With mortgage charges surging increased once more, considerably unexpectedly, a thought got here to my thoughts if you happen to’re at present residence buying.

A pair years in the past, I threw out the concept to regulate your most buy value decrease when searching for a property.

That submit was pushed by the numerous residence gross sales that had been going means above asking on the time. In different phrases, a house could have been listed for $600,000, however finally bought for $700,000 in a bidding battle.

That was all to do with a very popular housing market, pushed largely by a mix of document low mortgage charges and really low for-sale provide.

Immediately, we nonetheless have comparatively low stock, however the low-cost mortgage charges have come and gone.

And now that they’re so risky, it’s possible you’ll need to enter the next charge into your mortgage calculator to make sure you don’t get caught out.

Mortgage Charges Are Extremely Risky Proper Now

In the mean time, mortgage charges are tremendous unpredictable. Whereas that they had loved an excellent 11 months, falling from as excessive as 8% to just about 6% in early September, they’ve since reversed course.

The 30-year fastened was practically again into the excessive 5% vary earlier than the Fed lower charges and a better-than-expected jobs report arrived.

Sprinkle in some doubting concerning the Fed’s pivot and the upcoming uncertainty relating to the election consequence and residential patrons at the moment are going through a charge practically 1% increased.

Per MND, the 30-year fastened has risen from a low of 6.11% on September seventeenth to six.92% as of October twenty third.

Speak about a tough month for mortgage charges, particularly since many anticipated the Fed’s charge reducing marketing campaign to be accompanied by even decrease mortgage charges.

It’s an excellent reminder that the Fed doesn’t management mortgage charges, and that it’s higher to trace mortgage charges by way of the 10-year bond yield.

Additionally, these yields are pushed by financial knowledge, not what the Fed is doing. By the best way, the Fed makes strikes based mostly on the financial knowledge too. So comply with the financial knowledge for crying out loud!

Anyway, this latest transfer up serves an awesome reminder that mortgage charges don’t transfer in a straight line. And to anticipate the surprising.

Err on the Facet of Warning By Inputting a Greater Mortgage Fee

When you’re at present trying to buy a house, it’s typically a good suggestion to get pre-qualified or pre-approved upfront.

That means you’ll know if you happen to truly qualify for a mortgage, and at what value level, together with needed down cost.

The factor is, these calculations are solely nearly as good because the inputs. So in case your mortgage officer or mortgage dealer places in overly favorable numbers, it may skew the affordability image.

In different phrases, you virtually need to ask them to place in a mortgage charge that’s 1% increased than at this time’s market charges.

That means you may take up the next cost if charges occur to worsen throughout your property search, which might take months and months to finish.

If charges occur to fall throughout that point, great, it’ll simply be the icing on the cake. Your anticipated month-to-month PITI shall be even higher than anticipated.

However like these bidding wars that passed off, which resulted in increased asking costs, surprising spikes in charges also needs to be anticipated.

And if they’re, you would possibly take a look at properties which are extra inside your value vary, versus properties that solely work if every thing is good.

Provided that owners insurance coverage and property taxes are additionally on the rise (with nearly each different value), it could repay to be prudent together with your proposed residence shopping for price range.

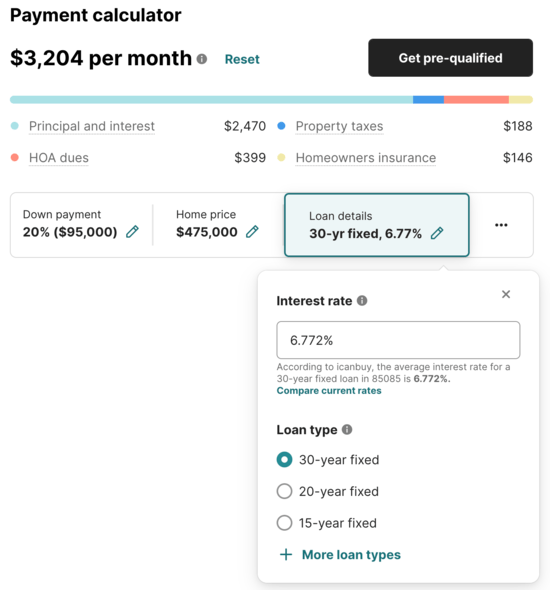

Modify the Mortgage Fee on the Property Itemizing Web page

When you’re utilizing a website like Redfin to browse listings, there’s a useful mortgage cost calculator on every itemizing web page.

It offers default quantities based mostly on typical down funds, mortgage charges, property taxes, and house owner insurance coverage.

Let’s say that rate of interest is 6.77% at this time, which is fairly cheap given present market charges.

When you click on on the little pencil icon, you may change it to something you need. You may also choose a distinct mortgage sort when you’re at it.

When you do, it tends to save lots of your inputs, so once you take a look at different properties, the speed you chose earlier ought to apply to different properties.

This can provide you a quicker, maybe extra practical estimate of the month-to-month cost, as an alternative of a charge which may change into too good to be true.

So you might put in 7.75%, or perhaps 7.50%. That means if charges go up, otherwise you qualify for the next charge due to some loan-level value changes, you gained’t be caught off guard.

You’re principally taking part in it extra conservatively in case pricing worsens, which is the prudent strategy.

When you’re at it, it’s possible you’ll need to overview the opposite inputs to make sure they’re reflective of your proposed mortgage.

Are you actually going to place 20% down on the house buy, or simply 3% to five%?

Overestimating these prices as an alternative of probably underestimating them may help you keep away from being home poor. Or worse, lacking out in your dream residence solely on account of inaccurate estimates.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on Twitter for decent takes.

{kind=link}