Understanding these frequent obstacles is step one to overcoming them. This information goals to make clear these challenges and provide actionable options that can assist you efficiently qualify for an FHA mortgage in Florida.

Earnings Necessities

Understanding the Earnings Requirement Pitfalls in FHA loans may be intimidating. Our complete method explains them completely, simplifying your journey to residence possession.

By comprehending and proactively dealing with FHA mortgage revenue necessities, you may enhance your approval odds and speed up your path to residence possession.

Proactively addressing income-related challenges within the FHA mortgage approval course of can maximize your possibilities of success, permitting you to safe your dream residence.

Minimal Earnings Threshold

Assembly the minimal revenue threshold for an FHA mortgage could be a hurdle for some. It is the FHA’s means of making certain you may deal with mortgage funds. If this complexity appears daunting, skilled recommendation can assist navigate these tougher waters.

If you happen to’re incomes lower than the FHA mortgage restrict, strategizing to spice up your revenue enhances your mortgage eligibility. Contemplate growing work hours, looking for a higher-paying job, or using facet gigs.

Bear in mind, FHA loans do not implement a minimal revenue requirement; as an alternative, they focus in your skill to repay the mortgage. Thus, low revenue does not essentially imply disqualification. A formidable credit score rating or low debt-to-income ratio can considerably improve your probabilities.

Above all, at all times hold up to date monetary data. Lenders confirm these data to evaluate mortgage affordability. Your wage statements, tax returns, and financial institution data needs to be in good order.

Making certain you perceive the nuances of the FHA’s guidelines on minimal revenue necessities is vital. Generally, the interpretation varies between completely different mortgage firms. Bear in mind, information is energy when navigating the home-buying course of.

Documentation of Earnings

Correct revenue documentation is pivotal in FHA loans because it establishes your capability to afford a mortgage. Figuring out last mortgage percentages and rates of interest is vital to your mortgage approval course of.

A complete paper path substantiating your revenue is essential amongst frequent hurdles like fluctuating revenue or self-employment. This may occasionally embody W-2s, tax returns, or pay stubs.

FHA loans typically confront challenges of inconsistent or unconventional revenue. However, overlaying two years of revenue verification bridges this hole and strengthens your mortgage utility.

An important resolution lies in completely documenting all of your revenue sources. This contains revenue from part-time work, bonuses, or alimony, enhancing your debt-to-income ratio.

Whereas the method might sound intensive, precisely depicting your revenue and monetary stability expedites your FHA mortgage approval. Bear in mind, transparency and consistency are treasured in FHA mortgage revenue documentation.

Credit score Rating

Establishing a wholesome credit score rating turns into pivotal for FHA mortgage approval. The Federal Housing Administration emphasizes lenders checking your creditworthiness and reimbursement capability.

Addressing FHA mortgage hurdles may be made less complicated by means of credit score rating enhancement. Common invoice funds, minimizing bank card balances, and rectifying credit score report errors can precipitate an improved credit score standing.

Minimal Credit score Rating

Securing FHA loans necessitates a minimal credit score rating. It types an FHA mortgage problem, but it may be surpassed by bettering credit score conduct, well timed fee, and debt discount.

Usually, a credit score rating of 580 is the entry barrier for an FHA mortgage, enabling potential owners to entry a 3.5% down fee. These with decrease scores should still qualify, but with extra intensive down-payment necessities.

Understanding the credit score rating barrier is essential in FHA mortgage acquisition. This barrier, typically a problem, minimizes threat for the lender whereas defending the market’s stability.

A decrease rating will increase the perceived threat for lenders, leading to the next down fee requirement. This rule ensures the applicant’s dedication and skill to satisfy mortgage obligations.

Thus, to beat the problem of a minimal credit score rating, sustaining a wholesome credit score conduct, clearing your excellent money owed, and avoiding late funds can develop an excellent credit score rating, easing the FHA mortgage course of.

Credit score Historical past

Mastering the crafting of a strong credit score historical past for FHA loans is paramount. Your fee observe report and accountable credit score conduct are vital in securing the mortgage.

Coping with credit score historical past discrepancies is inevitable. Shortly figuring out and rectifying errors in your credit score report can improve your possibilities of FHA mortgage approval.

Debt-to-Earnings Ratio

Understanding the debt-to-income ratio is key within the FHA Mortgage course of. This metric, measuring your whole month-to-month money owed in opposition to your gross month-to-month revenue, can considerably affect your mortgage approval probabilities.

Boosting your monetary profile for a good debt-to-income ratio entails a two-fold technique – growing revenue or lowering debt. This will alleviate some challenges linked to buying an FHA mortgage.

Calculating DTI

Figuring out your Debt-to-Earnings (DTI) ratio is essential to securing FHA loans. It is calculated by dividing your whole month-to-month debt by your gross month-to-month revenue. This numerical worth expressed as a proportion helps lenders assess your skill to handle month-to-month funds.

Misconceptions about DTI calculations typically result in confusion and decreased possibilities of mortgage approval. DTI is not nearly bank card money owed or mortgages; it additionally contains pupil or auto loans, alimony, and youngster help.

Intention for a DTI ratio decrease than 43% to enhance your FHA mortgage eligibility. Decrease ratios point out that you’ve an satisfactory revenue to handle present money owed and a possible mortgage, making you extra interesting to lenders.

Watch out for the parable {that a} excessive revenue negates a excessive DTI. Regardless of substantial earnings, a excessive DTI signifies potential problem dealing with further mortgage repayments. All the time try for a balanced DTI for a smoother FHA mortgage approval course of.

DTI Limits

The Debt-To-Earnings (DTI) ratio restrict is a vital hurdle in FHA loans; it dictates the ratio of your whole month-to-month debt to your gross month-to-month revenue. This metric is essential in evaluating a borrower’s skill to reimburse the mortgage.

Falling wanting the DTI restrict? Adopting an creative resolution like paying down small money owed or including a major different’s revenue to the applying can simplify your compliance with the FHA’s DTI pointers.

Property Necessities

Property necessities in FHA loans comply with strict pointers established by the Federal Housing Administration. Your adherence to those necessities can skyrocket your possibilities of mortgage approval. Our complete information decodes these requirements, paving your technique to property possession.

Crusing by means of FHA mortgage property necessities may be overwhelming, with its justifiable share of hurdles. We make it easier to navigate these challenges, making certain a smoother journey in direction of your dream actual property funding.

Appraisal Compliance

Unlocking the secrets and techniques of FHA mortgage appraisal compliance eases potential mortgage hurdles. Past cash and credit score scores, properties should fare effectively beneath rigorous FHA appraisal. Recognizing this, savvy debtors guarantee properties meet company requirements.

Appraisal compliance poses a standard impediment in FHA mortgage processes. Nonetheless, surpassing this problem requires an understanding of what valuers concentrate on. The appraiser’s eye lies in your potential property’s security, safety, and structural soundness.

Appraisal compliance is an sudden ace within the FHA mortgage maze. A compliant property assists not simply in mortgage approval however in negotiating honest costs, too. Make investments time in studying and navigating compliance; it is well worth the renewed peace of thoughts and monetary security.

Inspection Necessities

The FHA mortgage inspection course of ensures the property is liveable and protected. The inspector, knowledgeable accepted by the Division of Housing and City Improvement, opinions the property’s exterior and inside for structural integrity.

Failing the inspection doesn’t suggest the sport is over; it opens a possibility to barter repairs with the vendor. Bear in mind, a well-negotiated restore can flip a draw back into an upside.

Approaching the inspection confidently and being ready to deal with essential repairs can assist conquer FHA mortgage obstacles. A property falling quick solely means devising a brand new technique staying inside the purpose.

In mastering FHA mortgage challenges, foreseeing potential restore points may be a part of your warrior’s arsenal. Nimbleness and readiness can skirt potential roadblocks, making certain a smoother journey to homeownership.

Mortgage Insurance coverage Premiums

Mortgage insurance coverage premiums (MIP) are integral to FHA loans, offering a security internet to lenders in case of purchaser default. Decoding MIP consists of an upfront premium at closing and an annual value unfold throughout month-to-month funds.

Methods to mitigate MIP-related challenges embody paying the upfront MIP out of pocket to keep away from elevated month-to-month funds or contemplating a traditional mortgage various if the MIP considerably impacts the affordability of the property.

Upfront MIP

Perceive that upfront Mortgage Insurance coverage Premium (MIP) is a hurdle generally encountered throughout FHA loans. It is a one-time, upfront premium paid at closing or financed into the mortgage. This component helps defend lenders from default-related losses.

The preliminary hurdle lies in comprehending the upfront MIP. Nonetheless, fret not. There are methods to attenuate the impression of this problem, resulting in a smoother FHA mortgage course of.

Assuaging this hurdle is achievable by means of strategic monetary planning. Though the FHA requires the Upfront MIP, it may be rolled into your mortgage, thus easing the upfront value on the closing desk.

To additional handle this hurdle, think about securing a mortgage with a decrease principal quantity. This resolution successfully minimizes the quantity of the upfront MIP, paving the way in which for a profitable residence buy with FHA loans.

Annual MIP

The Annual Mortgage Insurance coverage Premium (MIP) may be daunting for FHA mortgage candidates. Its inescapability forces debtors to strategize round this impediment to safe the mortgage efficiently. By understanding the ins and outs of Annual MIP, they’ll strategically prepare for this extra payment.

Contemplate factoring the Annual MIP into your long-term monetary planning to navigate this problem. Changing this annual value right into a month-to-month expense can help in higher monetary administration, making the MIP funds much less overwhelming.

Reprioritizing spending and budgeting for this MIP can help debtors in assembly this requirement with out straining their funds. It is lifelike planning that acknowledges the precise value of an FHA mortgage.

Leveraging these methods can be certain that the Annual MIP turns into an achievable hurdle, slightly than a roadblock, in securing an FHA mortgage. A savvy method takes the strain off, remodeling challenges into surmountable duties.

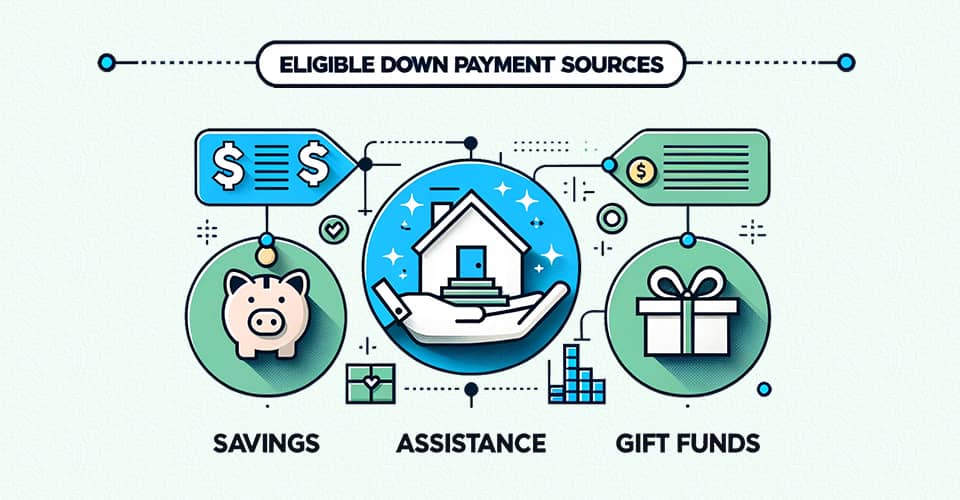

Down Cost

Addressing the down fee dilemma could appear daunting for potential FHA mortgage candidates. Nonetheless, sourcing funds from eligible down fee sources, reminiscent of financial savings or present funds, could be a viable resolution.

Crossing the down fee barrier for FHA loans requires efficient methods. As an example, supplementing private financial savings with down fee help packages can assist assignees attain the minimal wanted extra shortly.

Minimal Down Cost

Demystifying minimal down funds for FHA loans can alleviate patrons’ anxiousness. Based mostly on the borrower’s credit score rating, a purchase order necessitates as little as 3.5% down. Consequently, residence possession turns into accessible, even for these with modest financial savings.

Whereas conventional loans might mandate the next proportion, FHA loans introduce flexibility. Debtors can accumulate the mandatory funds by means of varied sources, together with items from household or grants.

The puzzle of minimal down funds unravels with understanding. Familiarizing oneself with FHA mortgage necessities can flip the dream of homeownership into actuality. Information and preparation remove the obstacles.

Various Down Cost Sources

There are a handful of different avenues to probe for potential homebuyers encountering hurdles with the required down fee for an FHA mortgage.

Leveraging them can present an efficient workaround for this frequent impediment, providing artistic options to satisfy FHA mortgage necessities.

Items from household, pals, or employers that may contribute to the down fee.

Grants from not-for-profit organizations or native authorities companies.

Loans from retirement or funding accounts.

Proceeds from promoting an present property, reminiscent of a automotive or residence.

Financial savings particularly from Particular person Improvement Account (IDA) packages.

Mortgage Limits

When making use of for FHA loans, navigating the panorama of mortgage limits could be a vital problem. It is a main stumbling block that would deter potential homebuyers and actual property buyers. This key side profoundly influences your borrowing capability and, finally, your home-owning dream.

Understanding the intricate particulars of those mortgage limits in FHA loans may be instrumental in overcoming this hurdle. Subsequently, studying about and totally greedy these nuances would supply a strategic resolution to alleviate any potential issues relating to mortgage limits.

Gaining information on particular FHA mortgage limits based mostly on counties and states.

Analyzing your monetary state of affairs to know how a lot you may qualify for.

Revisiting your budgets to satisfy mortgage restrict requisites.

Exploring the choice of getting an FHA-approved appraiser to evaluate the property’s worth.

Contemplate high-cost space mortgage limits should you plan to purchase a house in costly actual property markets.

{kind=link}