Walter Bibikow/DigitalVision through Getty Photographs

I’m including to my place in VICI Properties Inc. (NYSE:VICI) as of late because the experiential actual property funding belief affords a top quality 5.4% yield, a low pay-out ratio and a diversified portfolio poised to produce long-term funds from operations progress.

The true property portfolio is well-managed and the actual property funding belief is poised to boost its dividend within the third quarter.

I feel that VICI Properties makes a sexy worth proposition for passive revenue traders, significantly in gentle of the belief’s previous dividend progress.

I additionally assume that the U.S. economic system just isn’t but headed for a recession, which might give VICI Properties’ tailwinds for growth and progress in its funds from operations.

My Ranking Historical past

VICI Properties owns a cyclical, but inflation-protected actual property portfolio that’s dominated by gaming properties. The presence of lease escalators and the main place of Las Vegas as a vacationer vacation spot had been causes that supported my prior Purchase advice for VICI Properties.

I feel that VICI Properties continues to ship strong FFO worth to passive revenue traders in a rising economic system. The belief can also be poised to announce the next dividend in September, which might make VICI Properties much more engaging as a passive revenue holding.

Portfolio Evaluation

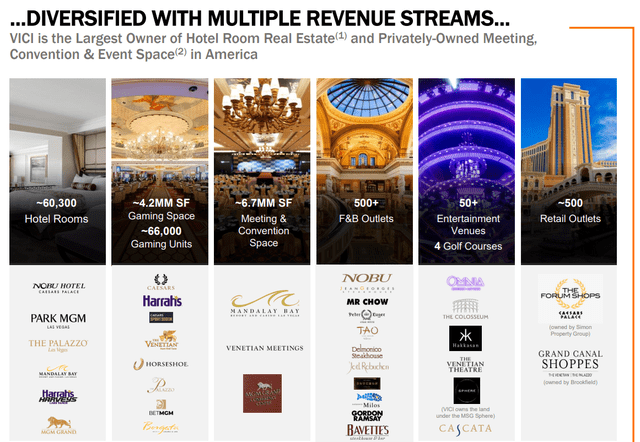

VICI Properties owns a big, Las Vegas-anchored, portfolio of gaming properties. The gaming actual property funding belief owns 54 gaming and 39 different experiential properties, together with assembly & conference house, resort rooms, retail outlet, golf and different leisure venues.

VICI Properties is targeted on long-term leases (which had a weighted-average lease time period of 41.5 years) and had 100% occupancy as of March 31, 2024.

Diversified Income Streams (VICI Properties Inc)

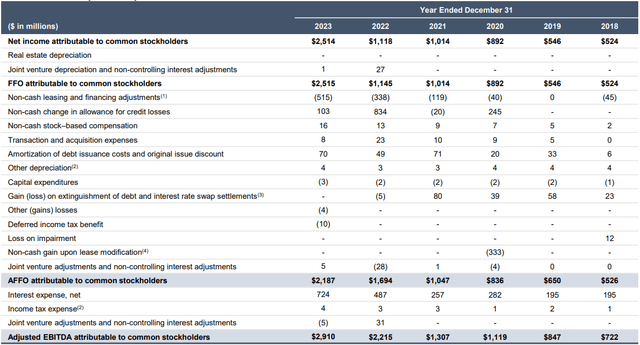

VICI Properties has persistently grown its adjusted funds from operations within the final six years, and this contains even the Covid pandemic. In 2023, all of VICI Properties produced $2.19 billion in adjusted funds from operations, reflecting progress of 316% since 2018 and 29% progress YoY.

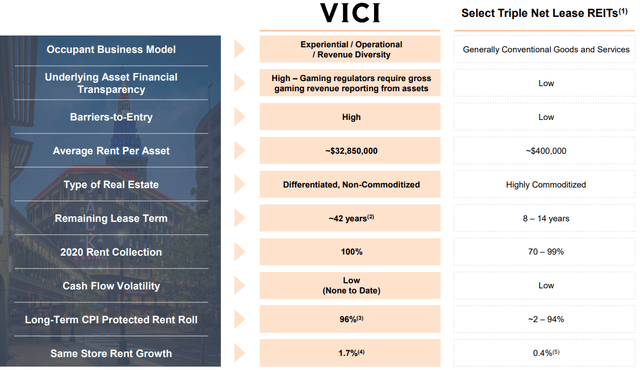

The important thing to VICI Properties monetary success is that the actual property funding belief owns properties in severely supply-limited areas, such because the Las Vegas strip.

As a consequence, VICI Properties has a large moat (low threat of recent market entries given the restricted provide of recent land at prime areas) and may cost tenants excessive charges for his or her properties.

Funds From Operations (VICI Properties Inc)

VICI Properties has distinctive lease options, ensuing from a excessive barrier of entry for rivals, together with a for much longer weighted-average lease time period, stronger lease assortment charges and better same-store lease progress.

Distinctive Leasing Options (VICI Properties Inc)

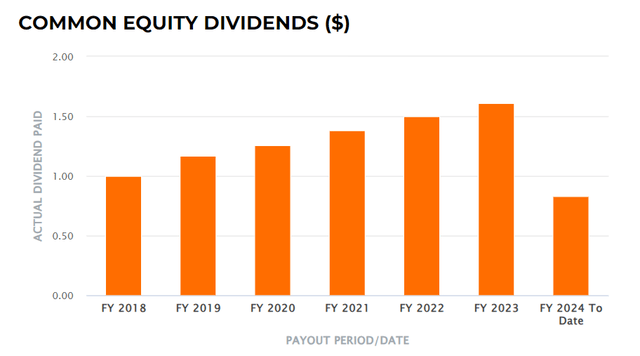

VICI Properties Pays A Rising 5.5% Yield And Delivers Dividend Development

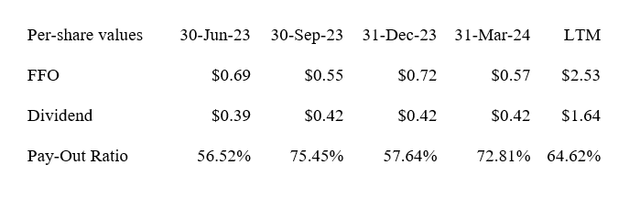

VICI Properties is doing nicely for itself by way of dividend protection. The experiential actual property funding belief earned $0.57 per share within the first quarter whereas paying out $0.415 per share in dividends, which introduced the dividend pay-out ratio to 73%.

Within the final twelve months, VICI Properties had a dividend pay-out ratio of 65%, so I feel passive revenue traders don’t have to fret in regards to the dividend presently.

Dividend (Writer Created Desk Utilizing Belief Info)

Importantly, VICI Properties is rising its dividend pay-out and traders can moderately anticipate a dividend hike in September. Between 2018 and 2023, the actual property funding belief raised its dividend by a median of 10% each year. I anticipate a 5% or greater dividend enhance in September, which might give traders a pleasant revenue increase.

Frequent Fairness Dividends (VICI Properties Inc)

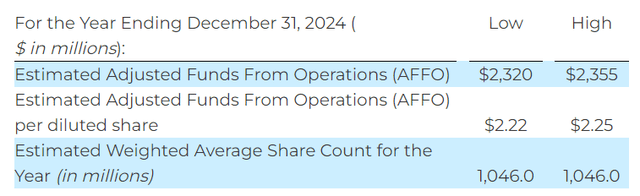

FFO Steering And A number of

VICI Properties reaffirmed its AFFO outlook for 2024 within the final quarter and continues to see $2.22 to $2.25 per share in adjusted funds from operations. For the reason that belief’s inventory is now promoting at $30.62, the valuation implies a AFFO a number of of 13.7x.

AFFO Outlook (VICI Properties Inc)

I’d evaluate VICI Properties to EPR Properties (EPR) which can also be an experiential actual property funding belief, although with a barely completely different portfolio orientation.

EPR Properties is extra oriented towards theaters, eat-and-play services, training services and ski resorts, however the belief has an identical pay-out ratio than VICI Properties, of about 65% on a final twelve months foundation.

EPR Properties is presently promoting at 9.0x estimated 2024 FFO, based mostly on a forecast of $4.76-4.96 in funds from operations as adjusted. I see EPR Properties as significantly undervalued, however I feel that each VICI Properties and EPR Properties as ‘Purchase’s from a valuation and margin of security angle.

Why The Funding Thesis Is Dangerous For Passive Earnings Buyers

As a gaming-focused actual property funding belief, VICI Properties has significantly greater FFO and pay-out volatility than extra secure, residential-focused actual property funding trusts.

The 2 largest tenants, Caesars Leisure and MGM Resorts, account for 74% of VICI Properties annualized lease, which means if certainly one of these corporations goes underneath, it will have a dramatic impression on VICI Properties’ money circulation and which might presumably result in a dividend lower.

My Conclusion

VICI Properties has a big, entertainment-focused actual property portfolio and produces a excessive quantity of funds from operation from its gaming properties.

The belief’s adjusted funds from operations are rising and VICI Properties runs a moaty enterprise, resulting in robust lease metrics together with 100% occupancy and long-term leases that create a excessive diploma of money circulation visibility.

As a consequence, VICI Properties can afford to pay a 5.5% dividend, which has persistently been coated by adjusted funds from operations.

The belief is rising its dividend pay-out as nicely and poised to boost its dividend once more within the third quarter.

The inventory is reasonably valued, reflecting a excessive margin of security for passive revenue traders. Purchase.

{kind=link}