Alones Artistic

Introduction

The tech-heavy market has bounced again sharply final week. Since August 9, the Invesco QQQ Belief ETF has jumped up about 9.2%. The VIX might need peaked at over 65 at one level on August 5. That is the best stage that VIX has reached for the reason that peak of the COVID-19 pandemic. The cooling down VIX could sign a short-term backside for the main market indices. Buyers could need to look into progress shares with sharp pullbacks to date in August and choose up good corporations for the remaining a part of 2024 and past.

Then again, the reasonably disturbing headlines, akin to SA information’ “Tech layoffs surge, led by mass purges at Intel, Cisco”, preserve reminding expertise traders of the significance of inventory picks.

REX FANG & Innovation Fairness Premium Revenue ETF (NASDAQ:FEPI) is just not the one I’d advocate to purchase due to its technique and portfolio construction, which I’ll focus on intimately later. Gathering revenue from choice premiums is a superb concept, particularly for many who need to dip their toes into the expansion however risky market areas. Many actively managed ETFs have emerged just lately to make the most of the coated calls. I’ll focus on a few of them along with FEPI to share my insights. There are higher alternate options to contemplate than FEPI for revenue traders.

FEPI ETF Overview

FEPI is an actively managed ETF with the next objective assertion.

FEPI Goal – from rexshares.com

The ETF’s portfolio may be summarized as:

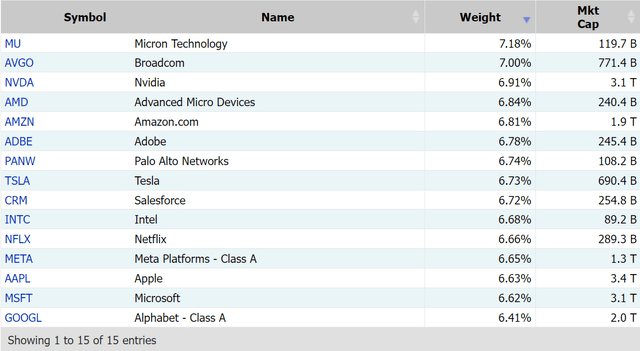

Equally weighted and consists of 15 extremely liquid shares centered on constructing tomorrow’s expertise in the present day.

The next is the present checklist of the 15 holdings within the portfolio:

FEPI Holdings – from marketchameleon.com

It’s truthful to say that the checklist has the largest market caps, which all exceed $100B except for Intel (INTC) (after the current large worth drop), within the expertise area together with “the magnificent 7” (Magazine 7) and semiconductor giants akin to Broadcom (AVGO) and Nvidia (NVDA).

Some key traits of FEPI are listed under:

Market Cap: $346.3M. Inception: October 11, 2023. It’s a new ETF. Extra time is required to validate its technique. Yield: 21.2%. Volatility (WK-52 HV): 17.1. It is extremely excessive for an income-focused ETF. Danger Rating (Morningstar): 91. It’s thought of to be very aggressive.

Why is FEPI’s Portfolio Questionable

After I was requested by my readers in SA to check out FEPI the primary time round, I used to be a bit puzzled by the “Innovation” and “Premium” elements in its title for 2 causes. 1) FEPI is just not Magazine 7 “obese” resulting from its equal weight construction. In different phrases, the opposite holdings can have the identical “innovation” and “premium” standing as Magazine 7 shares. It is perhaps high quality for taking part in the following tier for extra innovation progress. However in actuality, it is extremely tough to search out the proper picks with out market capitalization weighting. 2) the selection of INTC and MU lead me to consider that the administration’s premium selections are very totally different. SA database exhibits that 3-year CAGR metrics for INTC and MU are -10.78% and -5.70%, respectively. They’re the one constituents in FEPI’s portfolio which have proven unfavorable income progress over the previous 3 years.

It isn’t shocking to me to see that FEPI received clobbered in current weeks due largely to about 30% drops in each INTC and MU over the past two months.

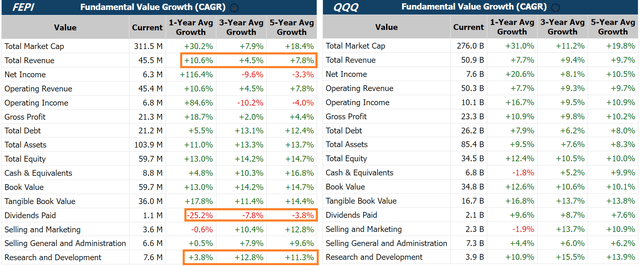

The next progress comparability between FEPI and QQQ will present extra complete insights. The income progress has been considerably slower than QQQ. The 1-year progress is best at 10.6%, which can be largely as a result of cycle from the semiconductor trade, therefore not thought of to be “secular”.

Progress Comparability (FEPI and QQQ) – from marketchameleon.com

Probably the most alarming metric is in Analysis & Growth Progress. FEPI is constantly decrease than QQQ. 3.8% 1-year progress can hardly be known as “innovation” ample, which ought to be in double digits primarily based on the historic knowledge. As mentioned earlier, the 2 major drags on FEPI’s CAGR metrics are INTC and MU.

Clearly, the administration will need to have seen one thing I didn’t see when INTC was chosen as one of many 15 holdings. Nonetheless, with the newest improvement with INTC, one can clearly see that INTC has been struggling for fairly a while.

The next is from Intel’s CEO on August 1 (in the identical SA new, as linked in Introduction part) when saying the large layoff:

Our revenues haven’t grown as anticipated – and we have but to completely profit from highly effective tendencies, like AI. Our prices are too excessive, our margins are too low. We want bolder actions to handle each – significantly given our monetary outcomes and outlook for the second half of 2024, which is harder than beforehand anticipated.

If I simply take a look at what the CEO acknowledged above, INTC inventory ought to be prevented as an innovation progress play proper now. The AI practice has already left the station, it’s going to price far more to do catch-up. Based on the CEO, the prices are already too excessive proper now, and I’d anticipate the prices to be a lot increased sooner or later to develop INTC’s AI competency and seize the AI market shares. I hope that FEPI’s administration can have the identical understanding as mine sooner or later replace of its “innovation” portfolio.

On the portfolio stage, the selection of 15 holdings is sort of a thriller to me. Fifteen is just not seen as assembly the minimal diversification requirement. It doesn’t appear to come back from the “alpha” issues by deciding on the highest 15. The equal-weight construction would solely work if all the alternatives are thought of on the comparable “premium” stage of their corresponding industries. I’ve to confess that I’ve little or no confidence within the portfolio to outperform primarily based on its present innovation and premium properties.

A Few Different Approaches to Take into account

I’ve a usually very optimistic view on the expansion revenue ETFs which use coverall calls to generate revenue. The portfolios may be simply constructed thanks largely to the ultra-popular and profitable ETF QQQ, with round 100 high expertise corporations.

Sometimes, the value efficiency is anticipated to be comparable as a result of identical underlying portfolio. Nonetheless, the strike costs of the call-writing make fairly some distinction as a result of QQQ is a risky ETF. Far out, OTM (out of cash) will protect a lot of the upside appreciation. The nearer to the cash calls will improve the capped quantity for good points. Nonetheless, on the opposite aspect, the draw back results are simply the other. The nearer to the cash, the higher worth safety shall be.

The strategy is seen as conservative if the strike worth is near the cash, whereas the aggressive finish of the spectrum shall be on the far OTM aspect.

QYLD – International X NASDAQ 100 Coated Name ETF. Probably the most conservative. Lowest volatility and lowest efficiency acquire.

International X Nasdaq 100 Coated Name ETF | NASDAQ: QYLD Market Cap: $8.0B Yield: 11.5% Volatility (WK-52 HV): 9.4 Danger Rating (Morningstar): 42

JEPQ – JPMorgan Fairness Premium Revenue ETF

Market Cap: $14.7B Yield: 10.2% Goal Strike: 2.5% Volatility (WK-52 HV): 12.9 Danger Rating (Morningstar): 42

YMAX – YieldMax Universe Fund of Possibility Revenue ETFs. YMAX has injected volatility into the revenue technique.

Market Cap: $270.2M Yield: 44.1%. It’s the highest yield, as a result of volatility focus Volatility (WK-52 HV): 18.7. It’s the most risky, as anticipated Danger Rating (Morningstar): 2. It’s the most conservative. I’ve known as it “new SWAN”

NUSI – Cashing QQQ For Sensible Progress Revenue Rotation. See extra particulars in my earlier article.

Market Cap: $335.1M Yield: 7.5% Volatility (WK-52 HV): 13.7 Danger Rating (Morningstar): 53

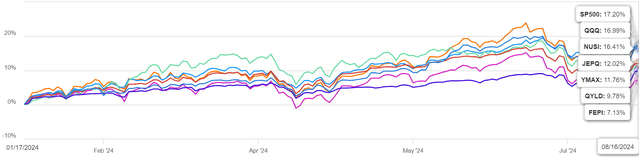

The next exhibits the whole efficiency comparability amongst these ETFs, along with SP500 and QQQ. The time-frame is January 17, 2024 (when YMAX was incepted) to August 16, 2024.

Worth Efficiency Comparability – from SA charting

Discover the above chart is given right here for reference solely, as a result of restricted time length. I’ll present the next insights primarily based on the ETFs’ traits. Readers are welcome to make use of future knowledge or previous knowledge to confirm and draw their very own conclusions for his or her buying and selling choices.

Probably the most danger conservative strategy relies on the promoting of coated calls near the buying and selling worth (or on the cash). The worth efficiency is capped probably the most, so the restricted worth upside is anticipated. An excellent instance right here is QYLD. Probably the most noticeable attribute is the low volatility. The ETFs at this finish of the spectrum are likely to outperform the remainder throughout the down and flattish QQQ market. On the opposite finish of the spectrum, the ETF might promote coated calls or be compensated by shopping for lengthy calls akin to NUSI. The yield shall be smaller, however the worth efficiency will doubtless be higher. The ETFs on this class can have excessive volatility and have a tendency to have worse efficiency throughout the downtrend. Nonetheless, the value restoration will usually be quicker and have higher worth good points. Promoting volatility-based calls is a brand new sort of technique. Over the long term, I consider the whole efficiency would nonetheless be just like the above, relying on the aggressiveness of choosing the strike worth to promote the calls. Nonetheless, within the quick run, the volatility might have a big effect on the value efficiency each when it comes to capping and restoration. In different phrases, quick and risky strikes in both path (up or down) will trigger underperformance in comparison with the underlying portfolios (often known as “worth erosion”). Extremely yield akin to 40% or increased may be typically seen with implied volatility over 50.

FEPI seems to be an “outlier” resulting from its “secretive” portfolio choice. As proven above, it does have the worst market traits within the group, akin to HV and danger rating. Until one thing adjustments drastically, I’d anticipate FEPI to be sitting on the bottom finish on my suggestion checklist. I charge FEPI as a maintain.

Dangers and Caveats

The FEPI portfolio nonetheless has a big portion allotted within the rising shares and a number of the greatest innovation corporations. It’s a high quality set of shares general. Current holders should still discover it snug to carry FEPI shares for the long run. For instance, some should still place confidence in the INTC inventory or FEPI’s administration to exchange INTC with one other “sensible” alternative. The dangers of the administration’s innovation selections ought to be watched intently.

Closing Ideas

ETFs which can be promoting calls have attracted loads of curiosity from revenue traders. These traders ought to be well-informed concerning the technique and constructions of those ETFs earlier than allocating substantial quantities of their cash into the ETFs. FEPI’s premium and innovation “labeled” strategy has not been confirmed but. Its portfolio complete holdings and particular person selections are seen as “unconventional”. They haven’t proven proof to beat the traditional coated name ETFs throughout their quick historical past. Revenue traders shall be higher off in search of different options, together with the bigger and extra common ETFs in that class. I anticipate the yield round 10% to be an inexpensive start line for an investor to get the positioning going within the portfolio. Extreme yields, akin to these exceeding 20% (FEPI and YMAX), sometimes contain complicated (together with proprietary) mechanisms which will deliver administration and/or operational dangers, which require extra administration that can doubtless depend on particular person traders themselves.

{kind=link}