Jaroslaw Kilian/iStock Editorial by way of Getty Pictures

Israel’s flag service, El Al Airways (OTC:ELALF), shouldn’t be your common airline. Not even on a standard day. Its airplanes are outfitted with protection programs, and at some airports, airplanes get further safety measures. With the warfare unfolding, the particular place of El Al as soon as once more turns into clear, as I focus on on this report.

What Are The Dangers And Alternatives For El Al Airways?

When discussing El Al, it makes a variety of sense to start out with an evaluation of the dangers and alternatives, and considerably counterintuitive the present scenario in Israel has resulted in a stronger place for El Al. As some nations have put Israel on the pink listing for journey as a result of security issues, varied airways have additionally suspended flights to the nation. The end result has been that provide has been considerably diminished in extra of demand, and that has led to raised cargo and passenger revenues for El Al. The chance for El Al to that improved monetary atmosphere is that different airways may determine to recommence operations to and from Israel, which may considerably scale back the unit income energy, however in the meanwhile, El Al enjoys elevated revenues.

El Al Earnings Soar 140%

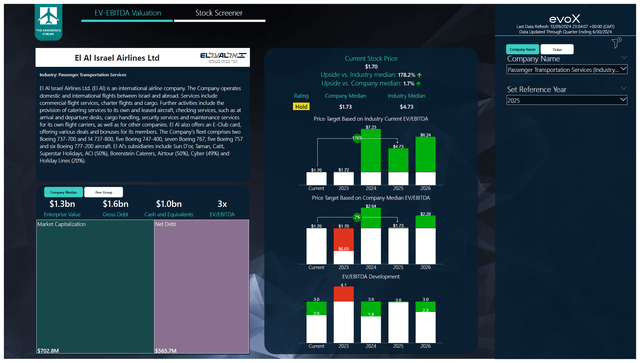

El Al Airways

Revenues elevated from $629.8 million to $839.1 million, indicating a 33.2% soar. This was pushed by a 7.9% improve in passenger capability coupled with a 24.3% improve in unit revenues and 35.8% extra cargo carried. On the similar time, prices solely elevated by 15.4% of which half is pushed by the upper capability deployed and, as we see in different trade, by greater labor prices in addition to greater gas prices. Unit prices excluding gas elevated 9% and together with gas it elevated by 9.5%. So, I’d say on the fee facet of issues are usually not wanting too unhealthy. Particularly, once we understand that the airline is at present working sub-optimally because it faces greater safety prices and has to pinpoint adjustments within the demand panorama and act on that as effectively as potential. Working revenue elevated from $126.1 million to $215.7 million, marking a 140.7% improve in earnings and margin enlargement from 14.2% to 25.7%.

So, what we’re left with is a powerful income atmosphere and a price atmosphere that’s at elevated ranges as a result of greater prices seen all through the trade in addition to further prices the corporate has in relation to the warfare.

Is El Al Airways Inventory A Purchase?

The Aerospace Discussion board

To find out multi-year worth targets The Aerospace Discussion board has developed a inventory screener which makes use of a mix of analyst consensus on EBITDA, money flows and the latest stability sheet information. Every quarter, we revisit these assumptions, and the inventory worth targets accordingly. In a separate weblog I’ve detailed our evaluation methodology.

El Al is doubtless essentially the most troublesome airline I’ve coated because of the present scenario in Israel. It’s not a lot the case that the warfare pressures the outcomes. The truth is, from what we’re seeing now, the impression is optimistic. The massive query is how lengthy that may final. I’ve at present modelled that optimistic impression for the rest of 2024 which reveals that valuing the corporate one 12 months forward of earnings that means towards extra normalized revenue ranges would suggest a maintain ranking. Nevertheless, if the warfare impression continues to impression positively into 2025, then we see the elemental worth of the inventory improve to $3.92 per share, implying 130% upside. That actually is a widespread to the upside case for El Al, and it’s one which I don’t really feel notably snug with. There both appears to be little to no upside or main upside.

Conclusion: El Al Airways Is Solely A Purchase On Continuation Of The Conflict

The funding case for El Al Airways is advanced. The corporate counterintuitively is performing higher throughout wartimes regardless of greater prices, and that’s as a result of different corporations have eliminated capability within the passenger in addition to air freight market, leaving El Al Airways as one of many few airways flying by means of and from Israel. The plain threat is that because the risk degree normalizes, airways will begin reconnecting to Israel once more, and that may put stress on El Al’s present sturdy unit revenues. If the warfare is to proceed properly into 2025, we may see one other 12 months of above-normal outcomes, which ought to drive the corporate’s inventory worth. At the moment, the uncertainty concerning the place issues might be heading doesn’t make me snug to place a purchase ranking on the inventory.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}