. First, the corporate was highlighted as coming to Apple Pay later this 12 months. Second, AAPL itself introduced that it’ll now not offer its personal BNPL product in america. In a single fell swoop, the “Huge Tech danger” story seems to have been addressed.

The inventory not too long ago traded palms at simply over 4x gross sales and 11x gross income.

Looking for Alpha

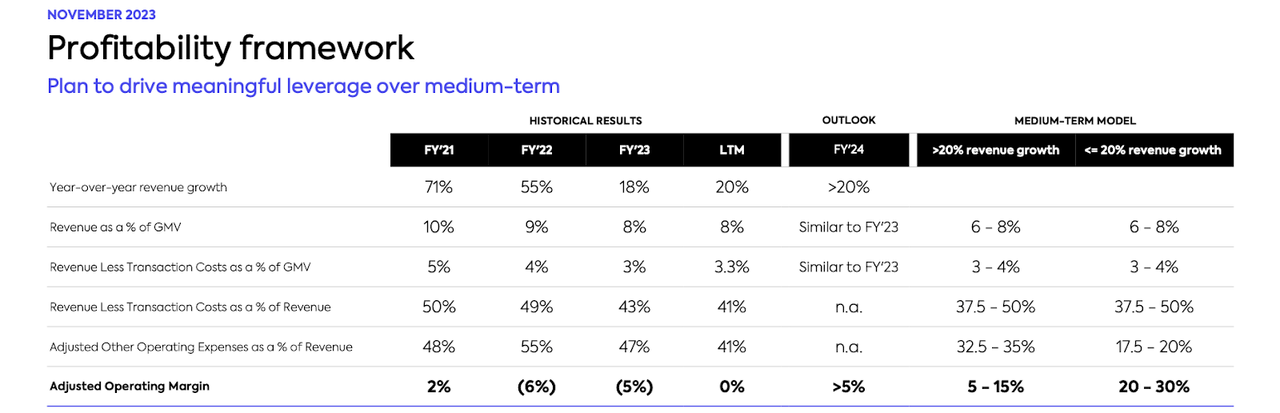

Administration has guided for 20% to 30% adjusted working margins as top-line progress decelerates under 20%.

November 2023 Presentation

Assuming 20% long run web margins, AFRM is buying and selling proper round 20x long run earnings. That appears like an inexpensive a number of given the 20% projected top-line progress fee subsequent 12 months. Plus, given the corporate’s strong monetary efficiency for the reason that rise of rates of interest, I’m of the view that the inventory doesn’t should commerce at discounted cyclical multiples. It have to be famous that the corporate’s BNPL loans are ultra-short length by design and the corporate doesn’t face fleeing-deposit danger on account of not being a conventional financial institution. Even when we assume gradual a number of compression to round 15x earnings (which nonetheless appears to be like greater than justifiable given the robust steadiness sheet), the inventory seems poised for market-beating returns if it could actually maintain 15% to twenty% progress for a few years.

AFRM Inventory Dangers

It’s potential that rates of interest rise once more, at which level AFRM may want one other time period to regulate their danger fashions and pricing. There are quite a few BNPL operators, it’s admittedly unclear if shoppers will stay loyal to at least one model. I think that the BNPL market may grow to be considerably just like what we’re seeing with PayPal (PYPL) branded processing, through which sure BNPL operators profit from a primary mover benefit earlier than dealing with competitors from different BNPL rivals on the checkout display screen. It’s notable that PYPL trades at low valuations, which is perhaps a disappointing foreshadowing for what may finally occur to AFRM.

AFRM Inventory Conclusion

AFRM is executing strongly with accelerating GMV progress and a strong push into non-GAAP profitability. AAPL’s newest slew of BNPL bulletins seem to disproportionately profit AFRM, with potential constructive influence to the valuation a number of. I see ongoing top-line progress as being sufficient to drive market-beating returns. I reiterate my purchase ranking for the inventory.

{kind=link}