Calvin Sienatra

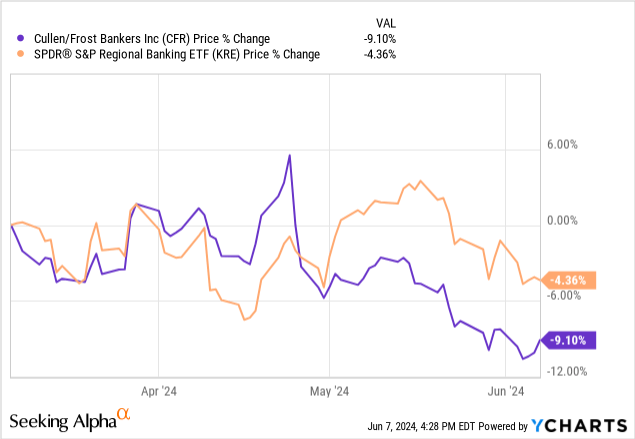

Over the previous three months, the inventory value of Texas regional financial institution Cullen/Frost Bankers (CFR) has underperformed even the poorly performing SPDR S&P Regional Banking ETF (KRE):

And but, CFR just isn’t cheaper than the regional financial institution common. The other is true.

In comparison with a median value to e-book worth of 0.94x for KRE’s holdings, CFR trades at a a lot increased value to e-book worth of 1.85x.

Furthermore, whereas KRE’s common P/E ratio sits at 10.3x, CFR’s P/E ratio is 11.9x.

Lastly, KRE’s index dividend yield stands at 3.7%, in comparison with CFR’s dividend yield of three.65%, in order that they’re mainly the identical.

Does CFR deserve this barely premium valuation over the regional financial institution index?

I might argue that CFR greater than deserves it. The truth is, I imagine that even at a slight premium, CFR’s long-term strengths are undervalued at a inventory value of round $100 and an earnings a number of a bit beneath 12x.

CFR has about 20% upside to its 5-year common valuation of about 14.5x earnings, which mixed with mid- to high-single-digit earnings development and a dividend yield of three.6% ought to generate double-digit whole returns going ahead.

For fellow dividend development traders, CFR appears to be like significantly interesting, as CFR has elevated its dividend for 30 consecutive years, averaging about 7% yearly over the previous 5 years, and it has a snug payout ratio of about 40%. I might count on a comparatively minimal dividend hike this yr however a return to mid- to high-single-digit development thereafter.

Frost Financial institution’s Underappreciated Strengths

Let’s get a snapshot of a few of the strengths I feel the market is undervaluing in CFR proper now:

The financial institution boasts robust and rising market share within the largest cities of the robust and rising state of Texas. CFR is well-capitalized with capital ratios nicely in extra of minimal required quantities. CFR is a first-rate instance of monetary conservatism with little or no debt, 17.5% of property in money, and a loan-to-deposit ratio of 0.47x. Two-thirds of the financial institution’s investor-owned workplace loans are Class A and over 90% are backed by properties in Texas, which is having fun with above-average development in office-using jobs. Credit score losses stay extraordinarily minimal. Allowance for credit score losses stood at 1.29% of whole loans in Q1 2024, down from 1.31% in This fall 2023 and 1.32% in Q1 2023. Non-performing loans have been 0.37% of whole loans in Q1 2024, in comparison with 0.32% in This fall 2023 and 0.22% in Q1 2023. Lower than 20% of CFR’s drawback loans are tied to investor-owned industrial actual property.

I might like to focus on three specific factors of power.

The Finest Offense Is A Good Protection

With regards to CFR’s longstanding monetary conservatism, observe that Frost Financial institution was the one giant financial institution to make it by the financial savings & mortgage disaster of the Nineteen Eighties with out requiring federal help or a merger. It was additionally the primary financial institution within the nation to show down TARP funds through the Nice Monetary Disaster of 2008-2009.

The financial institution’s typical coverage is to maintain about 20% of whole property in money, which provides it each a deep cushion and likewise acts as vital dry powder with which to pounce on enticing funding alternatives once they come up.

The financial institution has lately been drawing on that money pile to deploy into high-yielding loans and securities, which ought to serve the financial institution nicely in the long term. Not solely is it capturing some good yield, additionally it is capturing new borrower clients.

New industrial relationships elevated 10% YoY in Q1 2024. At 825 new relationships, it was CFR’s largest variety of quarterly borrower relationship positive aspects in its historical past.

In Q1, the mortgage e-book grew 10.4% YoY even whereas whole deposits declined 4.8%. If CFR didn’t have such a big money place or such a low loan-to-deposit ratio, it might not be capable of seize billions of {dollars} extra of the mortgage market.

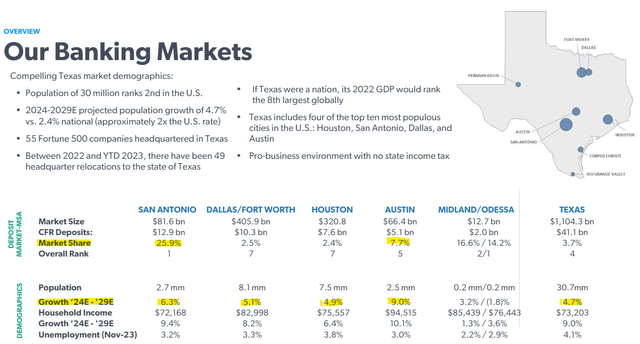

Robust Market Place In Texas

Now, in terms of CFR’s markets, remember that the financial institution’s bodily department areas are solely in Texas, and the overwhelming majority of its depositors and debtors are additionally based mostly in Texas.

The 4 main metro markets of Texas have been rising nicely above the nationwide common, when it comes to inhabitants and jobs, and projections for development over the following 5 years present that speedy development persevering with.

CFR February Presentation

Discover from this picture that Austin and San Antonio are anticipated to benefit from the quickest development in inhabitants and households within the coming years, and these two markets are additionally those whereby CFR has captured the best market share.

The financial institution is opening new department areas within the fast-growing Austin market, which signifies that Frost will possible proceed to develop its share in that market.

This can be a main and underappreciated power. Proper now, deposits are trickling out of Frost Financial institution searching for increased yield elsewhere, however inside a yr or so, the Fed Funds Charge and SOFR are anticipated to be decrease than they’re immediately. If and when that money flows again into banks, Frost needs to be an enormous beneficiary.

Robust development in relationships with each debtors and depositors is an underappreciated power.

Extremely Conservative Mortgage Underwriting

Lastly, I might like to the touch on CFR’s high-quality and conservatively underwritten mortgage e-book, significantly the industrial actual property phase.

Word from the above bullet factors that regardless of being about half of CFR’s whole mortgage e-book, industrial actual property makes up lower than 20% of problematic loans. These are non-performing, partially non-performing, or overdue loans.

Of the very small quantity of non-performance and credit score losses in CFR’s mortgage portfolio, the disproportionate space of weak spot is primarily in industrial & industrial (enterprise) loans adopted by residential mortgages. However even these areas of weak spot are extraordinarily restricted.

Non-performing (or non-accruing) loans made up solely 0.37% of whole loans in Q1 2024.

Now, might CFR’s delinquencies rise from right here? It’s definitely potential. However remember that any losses from delinquent CRE loans is more likely to be fairly restricted.

Contemplate, for instance, that investor-owned CRE at the moment has a median loan-to-value of 53%. For investor-owned workplace, particularly, the common LTV additionally stands at 53%. Nonetheless, investor-owned workplace loans even have a barely increased debt service protection ratio of 1.53x than the CRE phase as a complete’s 1.47x.

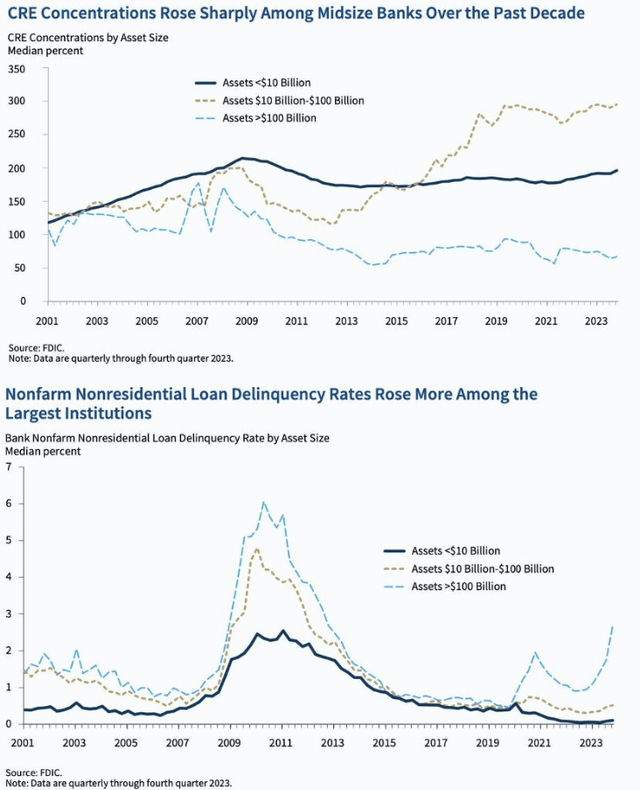

Additionally remember knowledge lately reported by CoStar that it’s truly giant banks ($100 billion+ property) which are experiencing increased delinquency charges from CRE loans proper now.

FDIC

As you may see from the charts above, whereas midsized banks like CFR vastly elevated their publicity to CRE loans over the previous decade, their CRE delinquency charges have remained fairly muted through the present rate-hiking cycle.

In the meantime, although massive banks have lowered their publicity to CRE, these CRE loans they do have are seeing a giant surge in delinquencies.

My proposed clarification for that is that small and midsized banks (regional banks) are extra aware of their markets and keep relationships with the locals. Massive banks are sometimes considerably faceless and committee-driven, making an attempt to make up for his or her lack of face-to-face relationships with extra documentation.

However good quaint relationships and good underwriting trump stricter documentation when the stuff hits the fan.

Even at almost $50 billion in whole property, CFR does a terrific job of working like a small, native financial institution, exemplified by its host of “finest financial institution” awards.

Backside Line

It appears as if any financial institution with substantial industrial actual property publicity is promoting off proper now, CFR included.

I feel this represents a terrific shopping for alternative for long-term traders, particularly dividend development traders corresponding to myself.

Whereas there was a modest deposit outflow during the last yr or so, CFR seems to be in no hazard of a “run on the financial institution” situation. It’s gaining clients, and people clients are usually fairly loyal because of the financial institution’s top-notch customer support.

However on the similar time, no financial institution, together with Frost, can elevate their deposit yields sufficient to maintain up with the 5%-yielding cash markets and high-yield financial savings accounts out there on the market — to not point out 4-5%-yielding Treasuries and CDs. In such a wierd atmosphere as this, it shouldn’t be shocking to see some money go away conventional banks searching for yield.

That does not imply depositors are panicking and pulling out. They’re merely appearing rationally.

When the yield differential between Frost Financial institution and different choices out there isn’t any longer so large, will probably be the rational determination to consolidate your money on the similar financial institution that hosts one’s transactional account. And Frost does a superb job of capturing and protecting these core transactional accounts.

With nice customer support and no legit causes for worry about CFR’s mortgage portfolio, the danger of a “run on the financial institution” situation certainly appears to be like very low.

Quite the opposite, as soon as the yield curve normalizes, I might count on CFR’s whole deposits to develop once more, which might return CFR to its regular, virtuous cycle of development.

{kind=link}