Photographs By Tang Ming Tung

The Client Worth Index (CPI) Report was revealed on September 11, 2024, at 8:30 AM. The report comprises details about modifications within the costs (inflation/deflation) of a wide selection of products and companies bought by shoppers within the US through the month of August 2024.

On this article, we’ll stroll readers by an in depth breakdown of the CPI Report. We can even focus on the possible implications of the report for bond and fairness markets.

Based on the BLS, All Objects MoM CPI in August modified 0.19% — shocking barely to the draw back in comparison with the median forecast {of professional} economists, who anticipated 0.20%. Whereas Core MoM CPI modified by 0.28% — shocking to the upside in comparison with the median forecast {of professional} economists which anticipated 0.20%.

The forecasted 3-month annualized all gadgets inflation charge was 1.20% progress charge, nonetheless, reported knowledge point out a 3-month annualized charge of 1.15%, a charge of change which ranks within the thirty seventh percentile traditionally.

The forecasted 3-month annualized core inflation charge was 1.73% progress charge, nonetheless, reported knowledge point out a 3-month annualized charge of two.06%, a charge of change which ranks within the fifty fifth percentile traditionally.

The query now could be: Primarily based on an intensive evaluation of the patron inflation knowledge, and the preliminary market reactions to it, ought to traders make any changes to their financial forecasts, and/or to their funding methods?

The correct reply is rarely an apparent one. On this article, we’ll stroll readers by a four-step course of. First, we’ll carry out a complete evaluation of the just-released report. Second, we’ll replace macroeconomic forecasts, based mostly on this evaluation. Third, we’ll modify our funding assessments of main asset lessons. Lastly, we’ll ship actionable insights that can allow readers to capitalize on our evaluation.

Headline Knowledge and Evaluation

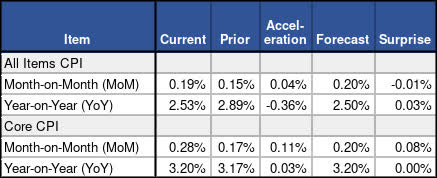

A abstract of key knowledge and evaluation for this month’s CPI Report is supplied in Determine 1.

Determine 1: Change, Acceleration, Expectations, and Shock

Core & All Objects CPI (BLS & Investor Acumen)

All Objects CPI grew by +0.19% in August 2024, which ranks within the thirty seventh percentile traditionally. This variation represented a +0.04% acceleration from the prior month and was a modest upside shock relative to expectations.

Core CPI grew by +0.28% in August 2024, which ranks within the fifty fifth percentile. This variation represented a +0.12% acceleration from the prior month and a average upside shock.

A Deep Dive Into the CPI Inflation Report

This part of our report shall be dedicated to evaluation of information derived from the CPI Report. The primary part tracks the charges of change of CPI annualized inflation over a number of time frames, damaged down by class. The second part presents a decomposition evaluation of the contributions of varied classes to the general MoM change and acceleration of CPI.

Charges of Change and Momentum of CPI Elements

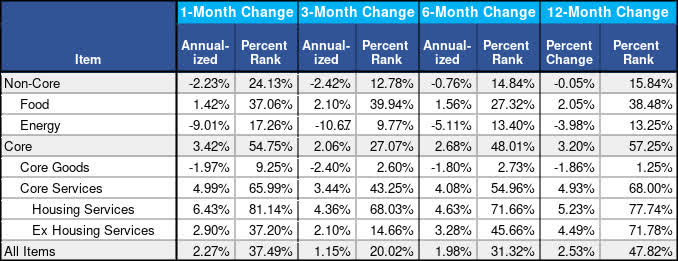

Determine 2: % Change, Annualized Change and % Rank: 1, 3 and 12 months

Annualized Inflation Over the Previous 12 Months (BLS & Investor Acumen)

Power and momentum of general progress. As will be seen in Determine 3, on a 3-month annualized foundation Core Providers Ex Housing (2.10%), the determine most watched by the Fed, was considerably under the historic median (fifteenth percentile).

Divergences in charges of change between classes. It’s attention-grabbing to notice the variations within the 3-month charge of change between Core Items and Core Providers. In Core Items, the 3-month annualized progress charge of CPI (-2.40%) was traditionally under (3 percentile). The annualized progress charge (3.44%) in Authorities payrolls through the previous 3-month interval was traditionally under (43 percentile).

Attribution Evaluation: Change and Acceleration of CPI Elements

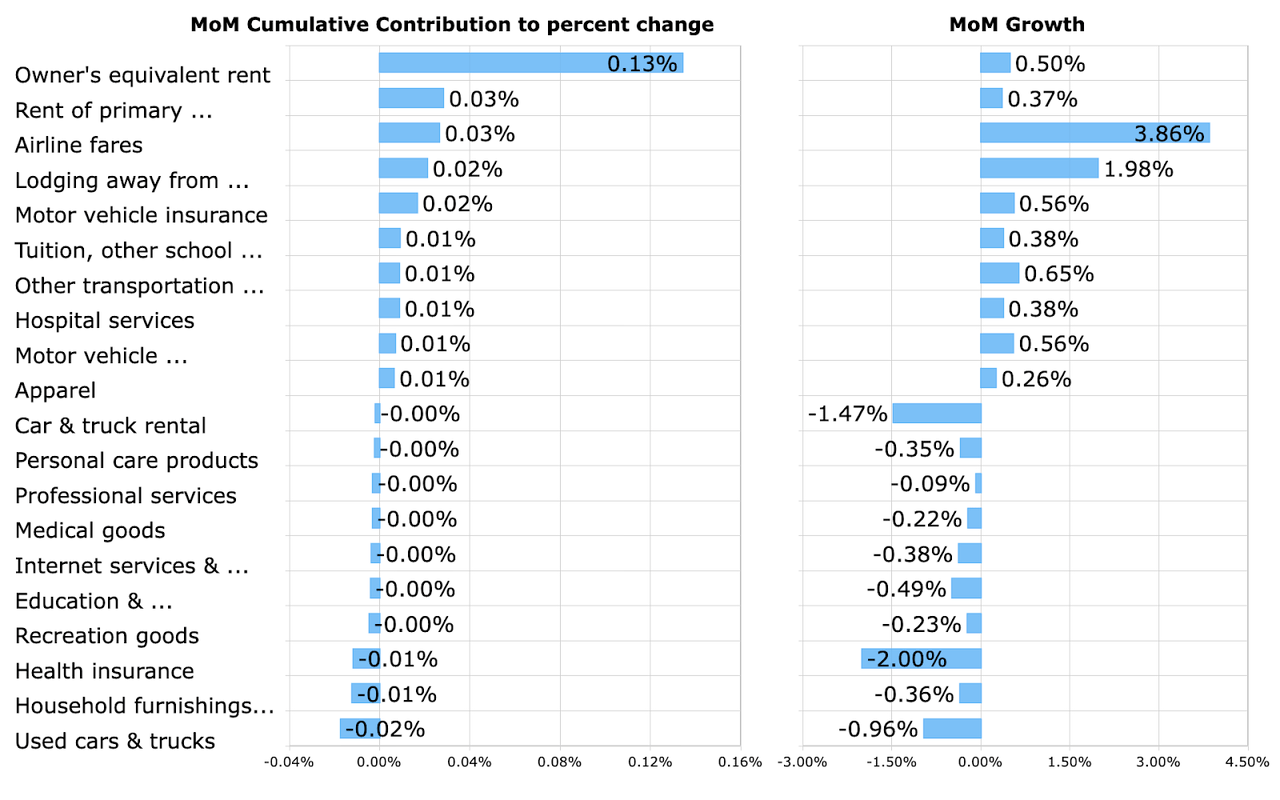

In Determine 3, we carry out a decomposition evaluation of change and acceleration, breaking CPI down into Non-Core and Core parts. We additional decompose the expansion of Non-Core CPI into two subcomponents and decompose the expansion of Core CPI into three subcomponents. Though all 5 columns within the desk present essential info, we suggest that readers pay particular consideration to the rightmost column (Cumulative Contribution to Acceleration). It reveals precisely what drove the month over month, or MoM, acceleration/deceleration in CPI through the present month in comparison with the prior month.

Determine 3: Evaluation of Key Mixture Elements

Mixture CPI Part Evaluation (BLS & Investor Acumen)

As will be seen in Determine 4, the MoM charge of change in All Objects CPI on this previous month (0.19%) skilled a 1-Month p.c change acceleration of +0.03% in comparison with the prior month (0.15%). This modest enhance is attributable to a +0.09% acceleration contribution from Core CPI, partially offset by a -0.06% deceleration contribution from Non-Core CPI.

Inside Core CPI, Core Items accounted for +0.03% contribution to acceleration, whereas Core Providers accounted for a extra substantial +0.06%. The Core CPI acceleration was notable, with Core Providers exhibiting a comparatively sturdy enhance from 0.31% to 0.41%. Nevertheless, Non-Core CPI skilled a major deceleration, notably within the Power part, which noticed a pointy decline from 0.03% to -0.78%.

Contributions to Month-to-month Change in Core CPI

In Determine 4, we dig deeper down into the info and current a bar chart that highlights notable constructive and damaging contributors to the MoM p.c change in Core CPI. These contributions take into account each the magnitude of the MoM change in every part and the burden of every part in CPI.

Determine 4: High Contributors to MoM % Change

High CPI Contributors (BLS & Investor Acumen)

Proprietor’s Equal Hire was an important constructive contributor to the month-to-month change in CPI. The lease of the first residence additionally contributed positively to the month-to-month change in CPI.

It’s crucial to concentrate on the truth that housing parts have the most important weight within the CPI (accounting for about 40% of core CPI). We anticipate that there shall be vital disinflation within the housing parts of CPI for the remainder of 2024 and far of 2025. This may be predicted with near-certainty as a result of roughly 12-18 month lag between real-time housing knowledge and the BLS’s CPI housing knowledge.

Because of the disinflation in housing gadgets, we anticipate that there’ll usually be downward strain on each All-Objects and Core CPI for the rest of 2024 and far of 2025. Nevertheless, it needs to be famous that declines in CPI which might be pushed by these severely lagged parts are usually not notably related for understanding what’s presently happening within the housing markets or within the economic system.

Because of the severely lagged nature of the housing CPI knowledge, readers ought to pay comparatively extra consideration to pricing tendencies in core companies ex-housing, in addition to core items.

Contributions to Month-to-month Acceleration in Core CPI

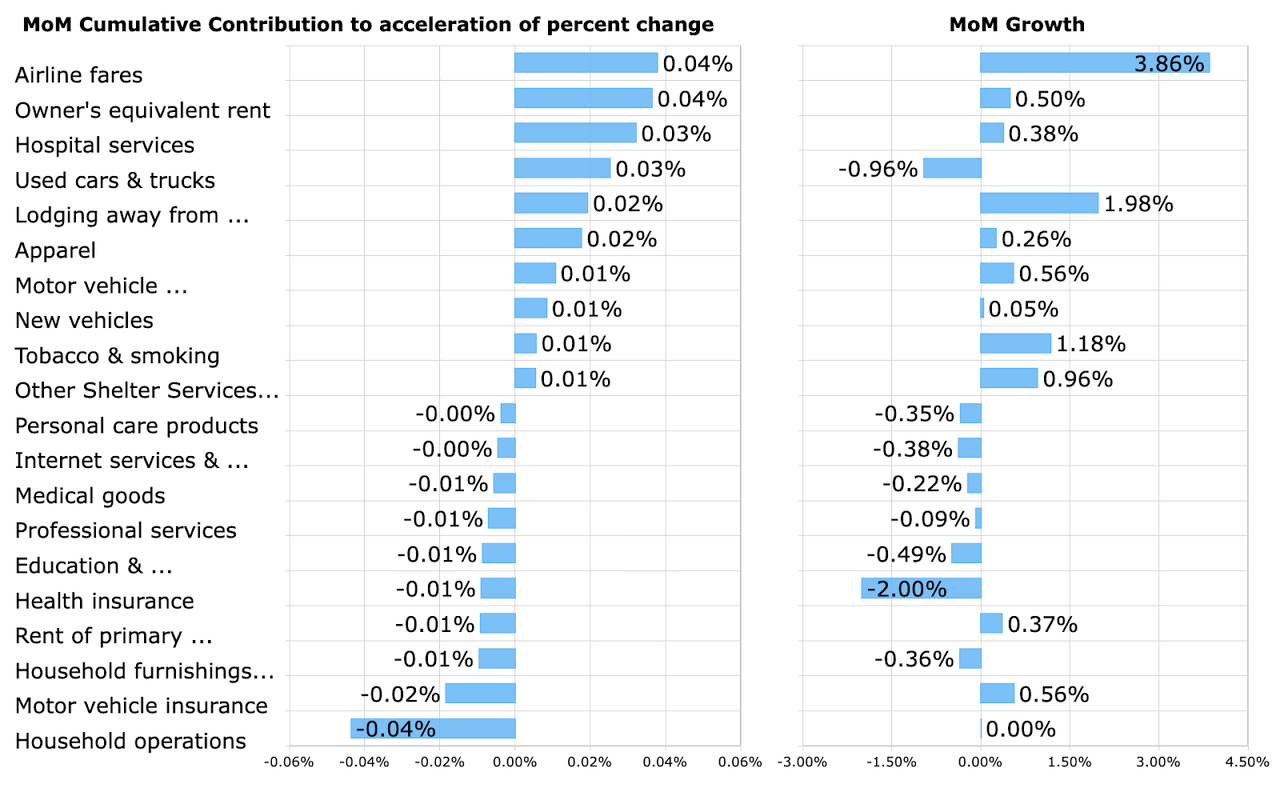

In Determine 5, we shift the main focus from a decomposition of the speed of change to a decomposition of the speed of acceleration. The bar chart highlights notable constructive and damaging contributors to the MoM acceleration in Core CPI. These contributions take into account each the magnitude of the MoM accelerations within the parts and the burden of every part in CPI.

Determine 5: High Contributors to MoM Acceleration of Core CPI

High CPI Acceleration Contributors (BLS & Investor Acumen)

We suggest that readers look at this desk rigorously, as it’s prone to embrace most or the entire gadgets that prompted deviations from forecasters’ expectations of Core CPI.

Amongst gadgets that contributed to the acceleration of Core CPI, Airline fares (+0.04%) and Proprietor’s equal lease (+0.04%) have been the most important contributors.

Amongst gadgets that contributed to the deceleration of CPI, Family operations (-0.04%) and Motorized vehicle insurance coverage (-0.02%) stood out as the most important contributors.

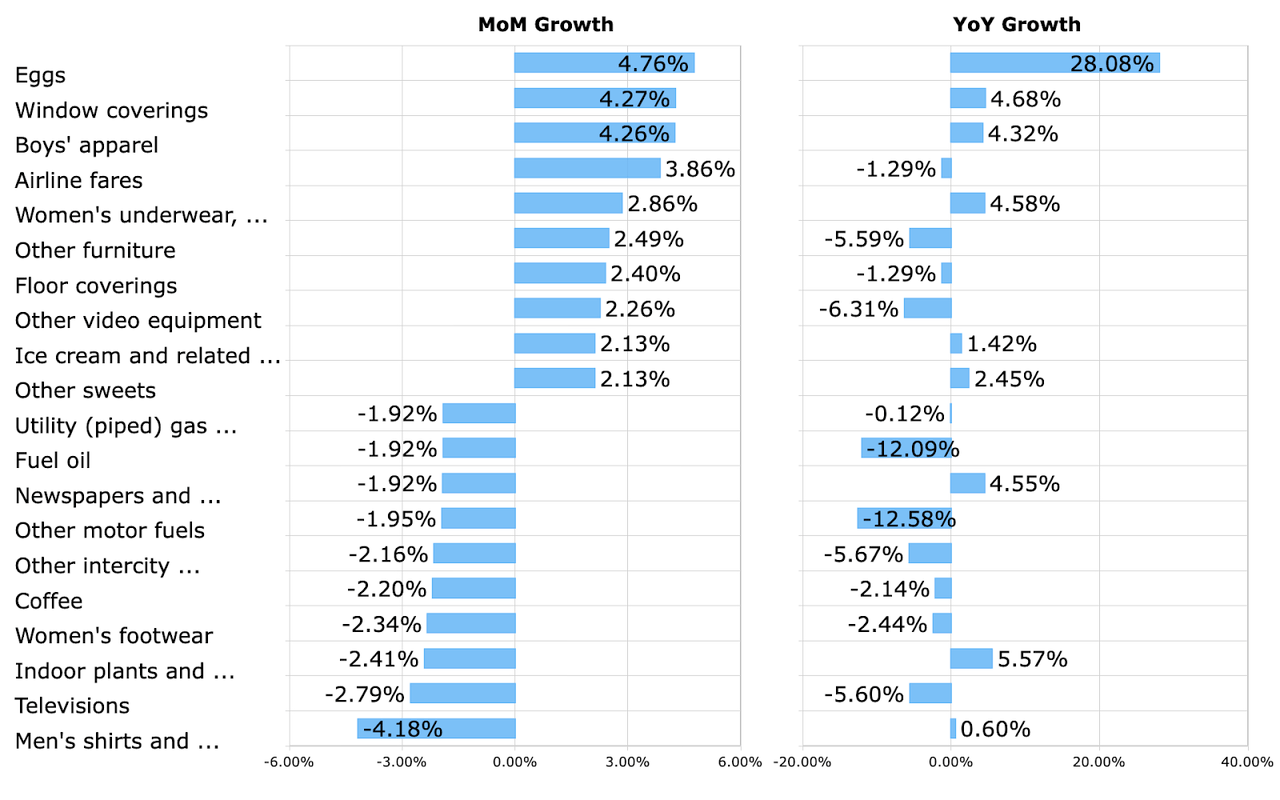

High Movers

In Determine 6, for normal curiosity functions, we spotlight a number of CPI parts (out of over 200) that exhibited the most important constructive and damaging change through the month. The YoY change in these explicit parts is exhibited to the fitting.

Determine 6: High Movers MoM % Change

High CPI Movers (BLS & Investor Acumen)

Eggs (+4.76%), Window coverings (4.27%), and Boys’ attire (+4.26%) have been notable high-inflation gadgets this month. On the reverse excessive, Males’s shirts and sweaters (-4.18%), Televisions (-2.79%), and Indoor crops and flowers (-2.41%) have been massive price-decliners.

Implications for the Financial system

This CPI report was roughly consistent with expectations, with a minor upside shock on Core CPI. Nevertheless, many market contributors have been hoping for a draw back shock which might encourage the Fed to chop charges by 50 foundation factors, moderately than 25 foundation factors, at its subsequent assembly. These hopes have been upset.

In our view, 50 foundation level fed rank was all the time an unlikely consequence. This newest CPI report ought to strengthen market expectations of a 25 foundation level Fed charge reduce.

From an financial standpoint, the Fed’s coverage motion in September is much much less essential than the long-term path of anticipated charge cuts. At present, the mounted revenue markets are pricing in a really aggressive path of charge cuts between now and the top of 2025. In impact, this anticipated path of charge cuts, has created a major market-induced easing of economic situations within the economic system.

Implications for Monetary Markets

The ten-12 months Treasury yield rose barely after the report. The S&P 500 index initially fell after the report, however has rallied again to the unchanged degree.

Whereas core CPI was barely above expectations, this report is usually supportive of the expectation that US worth inflation is headed down sustainably in direction of the Fed’s 2.0% goal. Within the absence of an exogenous shock, equivalent to a serious enhance in oil costs, there’s a good purpose to anticipate that inflation will, in reality, proceed to say no towards the Fed’s 2.0% goal.

Total, this report confirms disinflationary tendencies that shall be supportive of each bond and fairness costs going ahead. Particularly, actual yields, as indicated by TIPS yields, are nonetheless comparatively excessive, and there’s vital room for actual yields to fall, if inflation continues on its downward path. Actual yields can even are likely to fall if expectations for US financial progress charges settle at a below-average tempo. This may be bullish for TIPS and could be supportive of each the mounted revenue and fairness markets.

Conclusion

Though the present path of inflation is bullish, it’s our view that the US economic system is susceptible to an oil worth shock this 12 months, as detailed on this In search of Alpha weblog put up. A serious rise in oil costs can dramatically change the inflation outlook, the financial outlook, and the outlook for inventory and bond markets. As such, we’re positioned considerably cautiously, with sturdy allocations to the power sector.

{kind=link}