halbergman

January ninth was not that nice a day for shareholders of hashish agency Tilray Manufacturers, Inc. (NASDAQ:TLRY). Shares of the corporate dropped round 9.4% after administration reported monetary outcomes masking the second quarter of the firm’s 2024 fiscal yr. Though the enterprise exceeded expectations when it got here to adjusted earnings per share, it fell in need of forecasts when it got here to each income and GAAP earnings.

Administration did shock traders by reporting some moderately strong development when it got here to the beverage alcohol operations of the corporate. However exterior of that, there wasn’t all that a lot that was particular. We’re seeing, along with some good income development, some enchancment within the firm’s backside line. However for my part, the expansion and enchancment seen to date don’t but make the corporate a viable prospect for something apart from speculative traders.

Not a high-flying quarter

Within the final article that I revealed about Tilray Manufacturers again in August of 2023, I lauded the corporate’s resolution to amass 8 beer and beverage manufacturers from alcohol large Anheuser-Busch InBev (BUD) in trade for $85 million. These had been marginal manufacturers that didn’t transfer the needle for his or her prior proprietor. However for an enterprise like Tilray Manufacturers, which is hoping to develop a number of income strains directly, the acquisition of manufacturers which are already acknowledged made quite a lot of sense.

Regardless of my optimism concerning the transaction, I additionally said that Tilray Manufacturers nonetheless confronted some significant challenges that made it a dangerous funding. That led me to reiterate the “Promote” ranking I already had on the inventory. On the finish of the day, that has confirmed to be a smart resolution. Whereas the S&P 500 (SP500) is up 5.8% for the reason that publication of my article, shares of Tilray Manufacturers have generated draw back of about 25%.

Creator – SEC EDGAR Knowledge

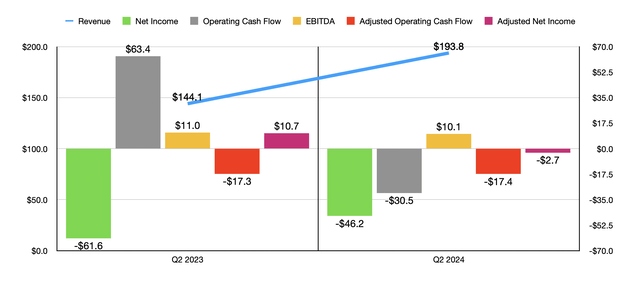

I take no pleasure in Tilray Manufacturers underperforming the market. Though I personally am not supportive of the leisure hashish business, I wish to see companies succeed. Main as much as the earnings launch for the enterprise, my hope was that monetary efficiency would are available sturdy. However for probably the most half, these hopes fell flat. Let’s take income to start out with. Gross sales for the second quarter of the 2024 fiscal yr totaled $193.8 million. That is 34.5% increased than the $144.1 million reported one yr earlier. Though this represents a pleasant improve year-over-year, it really fell in need of analysts’ expectations to the tune of about $1.2 million.

There’s a lot to unpack right here. As an example, whereas all segments of the corporate reported year-over-year development, the best improve in gross sales got here from the beverage alcohol enterprise of the corporate. Income shot up from $21.4 million to $46.5 million. Administration didn’t reveal how a lot of this development was pushed by the aforementioned buy. Nevertheless it’s clear that it had some affect. This dimension makes the corporate the fifth largest craft beer brewer within the nation. And if the present pattern continues, administration sees the enterprise turning into a prime 12 participant relating to the beverage/alcohol area, within the nation.

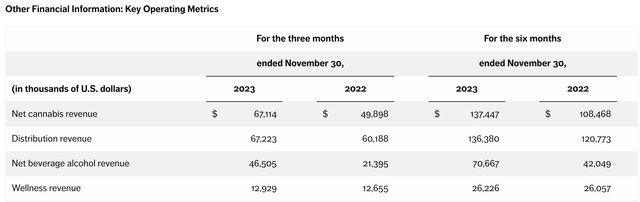

After all, there have been different areas of development for the corporate. Most notably was the hashish enterprise. Income jumped from $49.9 million final yr to $67.1 million this yr. The distribution and wellness companies additionally grew, however their improve was marginal by comparability.

Tilray Manufacturers

On the underside line, Tilray Manufacturers reported a loss per share accounting to $0.07. That is higher than the $0.11 per share misplaced within the second quarter of 2023. Nevertheless, it missed analysts’ expectations by $0.01 on a per share foundation. Which means that internet income went from destructive $61.6 million to destructive $46.2 million. On an adjusted foundation, the corporate broke even on a per share foundation with a lack of solely $2.7 million. That is far worse than the $10.7 million adjusted revenue reported one yr earlier. Nevertheless it exceeded analysts’ expectations by $0.05.

Creator – SEC EDGAR Knowledge

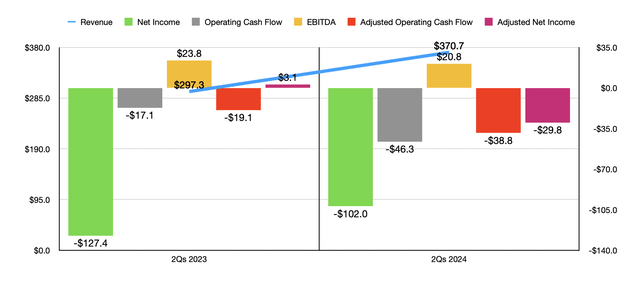

There have been, after all, different metrics reported that present a barely worse aspect to the corporate. Working money move, as an example, went from $63.4 million to destructive $30.5 million. If we alter for modifications in working capital, it was almost the identical, coming in at destructive $17.4 million in comparison with the destructive $17.3 million seen one yr earlier. Lastly, EBITDA for the agency went from $11 million to $10 million. Within the chart above, you may also see monetary efficiency for the primary half of 2024 relative to the identical time of the 2023 fiscal yr. This reveals a blended image as effectively, with income and income bettering however different profitability metrics worsening moderately considerably.

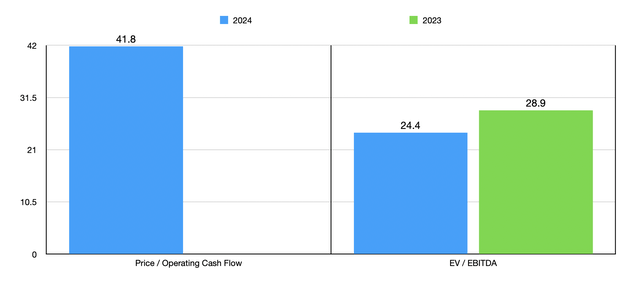

Given a few of these readings, it may be troublesome to consider that administration is being forthright relating to a few of their claims. Within the press launch, as an example, the corporate said that it nonetheless believes it may well obtain between $30 million and $35 million in synergies related to its acquisition final yr of rival HEXO. Nevertheless, it even went a step additional, claiming that it has achieved $22 million in annual run price synergies and $14 million in precise value financial savings, within the second quarter alone. The corporate then went to assert that steering for this yr requires EBITDA of between $68 million and $78 million. That will evaluate favorably to the $61.5 million reported for 2023. If we take the midpoint of steering, that might give us adjusted working money move, in keeping with my estimate, of about $37.3 million for 2024.

Creator – SEC EDGAR Knowledge

Within the chart above, you may see how shares are priced on each a ahead foundation and utilizing information from 2023. If the corporate was rising at a way more fast tempo, these numbers may be acceptable. However at this price, it’ll take the agency far too lengthy to develop into moderately priced. That is particularly if they’re being trustworthy about how a lot in financial savings they’ve already captured. After all, they don’t seem to be the one participant available in the market presently struggling. Rival Cover Development Company (CGC) is doing even worse.

Utilizing the latest information, which covers the second quarter of 2024 and that got here out in November of final yr, Cover Development noticed its income drop 18.3% year-over-year, whereas its internet loss for the quarter totaled CDN$324.8 million. Its shares had been additionally down moderately considerably on January ninth, falling about 8.3% as I write this. This was in response to administration issuing a non-public placement to promote $30 million price of inventory (within the type of warrants) at a share value of $4.83. That is at a 4.2% low cost to the $5.04 that shares had been buying and selling at on January eighth.

What’s worse than the low cost is the truth that half of the warrants, that are exercisable instantly, give the house owners the precise to buy stated inventory at stated value for 5 years, whereas the opposite half offers the identical five-year time however with a place to begin six months from issuance. Which means that administration isn’t terribly frightened about its share value rising materially over the subsequent few years, which isn’t confidence-inducing for the corporate’s traders.

Takeaway

As issues stand, I don’t discover myself all that taken with Tilray Manufacturers from an funding perspective. Even when I had been a fan of the hashish market, the monetary information simply isn’t there to help the sort of valuation that we’re taking a look at. A market capitalization of $1.56 billion for an organization producing lower than $800 million in income yearly, and that’s on monitor to lose round $200 million for the yr if issues persist, is simply not possible. On account of this, I’ve no downside retaining the corporate rated a “promote” for now.

{kind=link}