EdithRum

Article Thesis

Rolls-Royce Holdings plc (OTCPK:RYCEY) is an aerospace provider that has carried out properly over the past yr, however the longer-term previous is fairly checkered. Shares have gotten fairly costly in current months, I consider, which makes me consider that Rolls-Royce just isn’t one of the best choose for aerospace publicity.

Firm Overview

Whereas the identify Rolls-Royce could sound a bell in terms of luxurious vehicles, these should not manufactured by Rolls-Royce Holdings plc. As a substitute, the Rolls-Royce vehicle enterprise, known as Rolls-Royce Motor Automobiles, belongs to BMW Group (OTCPK:BMWYY). Rolls-Royce Holdings is an organization that designs, produces, and sells energy and propulsion techniques, primarily for plane, but additionally for sea and land autos, with some on-site (stationary) energy techniques being bought on high of that.

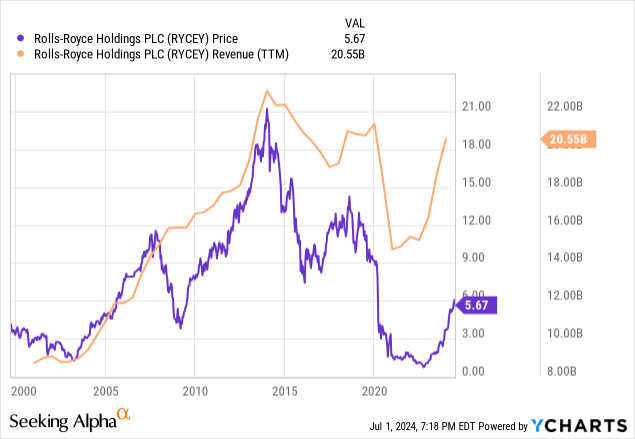

Rolls-Royce has a historical past relationship again far more than 100 years and its product line-up has, in fact, modified considerably over that point. Airplane engines didn’t exist when Rolls-Royce Holdings was based in 1884, and neither did nuclear-powered submarines and different merchandise for which Rolls-Royce has turn out to be a provider through the years and many years. However whereas Rolls-Royce’s historical past is lengthy, it’s checkered — the corporate has not been working from success to success and even needed to declare chapter in 1971. As we are able to simply see within the following chart, the final twenty years had been removed from good as properly:

Rolls-Royce’s revenues rose comparatively constantly from the start of the century to 2014, earlier than trailing off for a few years. Throughout the preliminary section of the pandemic, when many plane had been grounded attributable to journey restrictions, revenues took a giant hit, though the corporate has recovered shortly because the pandemic waned. Nonetheless, revenues are round 10% beneath all-time highs proper now, which, factoring in inflation over the past decade, is sort of significant.

The corporate’s share value fared even worse, nevertheless — Rolls-Royce at the moment trades at round one-fourth of the all-time excessive value seen a decade in the past. When an organization sees its shares drop this a lot, there should be main points at play, particularly after we think about that the broad market (SPY) has nearly tripled over the past decade. Whereas traders turned $10,000 within the S&P 500 into $27,000, earlier than dividends, over the past decade, a $10,000 funding in Rolls-Royce on the highs from 2014 would have became a measly $2,700.

We additionally see that the descent started manner earlier than the pandemic; thus, whereas the pandemic brought on non permanent headwinds, Rolls-Royce Holdings’ points started earlier than that. Trying on the firm’s previous outcomes, we see that Rolls-Royce Holdings generated losses for a few years, in 2016 and from 2018 to 2020. With losses of as much as $5 billion per yr, the corporate misplaced great quantities of cash even whereas producing strong revenues. The difficulty thus was clearly on the price aspect, not on the income aspect. Rolls-Royce Holdings needed to write down greater than $4 billion of property in 2016, its worst yr from a web earnings perspective, with these write-downs being primarily associated to forex hedges and different monetary objects.

Value-cutting applications adopted, and Rolls-Royce let go of 1000’s of individuals, which, in fact, brought on extra one-time bills within the following years attributable to severance funds, and many others. With the pandemic inflicting airways to cut back their orders and with provide chain points leading to decrease plane manufacturing numbers, the subsequent issues appeared, though Rolls-Royce Holdings wasn’t at fault when it got here to the pandemic — it was unfortunate to be energetic in an trade that was hit tougher than many others.

The excellent news is that Rolls-Royce Holdings has seen its working efficiency enhance markedly because the pandemic, as revenues have risen sharply and because the restructurings have begun to repay, with Rolls-Royce Holdings seeing an improved value construction that allowed the corporate to generate a pleasant $3.1 billion web revenue final yr — the very best since 2017.

Rolls-Royce Holdings: Energetic In Progress Markets

And in 2024 and past, Rolls-Royce Holdings may see ongoing enterprise progress as properly. The corporate is forecasted to see its revenues broaden by 9% this yr, with income progress for 2025, 2026, and 2027 being forecasted at 8%, 7%, and 6%, respectively, utilizing the Wall Road analyst consensus estimate.

This progress will seemingly be pushed throughout a number of of Rolls-Royce Holdings’ enterprise models. First, the civil airplane market is experiencing good progress, and the corporate will profit as a serious civil plane engine producer. International air journey numbers proceed to rise, regardless of excessive prices and environmental issues. Progress is pushed by international locations with quick financial progress equivalent to India. Over the past couple of years, Indian airways have made large new plane orders, as these carriers wish to broaden their fleets significantly with a purpose to service the rising home market in addition to rising demand for worldwide journey. Round a yr in the past, Looking for Alpha reported a huge 500 plane order from India’s IndiGo, and different Indian carriers equivalent to Akasa Air have lately made enormous orders as properly. Whereas not all of those airplanes will use engines from Rolls-Royce Holdings, total progress within the civil plane market will probably be helpful for Rolls-Royce for certain. India just isn’t the one rising market, as China is seeing rising airline journey as properly, and even in lower-growth markets equivalent to Europe, airways wish to enhance their gas effectivity and are thus upgrading their fleets to convey down emissions and gas bills — which implies that new, extra environment friendly engines are wanted.

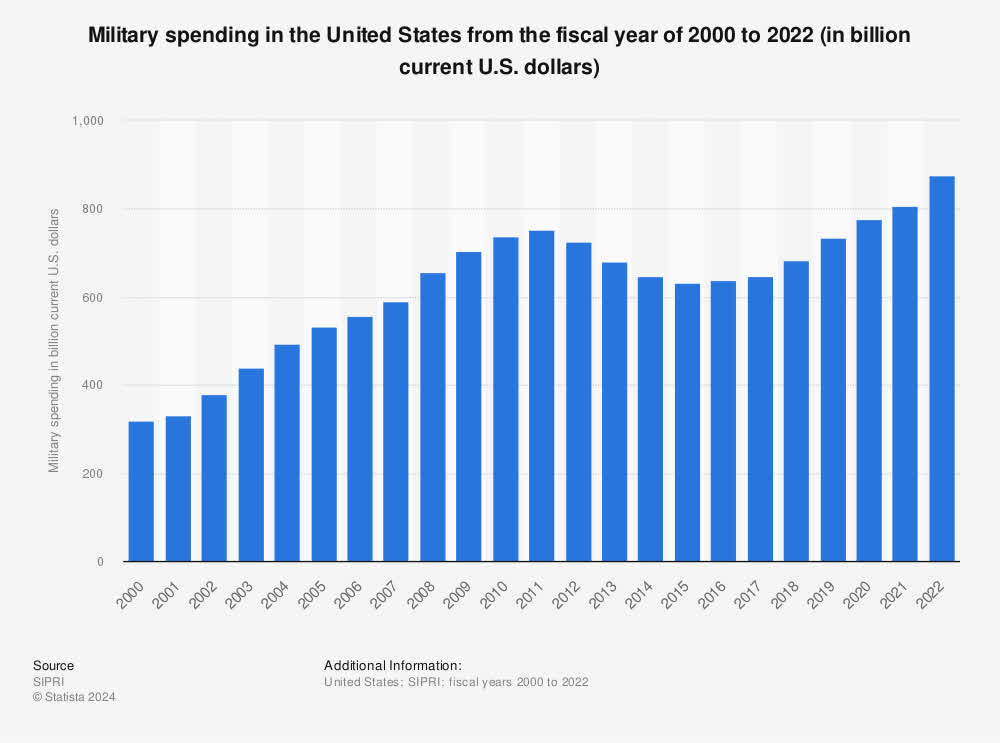

Rolls-Royce Holdings’ second main market, protection gear, is rising as properly. Resulting from a variety of conflicts around the globe, many militaries are upping their protection spending. In the USA, navy spending has been rising for years as properly:

US navy spending (statista.com)

Rolls-Royce Holdings advantages from elevated navy spending by the US, different NATO members, and different US allies by way of the sale of parts equivalent to navy plane engines, naval engines, and even nuclear energy vegetation for submarines. Whereas the protection unit is smaller than the civil plane engine unit, it’s nonetheless a significant contributor to Rolls-Royce Holdings’ total enterprise progress.

Rolls-Royce Holdings’ Energy Programs and New Power models are smaller, however some would possibly argue that they might be main progress drivers sooner or later. In spite of everything, Rolls-Royce Holdings is engaged on small modular reactors (a kind of nuclear energy plant) which are seen, by some, together with Invoice Gates, as an necessary future supply {of electrical} power. Whether or not the idea is in the end profitable and economical just isn’t but recognized for certain, and we additionally do not know which of the businesses on this house are best-positioned — Invoice Gates, for instance, has funded considered one of Rolls-Royce’s opponents. Small modular reactors are receiving funding from establishments such because the European Union, thus Rolls-Royce Holdings is energetic in a area that appears extremely enticing, though success is, as talked about above, not sure.

Rolls-Royce Holdings: Reasonably Costly

So Rolls-Royce has a checkered previous, partially attributable to company-specific points and self-inflicted wounds, partially attributable to macro headwinds such because the pandemic. The outlook over the approaching years is optimistic, however traders must also think about the corporate’s valuation, which is fairly excessive immediately.

Primarily based on present estimates for this yr, Rolls-Royce Holdings is buying and selling for a bit greater than 28x web income, which pencils out to an earnings yield of simply 3.5% — at a time when zero-risk treasuries yield far more than that. After all, exceptionally sturdy progress could warrant a premium valuation, however Rolls-Royce Holdings’ forecasted progress is not excessive — it is rather strong, however removed from Nvidia-like (NVDA). Even after we have a look at revenue estimates for 2026, i.e. two years from now, the earnings a number of stands at 23, with forecasted progress between 2024 and 2026 being round 25% cumulatively, or round 12% per yr. The PEG ratio is thus fairly elevated, at round 2, making me consider that Rolls-Royce Holdings just isn’t very attractively priced immediately.

Traders that need aerospace and protection publicity may as a substitute go for firms equivalent to Lockheed Martin (LMT), buying and selling at simply 18x web earnings, providing a pleasant dividend, having a greater observe document, and providing nuclear energy potential as properly. Airbus (OTCPK:EADSY) trades for 26x ahead earnings, is forecasted to develop by 12% per yr in 2025 and 2026 as properly, provides a dividend, and arguably has a much bigger moat than Rolls-Royce whereas additionally benefitting from Boeing’s (BA) issues.

General, Rolls-Royce Holdings is much from a foul firm, however the inventory just isn’t buying and selling at a valuation deserving of a “Purchase” ranking. For many who purchased this firm nearer to the lows, it has been a terrific funding, however I would not put new cash into Rolls-Royce at greater than 28x web income.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.

{kind=link}