lenscap67

Article Thesis

Anheuser-Busch InBev (BUD) is a number one beer and alcohol firm that has had a troubled yr. Whereas latest outcomes have been bettering, the corporate does however not look particularly robust proper right here. With its low yield, Anheuser-Busch InBev is not particularly enticing at present costs, I imagine.

Previous Protection

I’ve coated Anheuser-Busch InBev a number of instances right here on Searching for Alpha, most not too long ago in April 2023, a bit of greater than a yr in the past. I referred to as the corporate a dangerous funding again then and gave AB InBev a “Promote” score. Since that article was revealed, Anheuser-Busch InBev has underperformed the market by a hefty 36%, dropping 5% whereas the S&P 500 (SPY) rose 31% over the identical timeframe. In at the moment’s article, I’ll replace my thesis, accounting for latest outcomes and the now considerably decrease valuation.

Anheuser-Busch InBev: The Bud Gentle Hit

Round a yr in the past, Anheuser-Busch InBev made the information with an advert marketing campaign for one in every of its manufacturers, Bud Gentle, that wasn’t well-received by lots of the firm’s clients. A boycott started, and gross sales volumes for AB InBev’s Bud Gentle model began to say no. In lots of different instances, boycotts grew to become much less extreme over time, as shoppers both overlook in regards to the boycott, or they see it as much less essential as time passes and start, as soon as once more, to buy the gadgets that they boycotted for a while.

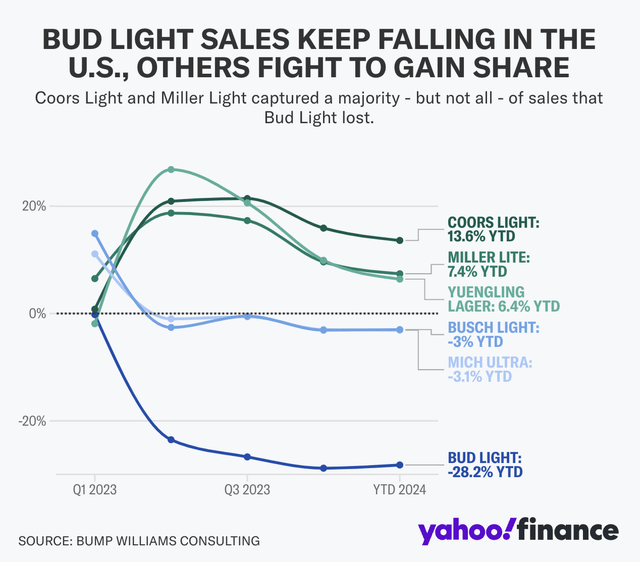

Anheuser-Busch InBev has, a minimum of up to now, not seen a serious restoration from the boycott. Current outcomes present that Bud Gentle gross sales are nonetheless down significantly in comparison with the place they had been earlier than the failed advert marketing campaign:

Bud Gentle gross sales (Yahoo finance / Bump Williams Consulting)

The decline of round 28% continues to be substantial, though marginally higher in comparison with the outcome in the direction of the tip of 2023. It’s price noting that another manufacturers, similar to Busch Gentle and Michelob Extremely, have reported small gross sales quantity declines within the year-to-date interval as properly, though different mild beer manufacturers, similar to Coors Gentle from Molson Coors Beverage Firm (TAP) are performing properly, probably partly as a consequence of the truth that some earlier Bud Gentle drinkers have switched to totally different manufacturers.

Even when the misplaced clients had been to by no means come again, the boycott might be lapped any more. Whereas gross sales could stay down in absolute phrases, the Q2 and later outcomes shouldn’t present a significant relative decline any longer as a consequence of this base impact. I thus imagine that Anheuser-Busch InBev ought to have the ability to report an improved gross sales quantity efficiency for the present quarter and in the course of the second half of the yr — a minimum of so long as the beer market, general, continues to stay intact.

Bud Gentle is just one model out of Anheuser-Busch InBev’s portfolio, and plenty of different manufacturers did means higher than Bud Gentle in latest quarters, even whereas Bud Gentle was negatively impacted by the aforementioned boycott. The boycott additionally was principally focused on the US, which means the model’s efficiency in different markets wasn’t as unhealthy.

General, AB InBev’s outcomes had been thus not too unhealthy in the latest quarter. General company-wide gross sales volumes within the US had been down, primarily because of the Bud Gentle boycott, however the firm benefitted from larger gross sales volumes in non-US markets such because the Center Americas, South America, Africa, and Europe. Whereas the boycott nonetheless has a unfavorable influence on AB InBev, the corporate’s good diversification, each geographically and relating to its many various manufacturers, lessens the influence of the boycott drastically. General, company-wide gross sales volumes had been down by 0.6% throughout the latest quarter. The corporate additionally elevated its costs in comparison with one yr earlier, which was sufficient to create a small income improve of two%, relative to 1 yr earlier.

Whereas this is not super-strong development, it’s good to see that the corporate managed to generate a minimum of some enterprise development regardless of ongoing headwinds. In the course of the earlier quarter, revenues had been down 1% on a year-over-year foundation, thus Q1 additionally was a sequential enchancment. It’s anticipated that outcomes will proceed to enhance all through the approaching quarters, as we will see within the following desk exhibiting the analyst consensus estimates for Q2 to Q1 2025:

AB InBev gross sales estimates (Searching for Alpha)

To me, this looks like an inexpensive estimate. With the start of the boycott being lapped, comparisons ought to get simpler, which means relative income development ought to profit, all else equal. It is usually price noting that the second and third quarters ought to profit from two main sporting occasions: Beginning this weekend, the European soccer championship (“EURO 2024”) will start, whereas the summer season Olympics in Paris will start six weeks from now. Consumption of beer will naturally additionally rely upon elements such because the climate and which groups are doing properly (or not), however general, main sporting occasions are a tailwind for beer consumption. With its giant portfolio of various manufacturers, AB InBev has a superb probability to learn from these two giant summer season sporting occasions, I imagine.

In relation to profitability, Anheuser-Busch InBev noticed its EBITDA develop by round 5% throughout the latest quarter, which is a really stable development price for a shopper staples inventory similar to AB InBev. The truth that EBITDA development was stronger than the income development that the corporate generated can also be optimistic. The corporate states that the margin growth was made doable by a mix of a shift in its product combine and by disciplined value administration, e.g. in overhead. That is excellent news, as tight value controls can create worth for shareholders when an organization retains rising its enterprise whereas ensuring that bills are rising at a below-average tempo — the following working leverage leads to income rising quicker in comparison with revenues. Earnings per share development throughout the latest quarter was enticing, at 16%, benefitting from larger revenues, though it’s price mentioning that the comparability to the earlier yr’s quarter wasn’t laborious.

Is BUD A Good Funding?

In my most up-to-date article on Anheuser-Busch InBev, I referred to as the corporate a Promote, as a consequence of a excessive valuation and the headwinds from the Bud Gentle boycott. With the boycott being lapped now, and with shares being down since my final article, AB InBev doesn’t look as unhealthy any longer.

At present costs, Anheuser-Busch InBev is buying and selling for 18x this yr’s anticipated web income. That is higher than the 20x web earnings a number of AB InBev traded at one yr in the past, though it’s price mentioning that AB InBev continues to be not the most cost effective beer firm by far. Competitor Heineken N.V. (OTCQX:HEINY) trades for simply 13x ahead web earnings, for instance, whereas Molson Coors Beverage Firm trades at a really low 9x this yr’s web earnings. On a relative foundation, AB InBev is thus removed from low cost and nonetheless trades at a premium in comparison with a few of its friends within the beer trade.

The dividend yield, at 1.5%, is just not sufficient to make AB InBev into a beautiful earnings inventory, I imagine. Whereas the corporate provided larger dividends not too way back and would possibly get again to providing a considerably larger payout once more sooner or later, the dividend is just not a serious plus at the moment. Its friends Heineken and Molson Coors supply larger dividend yields, which is explainable by the truth that they commerce at decrease valuations, which makes the dividend yield rise, all else equal.

General, I give AB InBev a Impartial or Maintain score at the moment. Issues look higher than they did a yr in the past and the inventory is cheaper now, each in absolute phrases (inventory value) and in relative phrases (valuation). The large sporting occasions this summer season may be a tailwind for the corporate and the whole trade. However AB InBev nonetheless trades at considerably larger valuations in comparison with a few of its friends, which is why I imagine that these looking for publicity to the beer trade could also be higher off shopping for one in every of BUD’s rivals.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

{kind=link}