RHJ

Uranium shares are distinctive throughout the vitality business as a result of they face financial fundamentals which might be vastly totally different from others. Additional, the North American uranium mining business is liable to immense hypothesis from retail traders, because the sector is usually unprofitable (significantly in the US). Most world uranium provides come from Kazakhstan via dominant corporations like Cameco (CCJ).

Since uranium is susceptible to large increase and bust cycles and has much less easy economics, it’s typically caught up in misconceptions or extra optimistic or destructive outlooks. That is understandably the results of immense market volatility and hypothesis within the sector, significantly concerning the potential for extra North American uranium mining firms to turn out to be worthwhile as costs rise.

Additional, many traders have a bullish tackle uranium because of their optimistic outlooks on nuclear vitality. In my view, the efficiency of uranium miners might not be related to the potential progress of nuclear vitality, stemming from the immense time lag for nuclear development and the excessive potential provide of uranium ore.

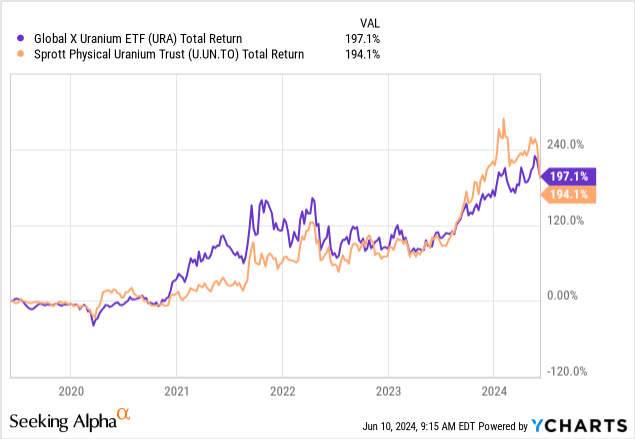

The business confronted important optimistic momentum final 12 months, with uranium ore being among the many only a few vitality commodities to rise. The favored uranium ETF (NYSEARCA:URA) is up 40% YoY, benefiting from a big wave in hedge fund shopping for exercise. URA is up by ~197% over the previous 5 years, with the uranium bodily commodity ETF (OTCPK:SRUUF) (the US OTC Ticker for Sprott Bodily Uranium Belief) up by the same diploma. Notably, URA and the bodily commodity have slipped in current weeks following a stagnation in uranium costs over the previous 5 months. See beneath:

In December of 2023, I revealed a impartial outlook for the uranium miner ETF (URNM), adopted by a bearish outlook on its main holding, Cameco (CCJ). CCJ can also be the biggest holding within the extra common uranium ETF URA at ~26% of its belongings. CCJ has risen since I lined it final, however uranium costs have stagnated and declined, with many smaller miners slipping. To me, that signifies the market could also be turning into additional dislocated from its fundamentals, pointing to declines for the business.

That mentioned, some market facets have modified in current months, so I imagine it’s a good time to cowl the favored uranium ETF (URA) to offer an up to date outlook. Beforehand, I used to be impartial on URA after being bullish from 2019 to 2021, incomes a large achieve over that interval.

Nuclear Demand is Unlikely To Rise Quickly

In my view, among the bullish arguments surrounding URA usually are not well-founded within the business’s financial fundamentals. For instance, analysts or traders typically level towards AI as rising demand for energy after which assume that nuclear should be that energy supply, implying that uranium costs will rise and improve the earnings and valuations of uranium miners.

I am going to assume that US energy demand will rise, given some evaluation that factors towards a ~20% improve in demand by 2030 from AI knowledge facilities. Nonetheless, it’s unclear if AI will see that velocity of demand progress. That mentioned, I don’t suppose that is essential for uranium as a result of there’s a good larger time between energy demand and nuclear energy plant improvement.

It takes round 7.5 years to assemble a nuclear and longer if we contemplate planning and laws. Additional, that knowledge is based totally on development instances in Asia, the place nuclear is rising the quickest, as US nuclear energy has steadily declined lately. The latest US nuclear plant in Georgia was accomplished seven years late and value over twice as a lot because the preliminary estimate. In different phrases, America’s first new reactor in over thirty years took fourteen years to construct, implying the US is nowhere near the velocity of China for nuclear plant development.

Nuclear energy will not be economical, with Lazard estimating its Levelized Price of Power to be round $182/MWh. So as, onshore wind, geothermal, coal, and utility-scale photo voltaic are cheaper. The one energy supply with a decrease return is residential rooftop photo voltaic, which advantages from theoretically decrease transmission wants. It might be argued that nuclear energy vegetation’ whole scale and lack of greenhouse gases make up for his or her decrease ROI. Nevertheless, the actual fact is that nuclear vegetation are extremely capital-intensive (a difficulty with excessive rates of interest), take a really very long time to plan and construct, and have immense ongoing labor overhead prices (an issue with inflation).

Additional, decommissioning is anticipated to speed up over the approaching a long time because of ageing nuclear vegetation in a lot of the developed world. Some hope to increase their lives, however many are too expensive to function.

Arguments could also be made about why nuclear continues to be a viable future energy supply. Certainly, the Biden administration has just lately shifted to help creating and sustaining nuclear vegetation. Nonetheless, even when there’s a important renaissance in US and European nuclear energy, that possible won’t end in an increase in uranium demand till the 2040s to 2050s, given the timeline of those tasks. However, renewables like wind and photo voltaic are seeing regular double-digit annual progress, with important anticipated acceleration over the approaching 5 years.

Uranium Economics Bearish For URA

Uranium will not be like oil, as it’s way more plentiful globally. In keeping with an NEA examine, there’s possible round 230 years of provide of uranium assets accessible on the 2009 consumption stage. Though that examine is effectively over a decade outdated, it stays related as there haven’t been important modifications in uranium provide and demand since then. That examine additionally famous that technological enhancements in extraction and exploration have been more likely to double that estimate over time. Additional, it famous that if a way for extracting uranium from seawater have been discovered, there can be over thirty thousand years of accessible provide.

I am positive some might argue the specifics, however the reality is that uranium provide will not be a constraint on nuclear energy. Which will make nuclear energy a viable clear vitality supply, significantly a long time into the long run, however that doesn’t make uranium mining worthwhile.

Remember the fact that the uranium demand curve is theoretically utterly inelastic. Energy vegetation won’t lower demand with larger costs of uncooked ore as a result of uncooked ore prices are negligible in comparison with enrichment prices, and even enriched uranium is a low general value of working a plant (in comparison with expert labor). This advantages URA by implying larger uranium ore costs won’t end in decrease demand.

Nevertheless, since many semi-developed uranium mines within the US usually are not working, the availability curve is probably going very elastic. There may be some debate on this level, however most research level to an exponential potential improve in provide as uranium crosses over into the $100 to $150/lbs vary. Do not forget that demand is basically stagnant immediately, with annual world demand progress forecasted at ~1%.

Thus, now that uranium is floating across the $85/lbs to $100/lbs vary, many US miners are lastly restarting manufacturing. The entire vital knowledge concerning provide and demand usually are not public. Nevertheless, I imagine it’s a digital certainty that the approaching output progress from US miners can be larger than demand progress, which is negligible.

I imagine Uranium costs usually are not rising because of rising climate-change-related demand, as some media retailers have popularized. It is usually primarily not appropriate that US mines are restarting due to misplaced Russian assets. The US needs to develop its uranium enrichment base to decrease its dependence on Russian enrichment services. In the long term, that will profit US ore miners, however once more, enrichment is, by orders of magnitude, the more expensive a part of the uranium gasoline cycle than mining.

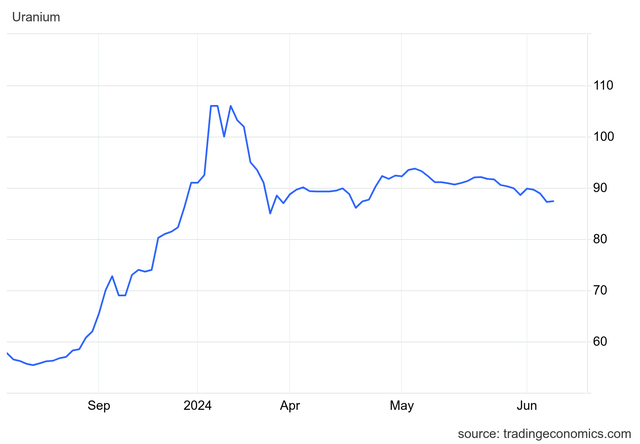

In actuality, the 2023 spike in uranium costs is primarily the delayed results of a provide and demand imbalance created by Cameco’s non permanent closure of MacArthur River and Cigar Lake, main world provide sources from Canada. Since these are North American uranium mines, they’ve a lot larger working prices than these in Kazakhstan. Thus, Cameco will typically lower manufacturing from these services if uranium costs are beneath $70/lbs (roughly). Nevertheless, because of COVID lockdowns and associated provide and labor points (lasting into 2023), the corporate had issue restarting manufacturing, resulting in a provide shortfall. The Niger Coup might have barely exacerbated this shortfall, however Kazatomprom shortly mentioned they’d improve exports (from Kazakhstan) to make up for any Niger-related shortfalls.

So, with Kazatomprom and Cameco now having normalized manufacturing and Cameco trying to develop its output, the availability hole is more likely to shut. Round Q3 to This autumn of 2024, US provides are anticipated to extend as a result of restarted mines. To me, this may possible push the uranium market again right into a persistent provide glut by 2025-2026. Thus, uranium costs are proof against rising over the $90-$100 vary, the place most North American miners can break even. See beneath:

Uranium Futures Worth (USD/LBS) (TradingEconomics)

In my view, the financial legislation of the zero-profit situation holds true within the uranium market. Think about the worldwide uranium mining business dominated by an oligopoly of Cameco, Kazatomprom, Orano, CGN, and Uranium One, collectively controlling round two-thirds of world provides. Largely, these firms share possession of quite a few mines in Kazakhstan and Canada and are liable to reducing manufacturing when costs decline. This creates a long-term uranium value ground of round $40/lbs to $70/lbs in immediately’s market, which is excessive sufficient for Kazakh mines to revenue however just under the North American breakeven ranges. As costs cross above that stage, we’re seeing extra small North American miners (of which there are numerous) look to ramp up manufacturing. Thus, trying ahead, it is rather possible that output will rise above demand, making a value ceiling of round $100/lb.

The difficulty with URA is that the majority of its holdings are in North America and Australia, the place uranium is round that zero revenue situation immediately. Moreover the quarter of the fund in Cameco (which has constantly worthwhile mines exterior North America) and the 7.5% of the ETF in Sprott Bodily Uranium, the remaining two-thirds of the fund is within the many small mines that haven’t any oligopoly pricing energy.

Many of those mines are more likely to be worthwhile immediately. Nevertheless, if all of them act on that and lift manufacturing to earn a revenue, I imagine it’s nearly sure that provides will rise above demand, pushing uranium again beneath $70/lb, leading to important losses. For instance, the ahead EPS outlook for Uranium Power Corp (UEC) and Denison (DNN) (two top-ten URA holdings) is -$0.01 and -$0.03, respectively, indicating they’re at breakeven with uranium round $90 however will face losses ought to it decline. Once more, I might be shocked to see uranium rise above $100 and stay that top exterior of a geopolitical disaster in Kazakhstan.

With the market the place it’s, I see no purpose to put money into uranium miners as I anticipate they may face losses over the approaching two years as their renewed output pushes the market right into a glut. Once more, there’s zero purpose to imagine uranium demand will improve within the coming years, not to mention within the coming a long time, so a slight provide improve would shortly create a glut. For a similar purpose, I proceed to imagine Cameco is wildly overvalued, primarily as a result of its provide contracts will significantly inhibit it from cashing in on the 2023 uranium rally. I feel uranium costs will decline by the point the majority of its contracts roll ahead, largely due to Cameco’s renewed output ranges.

One notable optimistic level concerning Cameco is its Port Hope conversion facility, which converts uranium to UF6 gasoline. That is one key asset that ought to profit from the trouble to maneuver away from Russian-converted to gasoline. Though I anticipate this facility to earn larger earnings, I don’t imagine it might offset the glut danger within the broader mining house.

The Backside Line

General, I’m bearish on URA immediately and imagine the uranium mining sector is kind of overvalued, given the numerous danger that the market will shift again right into a glut by the top of this 12 months. CCJ and chronically negative-cashflow North American uranium miners appear to have essentially the most important draw back danger, given it appears extreme investor exuberance surrounding uranium, which I imagine will not be well-founded in financial fundamentals.

That mentioned, there’s one circumstance the place I might turn out to be very bullish on URA, which isn’t essentially a really low-probability occasion. A lot world uranium comes from Kazakhstan particularly, in addition to Africa. Kazakhstan has a danger of unrest and instability. It is usually carefully tied to Russia and is a part of its CSTO navy alliance.

Whereas Western political leaders are primarily involved with Russian import dependence on enriched uranium, that problem might shift towards Kazakhstan’s import dependence on uranium ore. Certainly, ought to Kazak uranium imports to the EU and the US cease immediately, it might create a disaster as though North America (and Australia) has important potential uranium, the mines haven’t ramped up output quick sufficient to offset this. Thus, there’s sturdy reasoning that the US ought to and can prop up its uranium miners for nationwide safety. Certainly, this was a big problem that the Trump admin had labored on, which had made me bullish on US miners in 2019.

So, whereas the present financial scenario doesn’t appear to be bullish for URA, that would change on a dime with world geopolitics. At this level, there is no such thing as a speak of stopping Kazakhstan imports. Nevertheless, with Biden’s potential pro-nuclear and uranium safety shift and Trump’s historic give attention to this problem, I feel there’s purpose to invest. Nonetheless, I’m not satisfied the valuations of many North American miners are wise, but when uranium rises into the $200+ vary because of a provide disaster from Central Asia, then that would change.

{kind=link}