The way to Assemble a Lengthy-Solely Multifactor Credit score Portfolio?

There exist two commonest methods for developing multifactor portfolios. The blending strategy creates single-factor portfolios after which invests proportionally in every to construct a multifactor portfolio. The built-in strategy combines single-factor alerts right into a multifactor sign after which constructs a multifactor portfolio based mostly on that multifactor sign. Which methodology is healthier? It’s exhausting to inform, and quite a few papers present every technique’s professionals and cons. The current paper from Joris Blonk and Philip Messow explores this query from the standpoint of the credit score fixed-income portfolio supervisor and provides their evaluation, which reveals that an built-in strategy might be higher on this specific asset class.

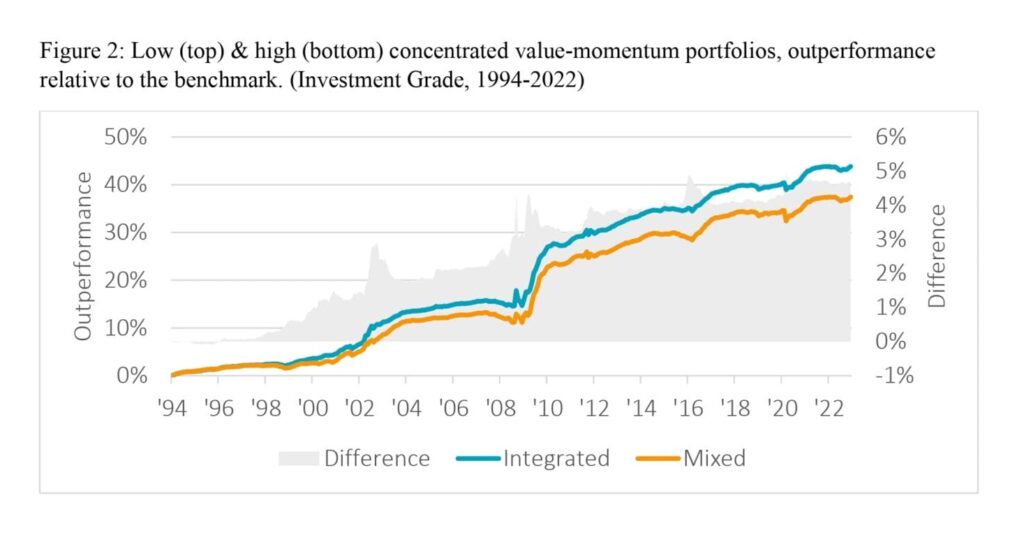

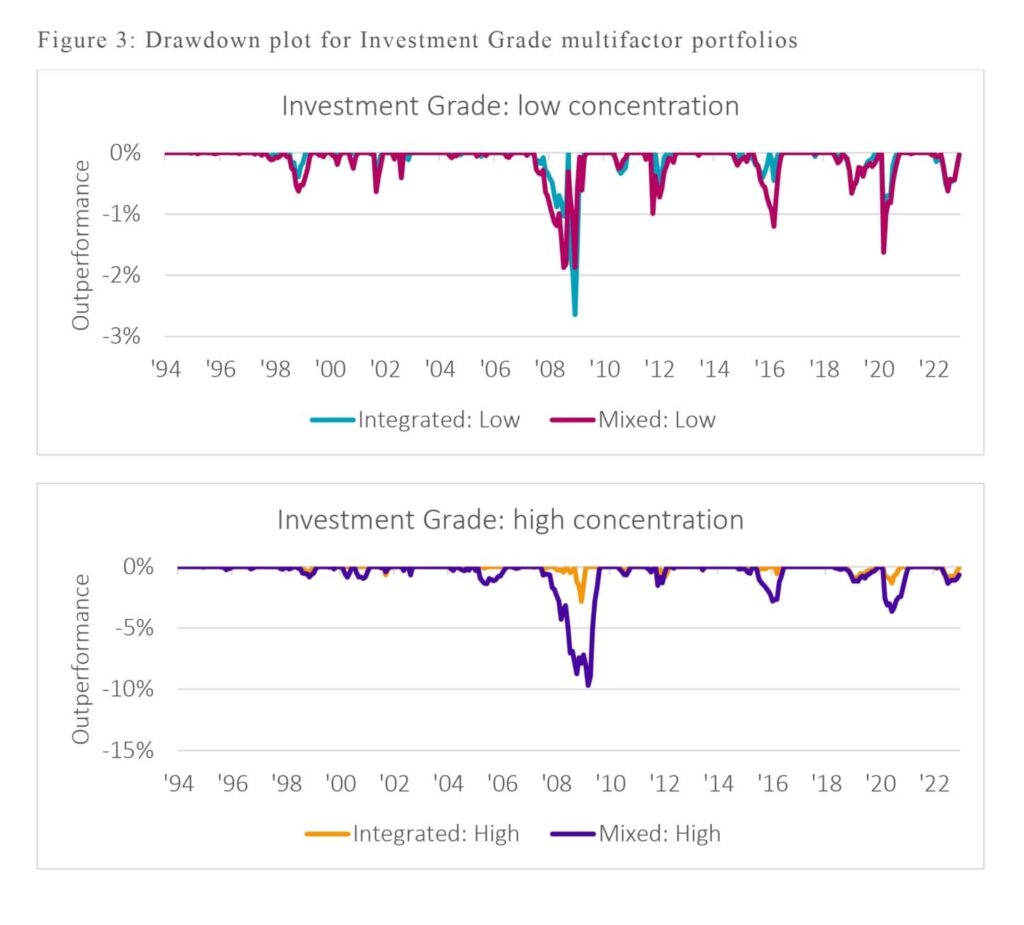

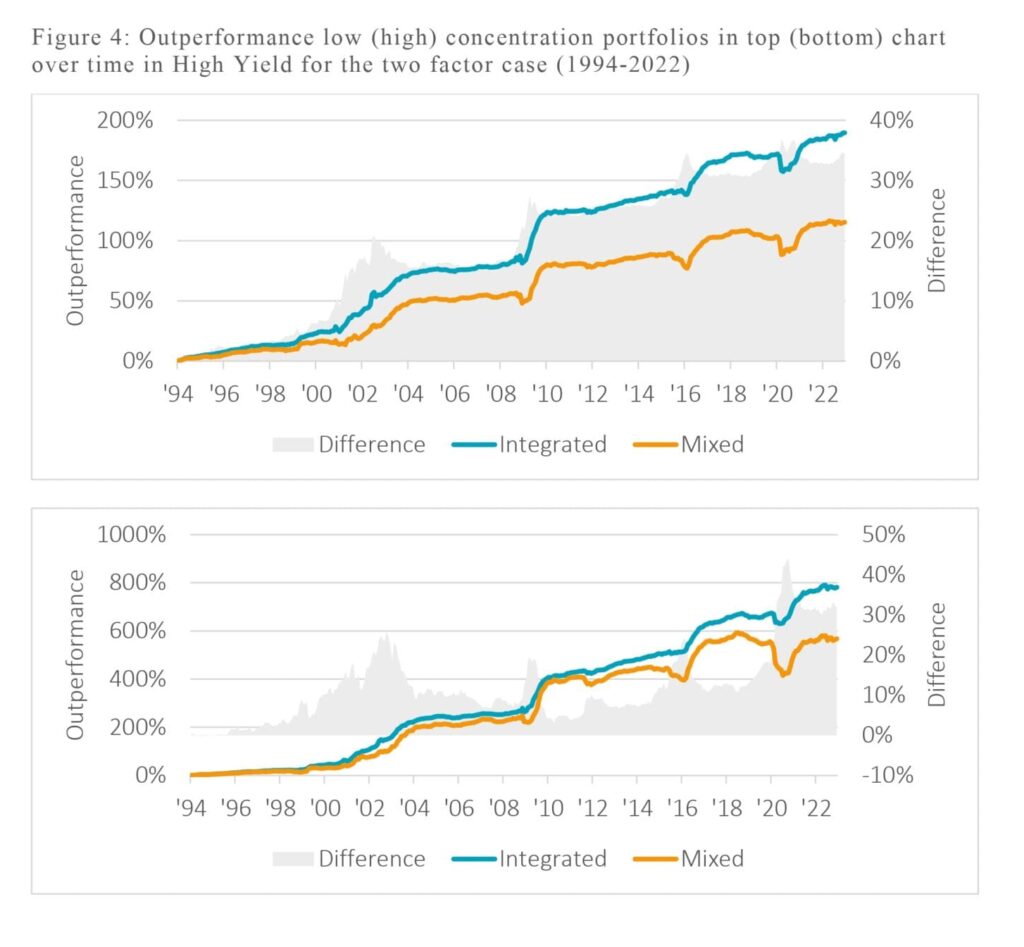

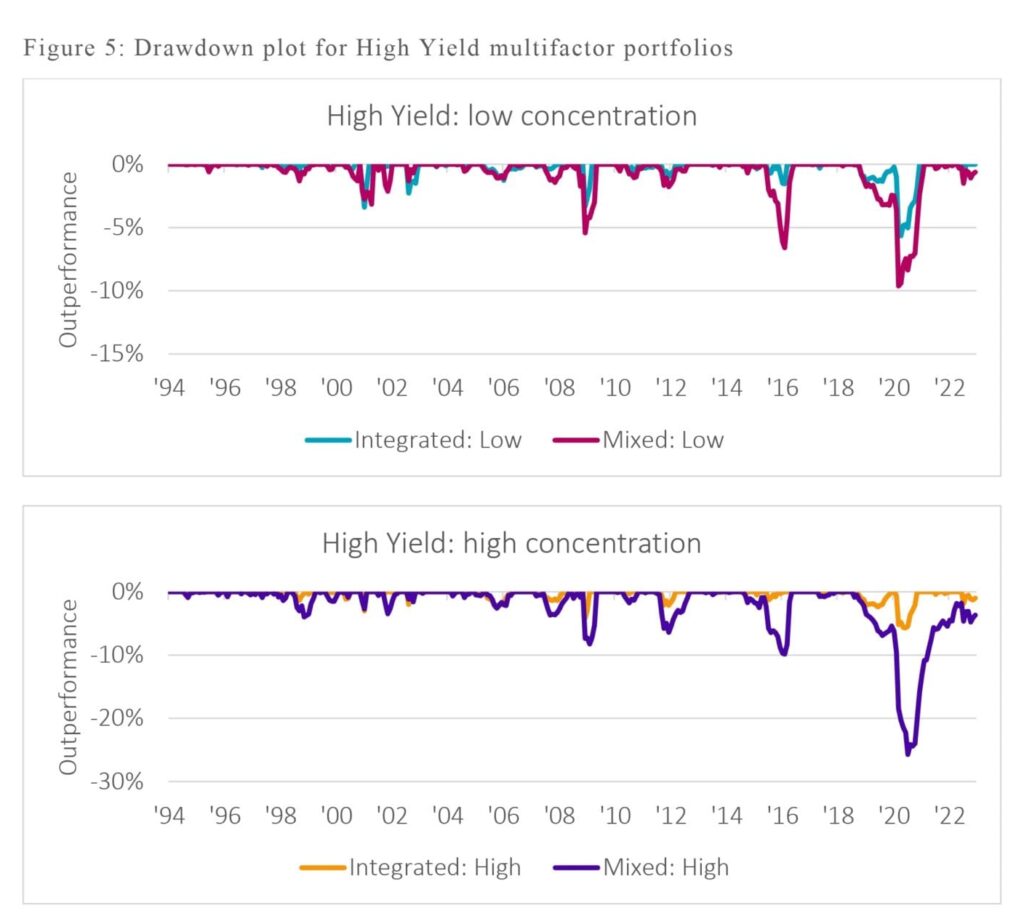

To make these two approaches comparable, authors use exposure-matched portfolios and restrict themselves to long-only portfolios, as long-short methods are extra of a theoretical assemble than a sensible, sensible utility for company bond traders. The authors discovered constant outcomes that indicated that built-in multifactor portfolios outperformed blended multifactor portfolios. These outcomes maintain throughout completely different funding universes (Funding Grade and Excessive Yield), completely different underlying issue suites (two or 4 elements), completely different publicity concentrations (low or excessive), and completely different market environments (falling/rising rates of interest, falling/rising credit score spreads, and so on.).

As well as, they present that an built-in strategy reduces draw back threat by avoiding investing in bonds with offsetting single-factor exposures (e.g., excessive worth & low momentum), the so-called “worth traps.” Most research within the credit score issue investing literature lack a solution to implementing these methods below sensible situations and attaining engaging risk-adjusted returns. Their evaluation supplies a primary route for translating these theoretical research into “actual” portfolios. Subsequently, this research has essential implications for practitioners who wish to implement multifactor methods for company bonds.

The subsequent logical step can be to ask one other query – which strategy is healthier in all-equity funding universe the place shorting is allowed and simpler?

Authors: Joris Blonk and Philip Messow

Title: The way to Assemble a Lengthy-Solely Multifactor Credit score Portfolio?

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4775767

Summary:

This paper examines how one can mix single elements right into a multifactor portfolio of company bonds. The 2 commonest approaches within the literature are the so-called ‘built-in’ and ‘mixing’ approaches. This paper analyzes these two strategies in company bond markets, and finds that the built-in issue portfolios typically result in increased risk-adjusted returns. That is largely because of the truth that they don’t put money into underperforming bonds that rating poorly on a single issue, to which the ‘mixing’ strategy is uncovered to. Our outcomes are sturdy over time and maintain in several macro environments and in each Funding Grade and Excessive Yield markets.

As at all times, we current a number of thrilling figures and tables:

Notable quotations from the tutorial analysis paper:

“Within the purest type of passive fairness investing, an investor’s portfolio contains every inventory available in the market in actual proportion to its weight available in the market (i.e., the overall inventory market index). Nonetheless, for a number of causes, together with that it’s impractical for many traders to carry a number of thousand shares, funds usually try to copy solely a subset of the market, often known as an index. They accomplish that utilizing certainly one of two strategies.

First, proudly owning every inventory in proportion to the underlying index is called full replication. This technique is difficult for a lot of causes, together with that it usually requires changes to all (i.e., tens, lots of, or hundreds) of the portfolio’s positions every time an index provides or removes a inventory. Lots of the required changes are small and pertain to comparatively illiquid shares, which creates the potential for big buying and selling prices that scale back the advantages of replication.

The second strategy, known as consultant sampling, selects solely a subset of index elements for inclusion within the investor’s portfolio, however retains the aim of matching index returns. In fact, sampling creates the potential for even better monitoring errors and thus strays farther from the passive excellent. Nonetheless, as a result of the technique requires holding fewer shares, it might scale back buying and selling prices, which might improve returns. For instance, as a result of they don’t maintain all the index, samplers may be capable of keep away from probably the most illiquid shares or keep away from buying and selling following many cases of index reconstitution.

We present that sampling funds have increased turnover than replicating funds. This implies that the lively part of sampling, or the number of shares utilizing variables apart from index weights, greater than offsets any discount in buying and selling arising from holding fewer positions. We additionally discover that sampling funds have increased expense ratios and administration charges, in keeping with the prices of lively choice greater than outweighing the advantages of holding fewer positions, and with fund managers searching for compensation from traders for his or her efforts to actively make investments. Nonetheless, our examination of fund returns suggests these increased bills and costs usually are not warranted as a result of the sampling fund managers don’t seem like expert at lively investing. Particularly, sampling funds’ returns are decrease than replicating funds.

A number of extra analyses assist and lengthen our primary outcomes. First, our outcomes maintain in subsamples of S&P 500 indexers and different market-cap-based indexers, which helps rule out issues that our findings are pushed by one or just a few peculiar indices, by “type” or “sector” funds, or by unobservable cross-index variations. Second, we discover that our outcomes are strongest amongst funds following indices with fewer constituent shares, and that they totally disappear for samplers following indices with 1,000 or extra shares. This implies sampling shouldn’t be dangerous solely when it could possibly drastically scale back the variety of shares held within the portfolio. Third, we discover that traders’ funds more and more circulate to samplers relative to replicators over our pattern interval, which is puzzling given our value and return outcomes.

The variations in prices, returns, and flows we doc are economically vital. For instance, replicators outperform samplers by about 60 foundation factors (bps) per 12 months on a web return foundation. For example the potential wealth results of this distinction, contemplate a hypothetical investor who makes a one-time index funding of $100K at 35 years outdated and holds the funding for the subsequent 30 years. Assuming a relentless 8% annual return, the investor’s holding might be value about $1,000K at age 65. Nonetheless, if annual returns are 60 bps decrease (i.e., 7.4%), then the worth of the investor’s holding would solely be about $850K at age 65. This $150K, or 15%, distinction in portfolio worth is roughly equal to shedding the final two years of returns over the 30-year horizon.

Most significantly, our findings must be helpful to fund managers making an attempt to resolve how one can monitor an index, to plan sponsors choosing funding choices for a corporation’s workers, and to the last word traders making an attempt to judge their index fund managers. The disparate approaches and outcomes of replication vs. sampling have been stunning to monetary economists (together with each lecturers and practitioners) with whom we have now shared our outcomes to this point. To us, this implies that almost all mom-and-pop traders, and even many finance professionals, are doubtless equally unaware of the distinctions.”

Are you searching for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to be taught extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing supply.

Do you wish to be taught extra about Quantpedia Professional service? Test its description, watch movies, overview reporting capabilities and go to our pricing supply.

Are you searching for historic knowledge or backtesting platforms? Test our record of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a good friend

{kind=link}