We Are

What a distinction six months could make. I steered Agnico Eagle Mines Restricted (NYSE:AEM) as one of many smartest risk-adjusted treasured metals miners to personal in a bullish story on February tenth right here. Since then, this low value, the most secure jurisdiction gold producer has gained +78% (as a complete return) for traders vs. the equivalent-period S&P 500 index rise of +12%.

Searching for Alpha – Paul Franke, Agnico Eagle Article, February tenth, 2024

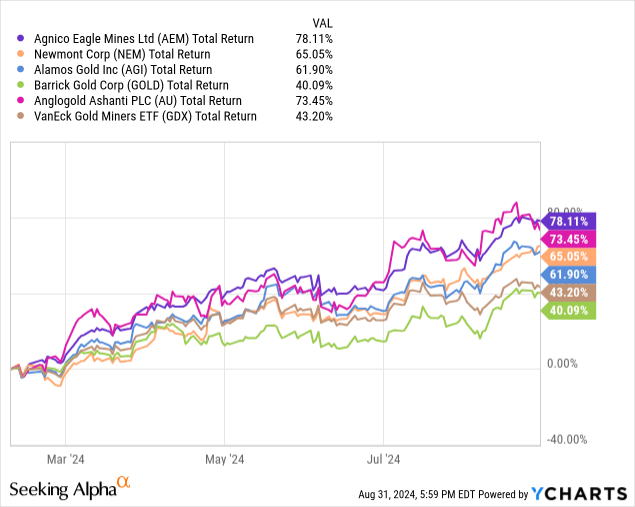

Actually, AEM has outlined the perfect whole return for traders out of the key gold miners you could possibly have picked, or sector common represented by the VanEck Gold Miners ETF (GDX). This record consists of Newmont (NEM), Alamos Gold (AGI), Barrick Gold (GOLD), and AngloGold Ashanti plc (AU).

YCharts – AEM vs. Gold Mining Friends, Whole Returns, Since February tenth, 2024

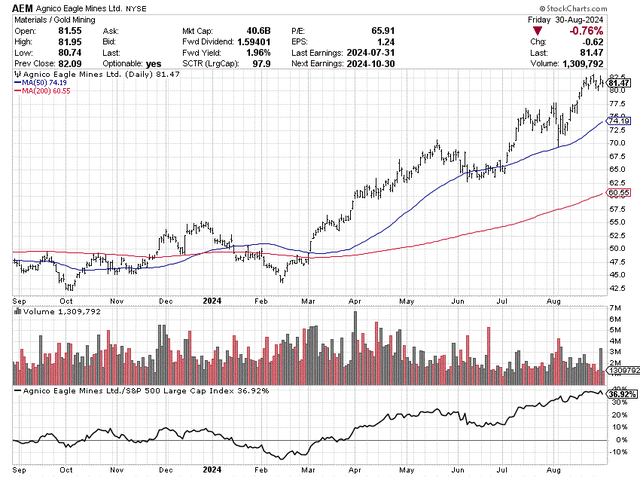

Nevertheless, issues change. Is Agnico affected by working issues? No. However, the valuation is getting considerably stretched. My present view is a breather might be subsequent, even when gold/silver bullion proceed to float increased the remainder of the yr. Do I counsel you promote your complete place? No. My considering is avoiding this identify as a purchase concept, or hedging your place with coated calls, or liquidating a small portion of your shares is smart right now. Consequently, I’m dropping my official 12-month score from Robust Purchase to Maintain.

StockCharts.com – Agnico Eagle, 12 Months of Every day Worth & Quantity Adjustments

Valuation-Primarily based Downgrade Logic

My view is the discount setup for all gold/silver miners from six months in the past and even a number of years in the past isn’t the identical right now. Positive, rising treasured metallic quotes (gold +28%, silver +17%) over the past 12 months ought to assist higher working ends in the second half of 2024 and all of 2025. But, the outsized gold miner positive factors of 2024 have largely discounted this excellent news.

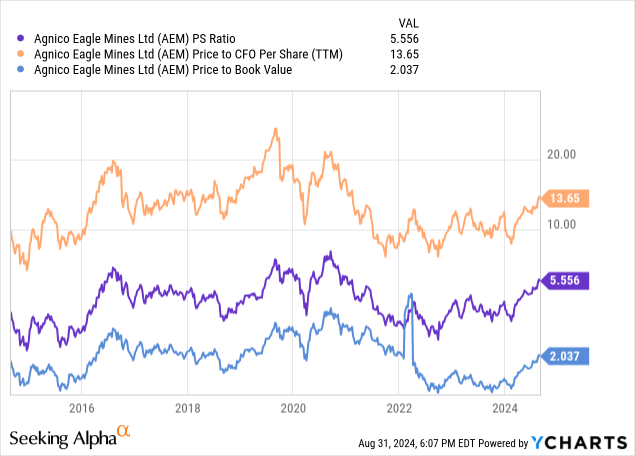

Reviewing a 10-year chart of AEM’s worth to trailing gross sales (5.5x), money circulate (13.6x) and e book worth (2x), the decade-low (or practically so) valuation setup of early 2022 to early 2024 is gone. The long-term investor benefit of buying-when-nobody-wants-them argument for gold miners that existed for years has considerably disappeared as nicely. Right this moment, I’d time period the share valuation zone for Agnico Eagle as nearer to honest, maybe shifting to completely cooked on additional worth positive factors.

YCharts – Agnico Eagle, Worth to Trailing Fundamentals, 10 Years

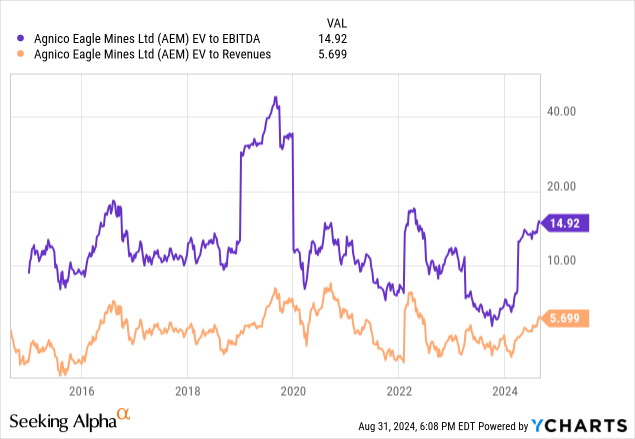

Once we embrace altering debt and money ranges, enterprise valuation ratios clarify an identical image. With EV to EBITDA (14.9x) and Revenues (5.7x) fairly a distance from six months in the past, and beginning to rise above 10-year averages, right now could be the correct time to noticeably take into account when to promote AEM than to purchase.

YCharts – Agnico Eagle, Enterprise Valuations, 10 Years

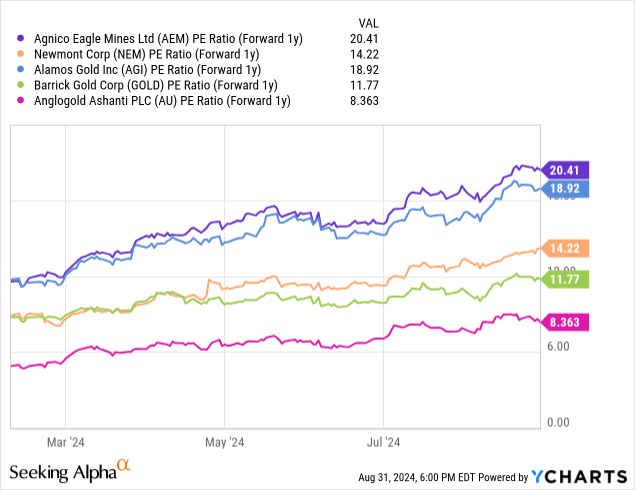

I’ll say a ahead 20.4x P/E on 2025 analyst estimates isn’t precisely costly traditionally. With the S&P 500 close to the identical quantity and Treasury payments out there at charges within the 4.6% to five.1% vary, AEM’s ahead earnings yield barely beneath 5% (E/P) is much from a sell-rated degree.

However, Agnico Eagle’s valuation on earnings estimates is the best of the mega-cap gold miners. After all, you possibly can argue higher useful resource belongings (areas and prices) must be priced at a premium, and I agree. But, the ahead 2025 P/E forecast has risen from 12x in February to 20x right now.

YCharts – AEM vs. Gold Mining Friends, Worth to Estimated 2025 Earnings, Since February tenth, 2024

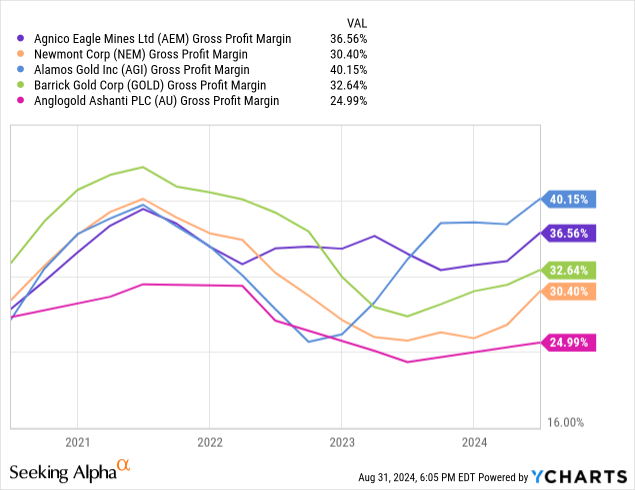

Gross margins are additionally a few of the strongest out of the peer group, which is a big plus if you wish to personal a miner. However, margins are usually not dramatically higher than the opposite main miners, with Newmont and Barrick probably catching AEM on additional gold worth positive factors into 2025.

YCharts – AEM vs. Gold Mining Friends, Gross Revenue Margins, 4 Years

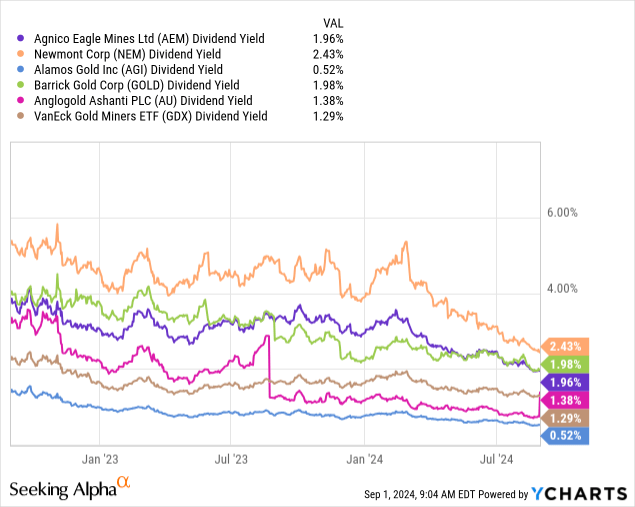

Lastly, dividend yields within the sector (together with AEM) are roughly half the extent of two years in the past. One of many best to argue excuses to personal the key gold miners in late 2022 revolved to dividend yields being superior to the general U.S. fairness market and people out there from T-bills. Agnico Eagle’s annual money distribution of just about 4% two years in the past and three.5% charge from February has declined to lower than 2% in late summer time 2024.

YCharts – AEM vs. Gold Mining Friends, Dividend Yields, 2 Years

Remaining Ideas

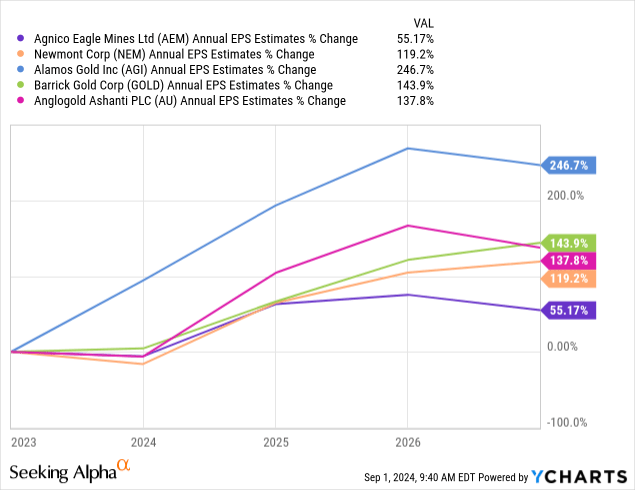

I suppose the first destructive information level working towards Angico Eagle shares throughout 2025 would be the realization that manufacturing development and working margin enchancment have turn out to be fairly subpar vs. the key mining teams. Why not personal a decrease valuation setup upfront with above-average development prospects?

YCharts – AEM vs. Gold Mining Friends, Analyst Estimates for EPS Progress 2024-26, Made August thirtieth, 2024

At this stage of the gold/silver rise, I a lot want Newmont’s place for brand spanking new funding. The advantages of the Newcrest Mining merger ought to actually shine by 2025 working efficiency. And, a bigger, extra diversified gold reserve base is available for purchase at a far decrease valuation than Agnico Eagle.

My analysis continues to be putting gold’s long-term underlying price round US$3000 per ounce and silver above $40 (utilizing relative valuation evaluation to different commodities, cash provide, debt creation within the U.S. because the Nineteen Sixties). So, the dear metals bull run ought to proceed, albeit at a slower proportion acquire tempo over the following 6-12 months, than we have skilled because the finish of 2023.

If China does one thing loopy, or Russia expands its warfare with Ukraine by attacking neighboring nations, or the Center East state of affairs turns into extra unstable with Iran getting straight concerned with Israel, an overshoot of my metals worth targets will turn out to be more and more seemingly. Relying on the financial and political circumstances, $4000 to $5000 gold and $80 to $100 silver might arrive ahead of most traders or residents of the world consider attainable. Given that is our future, Agnico Eagle ought to proceed to outperform the S&P 500 by a large margin.

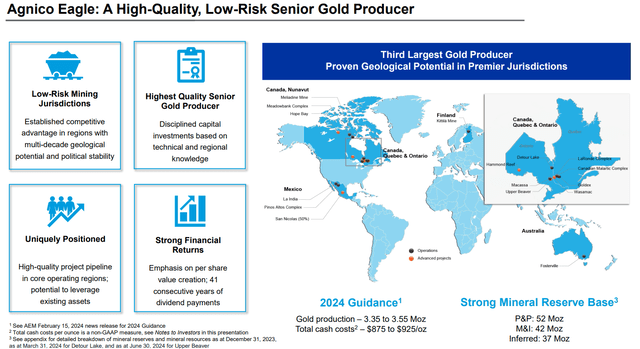

Agnico Eagle – August 2024 Investor Presentation

Eventual AEM targets of $120 to $160 per share are very lifelike a couple of years out. Nevertheless, the simplest a part of the dear metallic mining advance might be over, particularly if international fairness markets take successful quickly.

Essentially the most affordable buying and selling situations I’m modeling with a slower financial system and sizable U.S. inventory market decline might imply Agnico Eagle’s inventory worth will commerce between $70-$90 over the following 12 months. This forecast conclusion is forcing me to downgrade shares from Robust Purchase to Maintain, utilizing a 1-year outlook as my yardstick.

Proudly owning Agnico Eagle as a part of a diversified portfolio of gold/silver belongings stays a brilliant concept. I’m simply not as excited to purchase shares at this stage of fluctuations within the numerous monetary markets. I personally not maintain a stake, as I want to focus my gold buying and selling/investing on the most affordable options, comparable to Newmont. But, for long-term traders not buying and selling the gold sector each day, I consider sustaining an AEM place continues to be applicable.

Thanks for studying. Please take into account this text a primary step in your due diligence course of. Consulting with a registered and skilled funding advisor is beneficial earlier than making any commerce.

{kind=link}