David Tran

Introduction

There aren’t many monetary shares that readers deliver up as typically as BlackRock (NYSE:BLK), the monetary large that has turn out to be one of many titans of the fashionable monetary world.

It is no shock that readers hold mentioning this inventory:

It’s the greatest ETF supplier on this planet, even beating Vanguard. Whereas I often do not spend money on ETFs, many members of the family and buddies of mine have invested their hard-earned money in BlackRock-owned ETFs (iShares). It has more and more made headlines, as the large has used its energy to push for its agenda on among the corporations it owns. In response to the famend Australian Monetary Evaluation:

[…] Fink has made himself the face of the motion since 2016, when he started urging the chief executives of the businesses in BlackRock’s portfolio, in more and more strident phrases, to make their companies extra sustainable. – AFR

As I’ve typically mentioned in varied feedback, I’ve a difficulty with the way in which BLK has used its energy. It has turn out to be a extremely politicized firm that constantly makes information headlines (not at all times voluntarily), together with this one from final yr, when it was focused by two Republican candidates for the Presidency.

CNBC

That mentioned, I am not writing this text as an activist. I respect the corporate for what it has finished for its shareholders and buyers utilizing its merchandise, which brings me to the third level that explains why folks hold mentioning BLK within the remark sections of my articles.

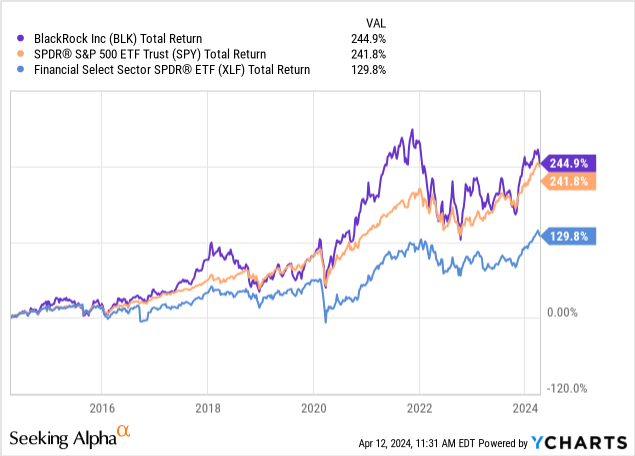

Since 2004, the inventory has returned 15% per yr, which has helped numerous folks attain their monetary objectives. Over the previous ten years alone, the BLK ticker has returned 245%, beating the S&P 500 by roughly 3 factors and the Monetary Choose Sector ETF (XLF) by greater than 110 factors.

My most up-to-date article on this inventory was written on December 6, once I went with the title “It Could Be Pointless To Wager In opposition to BlackRock.”

Again then, I wrote the next:

On a long-term foundation, I am bullish on BLK, because it appears to be a powerhouse that can solely enhance its moat within the years forward, letting shareholders profit from constant dividend progress, buybacks, and earnings progress alongside the way in which.

Just a few months later, BLK is buying and selling 5% increased after simply revealing its quarterly earnings.

Now, it is time for an replace.

So, with none additional ado, let’s get proper to it!

BlackRock Firing On All Cylinders

I simply talked about that BLK is “massive.”

Let me present some extra proof of that.

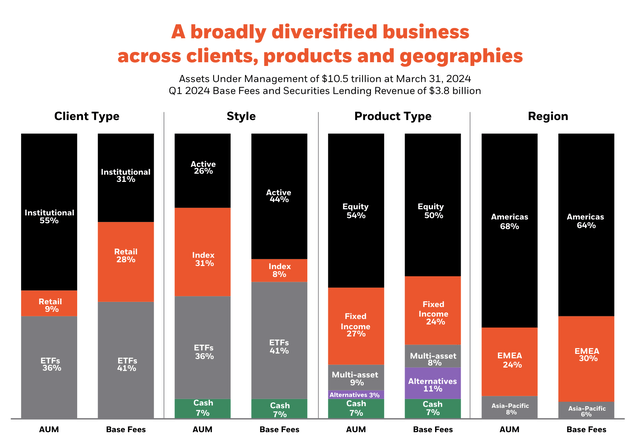

As of March 31, 2024, the corporate has $10.5 trillion in belongings beneath administration. Whereas it is a pointless comparability, it is roughly 2.6x the German GDP in 2022.

Greater than half of those belongings are managed for institutional shoppers. 45% is managed by retail accounts and ETFs.

You in all probability would not have guessed it, as BLK is thought for its ETFs, however 44% of its charges are generated by energetic administration.

BlackRock

The Americas account for 64% of complete price revenue, which leaves numerous room for progress in “worldwide” markets, which the corporate is focusing on by new product choices and companies.

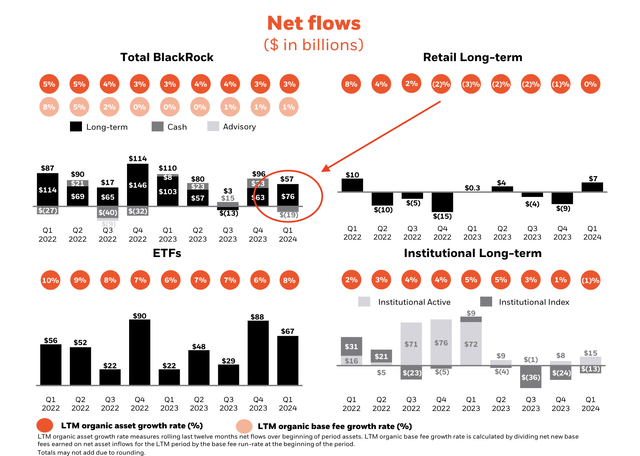

Probably the most vital metrics for BLK is the web inflows of money. In spite of everything, the additional cash it manages, the extra charges and efficiency revenue it may generate.

Within the first quarter, the corporate noticed long-term internet inflows of $76 billion. I highlighted this quantity within the overview beneath.

BlackRock

In response to the corporate, this exceeds business requirements and gives a powerful foundation for natural base price progress – which is considerably apparent.

Notably, ETF internet inflows had been led by core fairness and fixed-income ETFs, whereas monetary advisers are more and more on the lookout for personalized portfolio options. These contribute to progress throughout BlackRock’s SMA (individually managed accounts) and managed mannequin platforms.

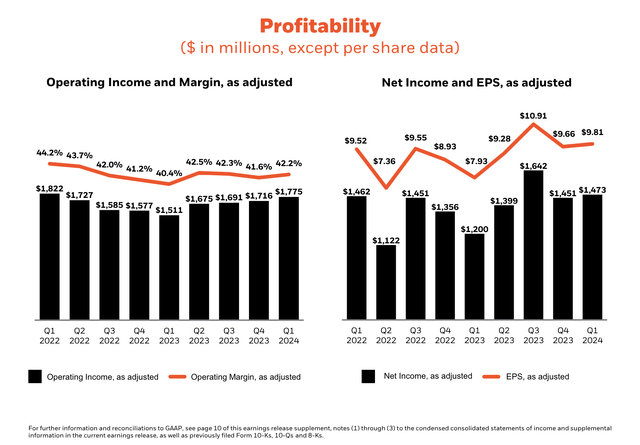

Furthermore, the corporate’s income surged by 11% year-over-year, reaching $4.7 billion, pushed by market appreciation and elevated income from efficiency charges and know-how companies.

Adjusted working revenue additionally noticed a notable uptick of 17% in comparison with the earlier yr. Earnings per share (“EPS”) got here in at $9.81, which is 24% increased in comparison with the prior-year quarter.

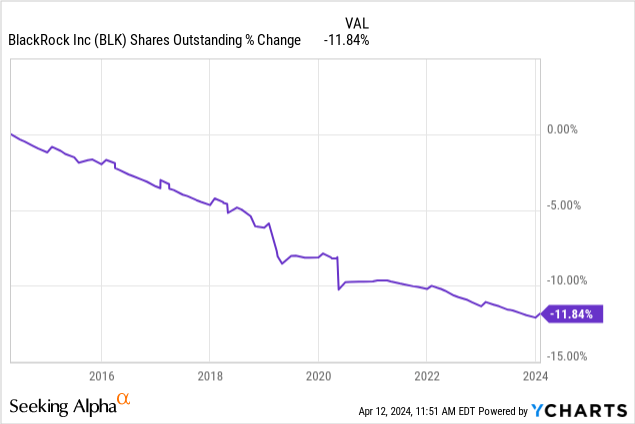

On a aspect be aware, the EPS quantity advantages from buybacks, because it exhibits earnings PER SHARE. Over the previous ten years, BLK has purchased again 12% of its shares.

That doesn’t make it an excessively aggressive buyback firm, but it surely definitely added to its spectacular complete return.

Furthermore, the corporate reported a rise in working revenue margins.

Working margins in 1Q24 had been increased on a month-on-month and year-over-year foundation. Particularly in an inflationary atmosphere, sustaining robust margins is essential.

BlackRock

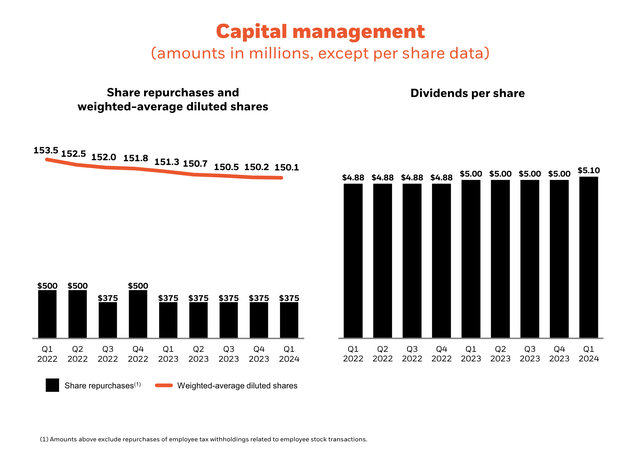

Because of robust fundamentals, the corporate hiked its dividend to $5.10.

This interprets to a $20.40 annual per-share dividend and a yield of two.6%. Assuming analysts are proper and BLK generates $41 in EPS this yr (FactSet information), we’re coping with a extremely favorable payout ratio of simply 50%.

BlackRock

Thus far, so good.

What issues much more is how the corporate is evolving, as this paves the way in which for future progress.

A Path To Constant Progress

Throughout its earnings name, the corporate made clear that it stays very optimistic about its progress prospects, particularly as shoppers proceed to “re-risk” (a flowery manner of claiming buyers are returning to the market) and market situations turn out to be extra supportive.

Even higher, due to these tailwinds, the corporate expects to broaden its market share.

Wanting forward, as markets pattern to be extra supportive and shoppers rerisk, we see vital alternative to broaden our market share and consolidate our place to shoppers. We have set ourselves as much as be a structural grower with the diversified platform that we have constructed. – BLK 1Q24 Earnings Name

Furthermore, in the course of the name, Mr. Fink highlighted the rising demand for infrastructure investments globally, pushed by components comparable to technological developments, globalization, financial progress in rising markets, and the necessity for brand spanking new infrastructure.

He has mentioned this subject so much this yr, and I included it in some articles this month (like this one).

On this case, the corporate’s infrastructure platform noticed 19% natural asset progress in comparison with final yr. Furthermore, the deliberate mixture with GIP (World Infrastructure Companions) is anticipated to additional broaden the corporate’s options on this space.

BlackRock

Furthermore, the corporate is seeing nice advantages from the launch of latest ETFs.

For instance, its Bitcoin fund, which launched in January, grew to become the fastest-growing ETF in historical past! It now has $20 billion in Bitcoin AUM.

On prime of that, energetic ETFs additionally noticed robust inflows.

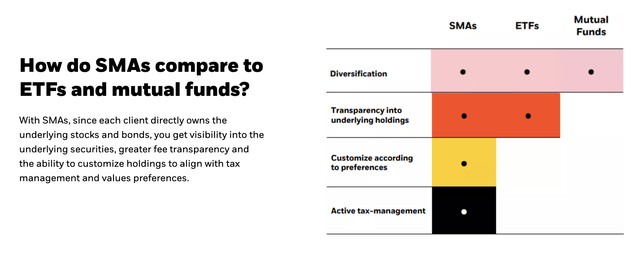

Typically talking, the corporate is seeing elevated demand for personalisation in its wealth enterprise, primarily by individually managed accounts (the aforementioned SMAs).

BlackRock

To capitalize on increased demand, the corporate continues to strengthen its SMA capabilities by acquisitions and natural progress.

Additionally it is more and more specializing in a subject that’s getting extra consideration in my In search of Alpha articles: retirement investing.

In response to Mr. Fink, the corporate is dedicated to offering retirement options, with a deal with serving to people each save for and spend all through retirement.

For instance, the corporate’s LifePath goal date franchise has seen vital progress and evolution through the years, and the introduction of LifePath Paycheck goals to deal with the de-accumulation problem by offering a possible lifetime revenue stream.

BlackRock

Final however not least, Larry Fink addressed political polarization.

I’ve spoken earlier than concerning the concern we see right now, some is stoked by more and more political polarization on this planet. Our business and BlackRock have been a topic of political dialogue, principally in the USA. We acknowledge a few of this with being the business chief. Now we have finished a greater job now of telling our story so that folks could make selections primarily based on details, not on lies and never on misinformation or politicization by others. – BLK 1Q24 Earnings Name

Furthermore:

As a fiduciary, politics ought to by no means outweigh efficiency. I do consider that with the overwhelming majority of our shoppers, our long-term fiduciary method and efficiency are resonating. We heard it in our dialogue with them and we see it in our flows, and I do know all of you as shareholders see it in our flows. – BLK 1Q24 Earnings Name

So, what concerning the valuation?

Valuation

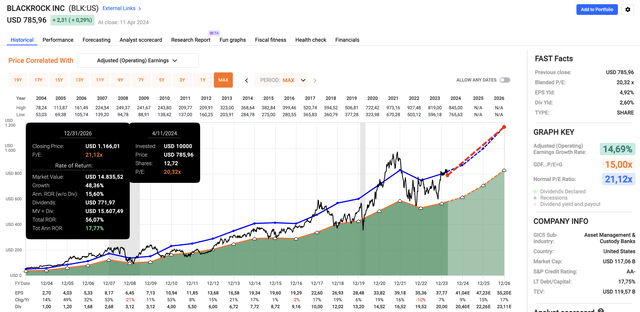

Technically talking, BLK stays in an ideal place to generate substantial returns.

Utilizing the info within the chart beneath, the corporate is buying and selling at a blended P/E ratio of 20.3x, which is barely beneath its long-term normalized P/E ratio of 21.1x.

This yr, EPS progress is anticipated to be 9%, doubtlessly adopted by 15% and 17% progress in 2025 and 2026, respectively.

FAST Graphs

Assuming the corporate retains a 21.1x a number of, it might return north of 15% per yr, together with its 2.6% dividend.

That mentioned, that is utterly theoretical.

Provided that inflation numbers hold coming in scorching and the Fed could also be pressured to maintain charges increased for longer, the financial system is liable to dangers that weren’t anticipated going into this yr.

Therefore, I’d not be shocked if we had been to see a decline to the $600-$650 vary.

If I had been on the lookout for extra monetary publicity, I’d be on the lookout for an entry in that vary – assuming the financial system doesn’t worsen.

All issues thought of, I keep on with a Purchase ranking, as I consider that BLK has the best instruments to proceed to use huge progress alternatives within the world monetary sector.

Takeaway

In conclusion, BlackRock continues to dominate the monetary world with its huge belongings beneath administration and spectacular progress trajectory.

Regardless of occasional controversies, its constant efficiency and dedication to shareholder worth make it a compelling funding selection.

With a various platform and a deal with increasing market share, BLK is well-positioned to capitalize on rising alternatives, significantly in infrastructure and retirement investing.

Whereas we might even see some volatility this yr, I keep a Purchase ranking, as I count on that BLK will proceed to face out in a extremely aggressive monetary sector.

Professionals & Cons

Professionals:

Sturdy Efficiency: BLK has delivered spectacular returns through the years, outperforming the market and its monetary sector friends. Various Choices: With a variety of ETFs and energetic administration choices, BLK caters to numerous investor sorts. Progress Alternatives: The enlargement into infrastructure investments and retirement options presents promising progress alternatives. Dividend Progress: BLK’s constant dividend will increase (and buybacks) replicate its dedication to rewarding shareholders.

Cons:

Political Sensitivity: BLK’s proactive stance on sustainability and political points might trigger potential backlash. Valuation Dangers: Regardless of its robust fundamentals, considerations over inflation and rates of interest might result in volatility. Market Dependency: On the whole, BLK’s efficiency is intently tied to market situations, making it liable to fluctuations and financial uncertainties.

{kind=link}