JHVEPhoto

Funding thesis

Celestica (NYSE:CLS) is In search of Alpha Quant’s top-rated inventory in the mean time. Certainly, the inventory has been on fireplace this yr, with the value greater than doubling year-to-date. This was as a consequence of constantly excessive YoY income progress within the final six quarters, which is uncommon for the corporate. However for the long-term, earnings and free money movement matter probably the most. And the corporate has large industry-inherent constraints to increase its profitability metrics. Working in a extremely aggressive atmosphere forces to be aggressive in pricing, which retains margins razor-thin even in periods of notable income enlargement. It’s also essential to say that income progress is anticipated by consensus to return again to regular within the upcoming quarter. The valuation doesn’t look enticing after an enormous rally both. All in all, I assign the inventory a “Maintain” ranking.

Firm info

Celestica is a Canadian firm that delivers modern provide chain options globally to prospects in two segments: Superior Expertise Options [ATS] and Connectivity & Cloud Options [CCS]. Celestica’s choices in each segments embody design and improvement, new product introduction, engineering companies, element sourcing, electronics manufacturing and meeting, testing, complicated mechanical meeting, programs integration, precision machining, order success, logistics, asset administration, product licensing, and after-market restore and return companies.

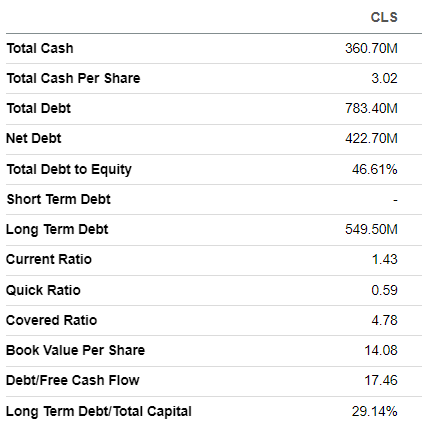

Celestica’s newest annual SEC submitting

The corporate’s fiscal yr ends on December 31. Based on Celestica’s newest annual SEC submitting, the corporate generated 66% of its FY2022 gross sales from the highest ten prospects.

Financials

The corporate’s monetary efficiency over the past decade appears to be like nothing particular. The income progress charge hardly outpaced the long-term common inflation charge with a 2.5% CAGR. The gross margin by no means climbed above single digits over the past decade, and the working margin is razor-thin. The common free money movement [FCF] margin ex-stock-based compensation [ex-SBC] is 1.2%, virtually nothing.

Writer’s calculations

Razor-thin margins imply the corporate has little room to reinvest in innovation and enterprise enlargement. Low profitability metrics additionally don’t permit Celestica to maintain shareholders proud of dividend payouts or substantial inventory buybacks. The common monetary energy additionally doesn’t shock me as a consequence of low margins.

In search of Alpha

However, the income dynamics ranging from Q1 FY2022 have been spectacular, with YoY progress constantly at double digits. The most recent quarter’s earnings have been launched on July 26, and the corporate topped consensus estimates. Income grew virtually 13% YoY, and the adjusted EPS expanded from $0.44 to $0.55.

In search of Alpha

Regardless of large progress momentum over current quarters, profitability metrics stay low. In Q2 FY 2023, the gross margin was nonetheless beneath 10%, and the working margin was beneath 5%. Quarterly income elevated by about 37% in comparison with Q2 of FY 2021, however margin enlargement was comparatively insignificant. This clearly signifies to me that the economies of scale impact may be very insignificant for the corporate, and income progress doesn’t add a lot worth to shareholders.

In search of Alpha

The upcoming quarter’s earnings launch is scheduled for October 26. Quarterly income is anticipated by consensus at $2 billion, which signifies a 4% YoY progress. The adjusted EPS is anticipated to increase YoY from $0.52 to $0.60. Income progress deceleration means that stable momentum is cooling down, and the tempo steadily returns again to the long-term trajectory.

In search of Alpha

The administration underlines that the corporate operates in a extremely aggressive atmosphere in its annual SEC filings. If we have a look at the profitability metrics of the corporate’s rivals, we will see that each one of them are low. That stated, the {industry}’s pricing competitors may be very intense, that means CLS has tiny room for profitability metrics enlargement. As we will see beneath, CLS leads concerning the levered FCF margin however principally lags in different profitability metrics. That stated, I don’t see any rivals having sturdy long-term aggressive benefits.

In search of Alpha

Valuation

The inventory greater than doubled in 2023 with a 106% year-to-date rally, considerably outperforming the broader U.S. market. In search of Alpha Quant assigns the inventory with a excessive “A-” valuation grade since its multiples are considerably decrease than the sector median throughout the board. On the identical time, present valuation ratios are considerably increased than the corporate’s historic averages.

In search of Alpha

The outcomes of a number of analyses are combined, so I want one other valuation strategy to run. Celestica doesn’t pay dividends, so the discounted money movement [DCF] simulation appears to be like like the one viable choice to proceed with. I take advantage of a ten% WACC for discounting. A 1.7% FCF margin is the final five-year common, which appears to be like truthful for the DCF. Consensus income estimates can be found just for the 2 upcoming years. For the years past, I incorporate a modest 2% income progress.

Writer’s calculations

Based on my DCF simulation, the enterprise’s truthful worth is $3.2 billion, which may be very near the present market cap. The upside potential is 5%, that means that the goal worth for the inventory is $24.5. Given all of the dangers and uncertainties I focus on beneath, I think about the upside potential unattractive.

Dangers to think about

I think about the corporate’s low profitability metrics a major shareholder threat. The 1-2% FCF margin signifies that even slight will increase in commodity costs and labor prices would possibly flip free money movement adverse. Slim profitability metrics over the long run counsel the corporate has virtually no pricing energy to share rising prices with prospects. That stated, there is just one strategy to improve earnings in absolute phrases: by increasing the enterprise scale. However the aggressive panorama may be very intense, and it will likely be robust to develop quickly.

Excessive income focus, which leads to 66% of gross sales generated from top-ten prospects, additionally doesn’t strengthen the corporate’s place in negotiating favorable phrases and circumstances. Focus threat additionally consists of excessive dependence on Celestica’s operations and earnings on the monetary well being of its largest prospects, which might reduce orders throughout difficult instances.

The corporate trades internationally with notable overseas gross sales, that means it faces substantial dangers of overseas alternate volatility. Unfavorable swings in forex alternate charges would possibly adversely have an effect on the corporate’s earnings. Buying and selling internationally additionally means excessive regulatory and geopolitical dangers.

Backside line

To conclude, Celestica’s inventory is a “Maintain”. The corporate operates in a extremely aggressive atmosphere, which makes profitability metrics very low as a result of competitors’s aggressive pricing. Even after an enormous income progress momentum within the final six consecutive quarters, the gross margin by no means climbed to double digits. It’s also essential to notice that the income progress momentum is cooling down because the upcoming quarter’s income consensus estimates forecast YoY progress returning nearer to regular. The valuation additionally doesn’t look very enticing after an enormous year-to-date rally with a mere 5% upside potential.

{kind=link}