An equities dealer’s place is taken into account “flat” once they have zero publicity to the market – no internet lengthy nor internet quick the market.

In some platforms, there’s a “flatten” button {that a} dealer can press in a market crash.

This function will attempt to exit their positions for equities merchants till all their positions are closed.

It is a little more difficult for the choices dealer, and there may be doubtless no flatten button in your specific platform.

So at this time, we’ll present you methods to purchase a lengthy put (or a protracted name) to flatten your portfolio delta briefly.

Contents

By getting your portfolio delta to as near zero as attainable, we take away the directional publicity. We’re not eliminating the vega (or volatility) publicity.

Nevertheless, directional publicity is a very powerful concern in preserving capital if the market strikes quick in a single route.

Because the market strikes quicker happening than up, we’ll begin with an instance portfolio with a optimistic delta and fake that the market is shifting down in opposition to us.

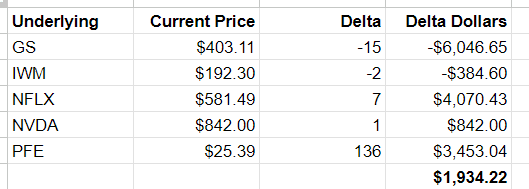

Suppose we have now choices positions on these shares:

It doesn’t matter if the place is an iron condor, butterfly, calendar, or diagonal as a result of the Greeks give us all the mandatory info.

To get rid of directional publicity, we’re solely involved with the positional delta of every place.

A very powerful quantity to calculate is the portfolio Delta {Dollars}.

To calculate this quantity, we multiply the place delta by the inventory’s present value.

Combination this for all shares within the portfolio.

Within the above spreadsheet, we calculated the portfolio Delta {Dollars} to be optimistic $1934.

That is equal to an equities dealer being lengthy $1934 price of inventory.

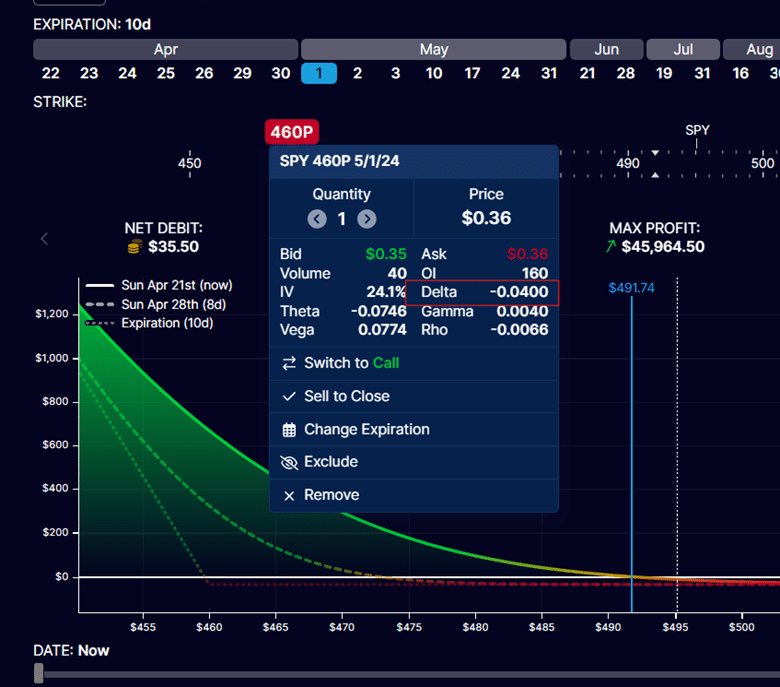

Attempting to get the $1934 Delta Greenback right down to zero by promoting or adjusting choice positions is simply too time-consuming when the market is shifting quick.

As an alternative, we’ll purchase a put choice in SPY (the S&P 500 ETF).

Suppose that the scale of SPY is $495 on the time.

$1934 / $495 = 3.9

We want a SPY put choice that has a -4 delta.

Wanting across the choice chain, we discover {that a} put choice with the 435-strike value expiring in 26 days has a couple of -4 delta.

This put choice prices about $60.

Or we are able to purchase a put choice with the 460-strike value, expiring in 10 days, with the same -4 delta. This feature will price much less at $35.

However it’ll lose its worth quicker.

In any case, this can be a momentary measure whereas the market is dropping.

It provides you time to correctly modify or exit your positions.

Because the market strikes, the delta {dollars} will certainly change, and the put choice could have to be exchanged with one other one with completely different deltas.

Obtain the Wheel Technique eBook

If the portfolio Delta {Dollars} is damaging and the market goes up in opposition to us, we have to purchase a name choice.

As a result of the market goes up, we’d like a bullish name choice.

We want one with the correct quantity of delta to offset the damaging Delta {Dollars} by performing the same calculation.

Why can’t we simply take a look at the place delta of every place?

Merely trying on the place delta is just not ample. Within the above, we see that PFE has a delta of 136.

One may suppose that that is the place that has essentially the most directional publicity.

However that may be incorrect.

The scale of the underlying value is vital. NFLX, with a delta of seven, has a bigger Delta Greenback than PFE as a result of one share of NFLX is many instances bigger than one share of PFE.

Therefore, we have to take a look at the Delta {Dollars} for the calculation.

Does the variety of contacts matter?

The variety of contracts does matter.

Nevertheless, it’s already accounted for within the place delta.

The place delta of the place already considers the variety of contracts.

A place with double the variety of contracts would present a positional delta twice as massive.

What if we have now damaging Delta {Dollars}, and the market is crashing?

If the market goes down when you have damaging Delta {Dollars}, the portfolio ought to theoretically achieve worth because the market goes in the identical route because the delta.

Nevertheless, the results of vega haven’t been accounted for and could also be affecting the P&L of the place.

In both case, the damaging Delta {Dollars} could change rapidly, and you want to recalculate this quantity rapidly (in case your platform doesn’t already do it for you).

In some unspecified time in the future, the damaging Delta {Dollars} could even grow to be optimistic Delta {Dollars}.

Can we use one other underlying to hedge?

It’s also attainable to make use of one other underlying, similar to IWM, SPX, or RUT, to carry out this delta hedge.

Should you discover that you just want a 100-delta put, don’t purchase an choice that’s so far-off from the cash.

As an alternative, purchase two 50-delta put choices.

Should you discover that you just want 10 SPY put choices, you should buy one SPX put choice as an alternative – roughly talking, you want to do the precise calculations.

How come I don’t discover a 4-delta put choice within the choice chain?

The platform could present the delta on a “per share” foundation.

The deltas we’re utilizing on this article are on a “per contract” foundation, which means they’ve already been multiplied by 100.

What we name a 4-delta put is proven in some platforms as “-0.04.”

Can we use this hedging approach for inventory portfolios?

Sure, one share of inventory is one delta, so in case you have 5 shares of NVDA at $842 per share.

Then your Delta {Dollars} is $4210 for that place.

To flatten our portfolio delta, we have to know the Delta {Dollars} of our portfolio.

Take this quantity and divide it by the value of SPY to find out what delta put or name you want to purchase.

Purchase a put if the market goes down in opposition to our place.

Purchase a name if the market goes up in opposition to our place.

We hope you loved this text on methods to rapidly flatten delta.

You probably have any questions, please ship an e mail or depart a remark beneath.

Commerce protected!

Disclaimer: The knowledge above is for academic functions solely and shouldn’t be handled as funding recommendation. The technique offered wouldn’t be appropriate for traders who are usually not accustomed to change traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.

{kind=link}