J Studios

At present, we enterprise again into the world of the best yielding actual property. Straying from our standard dialog of fairness REITs, we often peer over the fence to the debt facet of the equation. This was the case for our prior protection of the Blackstone Mortgage Belief (NYSE:BXMT), one of many largest diversified mortgage REITs on the planet, managed by the legendary asset supervisor Blackstone (BX).

Our most up-to-date protection of BXMT got here throughout a particular time that we affectionately nicknamed March mREIT Insanity because of the carnage attributable to rates of interest. Close to the start of the 12 months, Ares Industrial Actual Property (ACRE) turned one of many largest victims of the industrial actual property carnage, forcing a minimize to the dividend. Concern unfold all through the mREIT world as traders started to marvel if points backstage have been extra important than initially believed.

In April, we revealed an article on BXMT, shortly after ACRE’s dividend minimize and BXMT’s This fall earnings launch. The article was titled “Blackstone Mortgage Belief: Ample Dividend Protection Helps Defend From Ongoing Points” and mentioned two offsetting issues for BXMT traders. There have been clear indicators of hassle brewing, together with three new impairments through the quarter, which have been coated on the earnings name. But it surely appeared that administration was proactive in tackling these points, and the REIT’s 123% dividend protection would supply respiratory room for extra points.

Our thesis may very well be boiled right down to the next excerpt from the conclusion:

BXMT earns a Maintain ranking underneath present market circumstances. On one hand, mREITs throughout the business continued to be pressured by a troublesome backdrop by which declining asset values have challenged the business at giant. With ongoing stress and systemic points dealing with the banking sector, the industrial mortgage sector may even see extra stress within the close to time period. Nonetheless, BXMT is well-equipped to navigate the tough waters with a stellar and well-connected administration workforce.

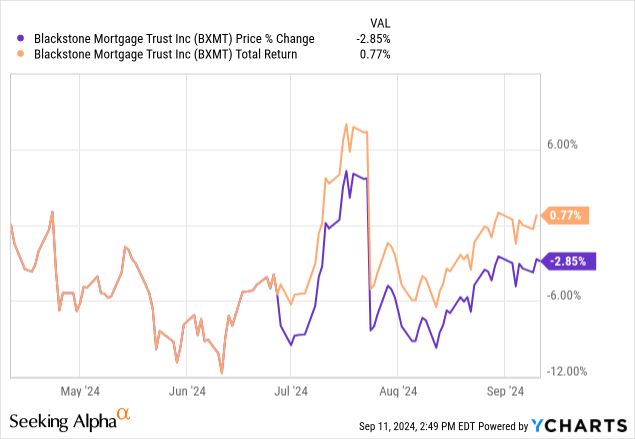

Since publication, issues have unfolded poorly for BXMT. Essentially the most important improvement for BXMT was the dividend minimize from $0.62 per share to $0.47 per share, which was introduced close to the tip of July.

What Went Fallacious?

A key element of our thesis hinged on the unfolding macroeconomic shift that administration, together with BXMT CEO Katie Keenan, recognized as an vital driver for efficiency enhancements. To place it in essentially the most concise phrases, the anticipated enhancements didn’t unfold, together with no modifications to rates of interest and continued deterioration of a number of key sectors of business actual property. Let’s discover these items additional.

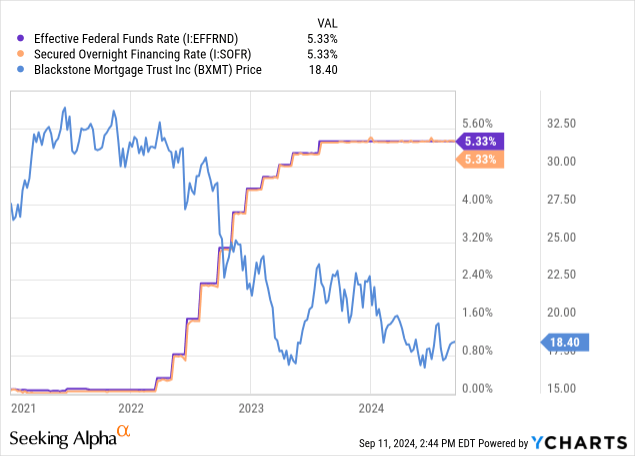

At first, rates of interest are a essential piece of the true property market. They’re of the utmost significance for a floating fee lender like BXMT the place rates of interest have an effect on curiosity revenue on present loans, the flexibility to finance new capital, and the underlying circumstances of the true property market. Every bit of their enterprise is uniquely impacted by actions in rates of interest. On the This fall earnings name, Keenan recognized rates of interest as a key piece of the outlook.

…are encumbered each by loans on price restoration and extra liquidity, earnings energy we are able to recapture over time. And whereas fee cuts have an effect on curiosity revenue for a floating fee lender, additionally they present a extra constructive atmosphere to deploy capital and resolve challenged credit.

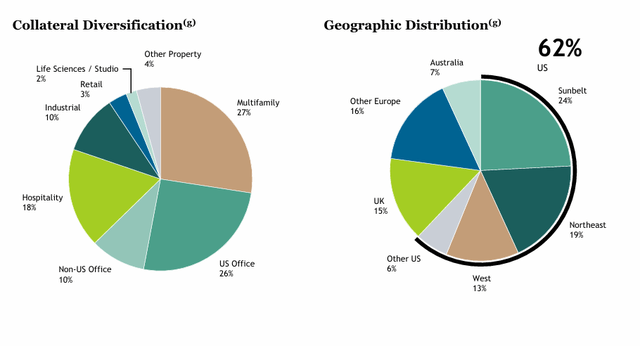

She notes that decrease rates of interest have a push-pull impact on mREITs. Whereas curiosity revenue from floating fee loans falls, the underlying actual property market tends to warmth up. This implies deal stage money circulation weakens, however BXMT’s alternative set widens significantly because the market turns into extra aggressive. For BXMT, rate of interest cuts have been a essential piece of the puzzle. With nearly all of BXMT’s property invested in closely impacted sectors together with workplace (36%), multifamily (27%), and hospitality (18%), the REIT was dealing with a ticking time bomb for asset stage points.

BXMT Web site

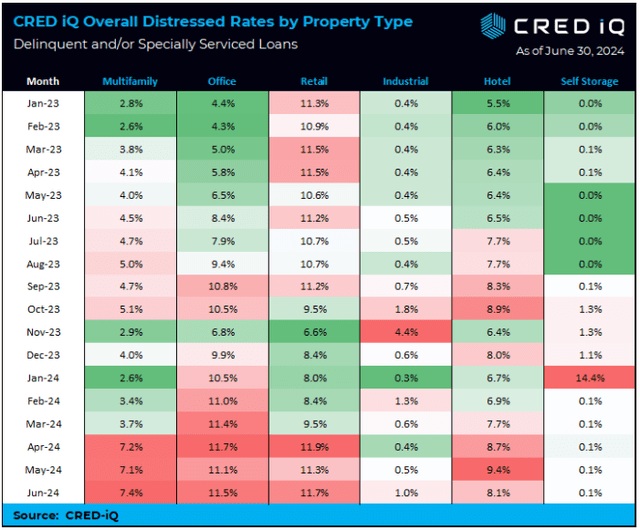

CRED-iQ gives ongoing information round default charges for industrial loans. These are corresponding to the loans that will be held by an mREIT like BXMT, offering a proxy for the well being of particular person asset lessons. In response to their analysis, workplace, hospitality, and multifamily are among the most closely distressed sectors as illustrated under.

CRED-iQ

BXMT reported Q2 earnings close to the tip of July, which included an replace on a number of key areas of the portfolio. Essentially the most important piece of the dialogue was across the ongoing impairment of workplace property, which proceed to impression distributable earnings. Administration famous important progress, reaching “a 90% performing portfolio” and the improve of 9 loans over the earlier quarter. This looks as if excellent news as ongoing points are resolved. Nonetheless, BXMT is hardly out of hassle.

Within the analysis of ongoing points, BXMT’s board elected to chop the dividend to $0.47 per share, a discount of practically 25%. This was mentioned on the Q2 earnings name.

With this in thoughts, our Board has declared a 3rd quarter dividend of $0.47 per share, which we consider displays a sustainable stage relative to long-term earnings energy. Whereas we’re prone to have quarters the place distributable earnings fluctuate from this stage, relying on the timing of asset impairments and determination, we additionally see many upside eventualities over time.

The acknowledgement that ongoing impairments proceed to negatively impression distributable earnings is a degree of concern for BXMT. Following the stabilization of rates of interest, the workplace market has not meaningfully improved as fundamentals stay weak, reminiscent of report emptiness. For reference, the nationwide emptiness fee for the workplace reached 18.1%, a rise over the prior 12 months. The board acknowledging that volatility lies forward is a regarding improvement within the face of virtually sure rate of interest cuts. Actually, the speed outlook was far murkier in earlier quarters when BXMT was buzzing a considerably extra optimistic tune. The workplace has acquired a lot of the consideration for BXMT’s troubles, together with dialogue round present and anticipated impairments.

This is sensible given multiple third of BXMT’s portfolio is workplace property. It overlooks the regarding improve in impairments for multifamily property, which account for greater than 25% of BXMT’s portfolio. Because it stands at the moment, BXMT’s impairments have been largely focused on underperforming workplace property, however there’s hassle brewing in multifamily.

Multifamily Issues Are Rising

Criticizing multifamily property is a troublesome gambit. Traditionally, residences have been one of the crucial profitable asset lessons resulting from rising demand from a number of sources. First, the unaffordability of housing has pushed extra demand in the direction of multifamily residing. Second, inhabitants development round dense city areas continues to push improvement of recent property and redevelopment of present property so as to add density. Lastly, individuals merely want a spot to stay and accordingly, residences are inclined to have few aggressive threats.

Nonetheless, these tailwinds have been all too apparent to traders within the post-pandemic period. The thesis laid out above hit the desk of funding committees far and broad, with the approval stamp hitting most alternatives. This has led to a rare, generational improve in provide in key markets throughout america.

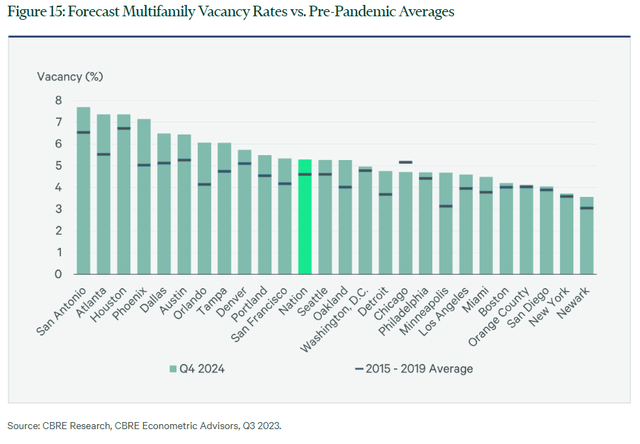

CBRE (CBRE) lately revealed their 2024 Market Report for multifamily actual property, which included a number of essential information items. First, there are practically a million items underneath development throughout america, inflicting 17 of the surveyed markets to extend their stock by greater than 7%.

The largest wave of recent residence provide in a long time will mood lease development and enhance affordability for renters in 2024. With supply of 440,000 new items anticipated in 2024 and greater than 900,000 at present underneath development, the general emptiness fee is predicted to rise and lease development to decelerate.

Of the 69 markets tracked by CBRE, 17 are poised to develop their inventories by greater than 7% in 2024 and 2025. Development completions have already peaked in a number of markets, together with Chicago, Washington, D.C. and Las Vegas. Completions will peak in most different markets in 2024. We count on weaker common lease development of 1.2% in 2024. Provide headwinds restricted latest report lease development to simply 0.7% year-over-year in Q3 2023.

The market has been onerous at work absorbing these items, particularly in rising cities like Austin, TX. Nonetheless, the large wave of provide is inflicting emptiness charges to rise.

CBRE

The rise in emptiness will possible be concentrated in underperforming geographies the place development projections fail to man out. For instance, among the most hotly anticipated markets all through the Sunbelt are experiencing essentially the most important emptiness will increase, reminiscent of Atlanta and Dallas.

This can be a essential concern for BXMT, the place rising emptiness may trigger asset stage issues resulting from aggressive underwriting. Given multifamily accounts for greater than 1 / 4 of the REITs collateral, this could compound on the present workplace points. The forecast of rising emptiness coincides with the numerous improve in misery charges within the three months main as much as June 2024.

Investor Takeaways

Whereas workplace property proceed to obtain a lot of the consideration from BXMT traders, there’s one other downside hiding within the woodwork. This is sensible contemplating workplace is the biggest portion of BXMT’s collateral pool, however it misses a key piece of the equation. BXMT is taking a look at ongoing points as a barometer for the long run, whereas presumably downplaying the emergent dangers in different asset lessons.

Workplace actual property continues to undergo with nearly no finish in sight because the market continues to shift away from pre-pandemic preferences. Nonetheless, this development has been working for greater than 4 years and seems to be everlasting. In distinction, points with multifamily are persevering with to emerge extra lately. As a whole lot of hundreds of items proceed to return on-line this 12 months, the biggest markets are struggling to soak up the brand new provide. This results in rising emptiness and declining market lease, each of which negatively impression asset stage efficiency. Merely, BXMT has no room for error in the case of including extra issues to their portfolio.

As dangers proceed to emerge and the basics behind industrial actual property deteriorate, BXMT earns a Promote ranking.

{kind=link}