Luis Alvarez

Expensive subscribers,

I have been pretty clear in the previous couple of months about the truth that I am going into Workplace REITs, and my three picks of Highwoods (HIW), Kilroy (KRC), and Boston Properties (BXP).

My shares have been purchased at a mixture of valuations, however one factor all of them have in widespread after the previous couple of days is that they are all firmly within the inexperienced. Additionally, the truth that not one of the corporations talked about are any longer at what I might contemplate their “backside”.

The newest few days of rate-related and macro-related surges have resulted in a really a lot modified upside for a lot of of those REITs.

In fact, on the identical time, I’ve seen over the previous few days, in feedback and in solutions, that now may be the time to put money into these workplace REITs.

What?

This text seeks to supply solutions and a few steerage, for buyers who want to study one thing about valuation and techniques that may be utilized to most buyers seeking to beat the market utilizing elementary methods.

Workplace REITs – why I’ve outperformed, and why I am not promoting (but)

I’ve written at least ten articles on the aforementioned corporations throughout 2023 in a mixture of singular and multi-company articles the place I’ve, time and time once more, known as these corporations to be price shopping for. Whereas it is true that I’ve all the time been clear in regards to the dangers and can proceed to be this right here – keep in mind, we’re speaking about workplace house, the false equivalency that many buyers have fallen to right here is that as a result of workplaces are seeing a downturn, all workplace property corporations needs to be prevented.

I hope that the previous few days have proven you, if you happen to’ve prevented these investments like many appear to have achieved, that this isn’t the case and the way a lot of the undervaluation was perceived price threat to the businesses in query.

Is the danger over?

No, I might argue that the basic threat to those corporations is just about unchanged since my final set of articles for them. The market might imagine itself to have higher visibility for 2024, however:

These firm fundamentals haven’t modified. Their credit standing has not modified. Their dividends haven’t modified Their administration has not modified.

What has modified is market notion. And as you’ve got seen over the previous few days, if you happen to miss out on these few up-days, then you definitely miss out on an entire lot of progress. Lots of the workplace corporations in query, the place I’ve secured yields of over 7.5% on value, are actually yielding lower than 5.5-6%.

Not solely is that this materially deteriorated from their earlier, interesting valuations throughout troughs, but it surely’s at a stage the place I might argue that there are corporations with higher upside right here.

Let me title a fast instance.

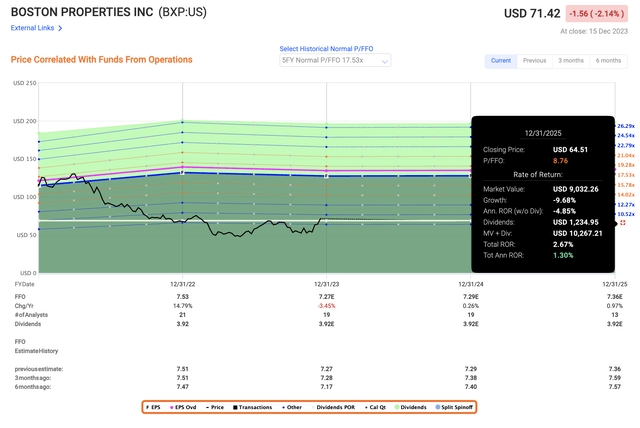

On the one hand, I’ve Boston Properties – an excellent, BBB+ rated workplace price. On the trough, it yielded over 7% and I might see a conservative upside of 25% yearly, by which I imply an upside to lower than 8.7x P/FFO even with a progress of almost 0% till 2025E. At a 25% upside, this was an excellent potential – however now the potential to that 8.7x is like this.

F.A.S.T Graphs BXP Upside (F.A.S.T Graphs)

Whereas the corporate might go increased, we additionally have to estimate the place this firm might go, and the way excessive it might go given the expansion price the corporate is forecasted.

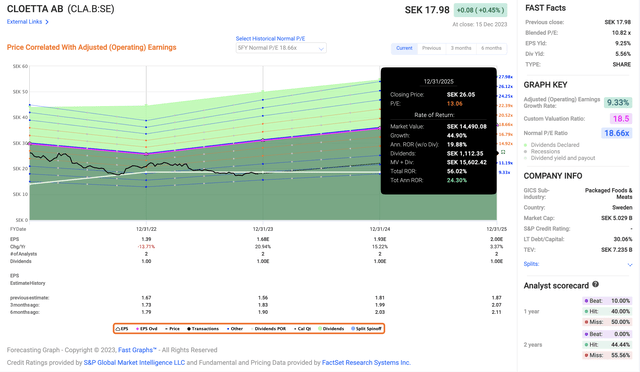

After which evaluate it to one thing like Cloetta (OTCPK:CLOEF). This can be a Swedish sweet and meals firm yielding extra at 5.56%, with an upside to a conservative 13x P/E that appears like this.

F.A.S.T Graphs cloetta upside (F.A.S.T graphs)

So you possibly can see how an organization’s enchantment on the broader market relies on a large number of things, however all issues being equal, valuation is the important thing deciding issue. So if selecting between these two corporations immediately, and if I did not have full publicity to Cloetta AB, that is what I might add to my portfolio.

The newest few days have actually pushed all of those REITs, particularly these which were considerably undervalued, to ranges the place they could not be that interesting if we assume {that a} zero-growth estimate leads to pressured multiples for the subsequent few years.

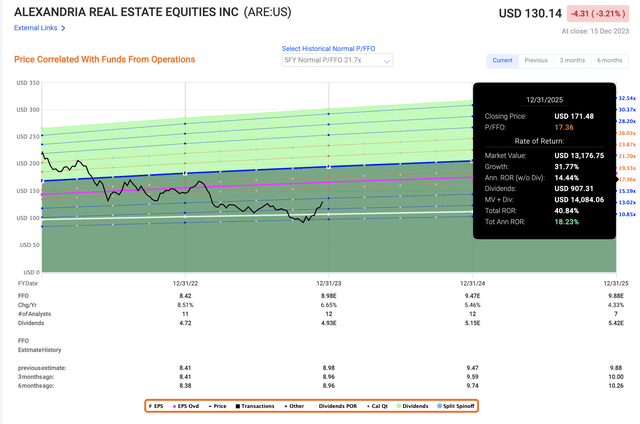

As I have been saying in my previous articles, these workplace REITs have been undervalued for a really very long time, and regardless of pressured progress charges and refinancing dangers, all of them have additionally proven continued sturdy demand for his or her properties – and we’re not even speaking about Alexandria (ARE) right here, the REIT that has been achieved greatest by far, with RoR of over 30% since my funding.

On this article, I wish to make clear the place I see the enchantment for Workplace REITs like BXP, HIW, and KRC after this latest surge.

I wish to clearly state that there’s continued enchantment in investing right here, however wish to make it equally clear that the very best upside has now handed.

I am speaking in regards to the upside to a 7-9x P/FFO for these REITs of over 20%. With the intention to get these charges of return now, you want to really estimate these REITs buying and selling at double-digit multiples, within the case of KRC, virtually above 11x to get a 15% annualized RoR right here. (Supply: F.A.S.T graphs)

These should not outlandish calls for or projections – not when you think about that KRC as an example, manages a historic premium of virtually 18x P/FFO.

However is that premium probably in a world of a 4-5% risk-free price when the corporate is forecasted, with 100% accuracy, to develop earnings at damaging quantities for the subsequent few years?

Whereas all the workplace REITs have seen a resurgence, and all of their quarterly experiences and releases present operational stability that may deny any kind of elementary decline firmly, all the forecasts are very clear in a single matter.

Any kind of FFO/AFFO progress within the subsequent few years might be small, if not barely damaging. And when you might generate double-digit returns, these returns grow to be much less and fewer interesting the upper these shares go.

That is why I preserve a really shut eye on high quality shares – like these workplace REITs – and as soon as they really go decrease, I purchase extra.

When Alexandria hit double digits, that is after I actually dialled up my shopping for. Alexandria represents the one largest workplace REIT in my portfolio and over 1% of my present whole, each privately and commercially for a really particular set of causes.

Take my standards for example.

Alexandria is BBB+ rated. Alexandria’s dividend is extraordinarily well-covered. Alexandria, in contrast to these different REITs, is estimated to develop at 4-5% FFO yearly. Alexandria has a historic 10-year 100% forecast accuracy (Supply: FactSet) Alexandria is a little more specialised by way of the workplace sub-sectors and is unlikely to see a big decline even in a tough market atmosphere.

The entire different workplace REITs have enchantment as nicely – and are cheaper – however none are as qualitative, and I at the beginning concentrate on high quality.

Let’s take a look at what kind of shopping for appeals these REITs nonetheless have immediately.

Valuation for KRC, HIW, BXP (And ARE).

We now enter what I view as a interval to be extra cautious. I view valuations for a lot of corporations at their peak, or at document ranges. I preserve a big listing of corporations that I cowl along with worth targets, and I’ve not often seen so few price shopping for as I’m seeing immediately. The potential for corporations to “drop” again down appears increased presently.

That being stated, if you wish to put money into Workplace REITs now, it is not “too late”, offered you average your progress assumptions.

Lower than 2 weeks in the past, you possibly can get 20%+ annualized RoR if forecasting ARE under 15x P/FFO. At the moment you want to forecast it at 16-17x P/FFO to get above 15% per 12 months and solely a yield of three.9% as a substitute of virtually 4.5%. The present share worth is not unattractive, and I nonetheless contemplate ARE to be a “BUY”, with the next lifelike upside.

ARE Upside (F.A.S:T graphs)

That is the highest-quality workplace REIT upside, and I refer you to my different articles to grasp why this is not your typical workplace REIT.

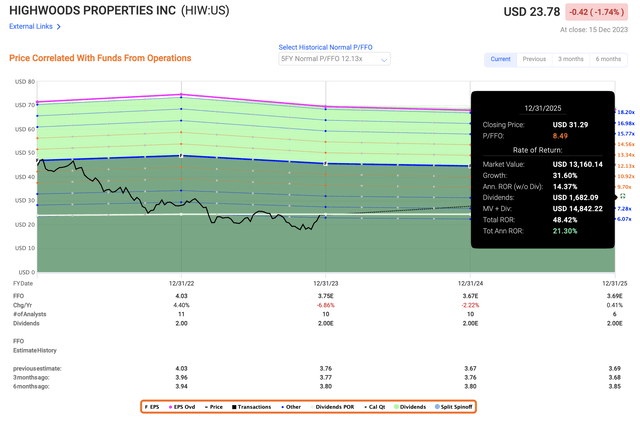

Out of the opposite REITs right here, they now commerce at a mixture of valuation multiples – often associated to fundamentals and progress prospects. Highwood is by far the most cost effective of the bunch, at present nonetheless at an 8.4%+ yield, however the REIT can also be the one which’s anticipated to say no over 1% per 12 months, making an upside to any considerably “excessive” a number of much less probably than the others.

I nonetheless contemplate Highwood a “BUY” right here, however solely to a 7-8x P/FFO, at most 8.5x. And to an 8.5x, this firm nonetheless manages round 21% yearly – although once more, we’re speaking about investing in an organization that appears more likely to decline, which places a query mark on any upward trajectory it might need.

HIW Upside (F.A.S.T Graphs)

An identical case is true for Boston properties – although that is the one workplace REIT I cowl right here, besides Alexandria, that is anticipated to develop FFO. Even when that progress is just 0.5% per 12 months. Nevertheless, because of this, the corporate is near 10x P/FFO right here in comparison with HIW, and you want to estimate it at 12.5x to get even 17% per 12 months.

My level right here is that these charges of return are fairly good, however nowhere close to pretty much as good as they as soon as have been solely 2-3 weeks again, or months again.

My level is that whole sectors or subsectors generally, irrationally, commerce down for prolonged durations, and that is the time to put money into them – not after they’ve already recovered over 10-18%, which is what has occurred solely previously 1-2 weeks.

It requires figuring out what I contemplate to be basically sound companies. You may even see that I’ve not coated companies I contemplate riskier all that a lot, however as a substitute concentrate on the BBB-rated or above corporations, the place any elementary decline over the long run appears fairly far off. Whereas I do personal a stake in Medical Properties Belief (MPW), as an example, that stake is extraordinarily small – and whereas I do view it as a “spec” purchase, it is a enterprise that whereas yielding 11%, can also be estimated at rising FFO damaging 6% or much less yearly within the subsequent few years. Couple this with some administration points, and I am clear why I’m not going as deep as within the corporations that I’ve talked about right here.

My level right here is, concentrate on valuation

My level is that I’m continually searching for the very best valuation and fundamental-related upsides, and whereas Workplace REITs are nonetheless good picks right here, their threat profile has not, a minimum of to my thoughts, materially improved or declined. The market’s view on them has. Nevertheless, this latest surge has made different choices much more fascinating – as I confirmed you with my instance for Cloetta. There are maybe 15-20 undervalued corporations that I might say have much less of a damaging rate of interest threat than these REITs do, and these have all grow to be far more fascinating to me after the previous few weeks.

As we’re shifting towards the tip of 2023, I feel it is vital to be lifelike about what 2024 might carry. Whereas we’d see a continuation of the optimistic growth we have seen thus far, I want to err on the facet of warning right here and anticipate a much more sobering expertise for the approaching funding 12 months.

That is why my battle cry for 2024 might be centered round choosing solely probably the most qualitative however undervalued equities to put money into – corporations with excessive outperformance potential even within the case of sub-par growth.

Should you missed out on investing in these 4 corporations at trough valuations, then I hope that my articles for the rest of 2023 and going into 2024 can give you qualitative concepts for the place one might put one’s cash for the quick, medium or longer-term.

I am going to proceed to offer conviction right here, within the sense that I very, very not often write about corporations I’ve no “pores and skin within the sport in”, and make it very clear the place I see the risk-reward ratio.

For now, that is what I see for the Workplace REITs that I cowl right here. I contemplate them “BUY” nonetheless, however their enchantment has materially modified from only some weeks again.

{kind=link}